Industry enterprises have rebuilt their logistics routes by directing exports to European seaports

In the conditions of Russian military aggression and the blocking of seaports, Ukrainian iron and steel companies, through trials and errors, began in 2022 to build new logistics routes for the export of their products. It quickly became clear that it would be much more expensive and longer than before the war. However, within a few months, enterprises in the industry were able to largely reconfigure their logistics, although due to the war and the reduction in production, export traffic volumes decreased significantly.

Focus on Euroports

Ukrainian steel industry and mining companies were hit hard by the blockade of the Black Sea by the Russian navy, as shipping was the main export route. The share of maritime transport in the pre-war export of iron ore was 60%, iron and steel – 80%.

“Before the outbreak of hostilities in 2022, 98% of ArcelorMittal Kryvyi Rih products were shipped by sea, mainly on FOB terms through Ukrainian ports (Mykolaiv, Odesa). With the outbreak of hostilities and the closure of Ukrainian port facilities, the business model also changed. The only option to keep sales of products was the option of reorientation to the port infrastructure of European countries,” emphasizes Andriy Myagkov, Logistics Director at ArcelorMittal Kryvyi Rih.

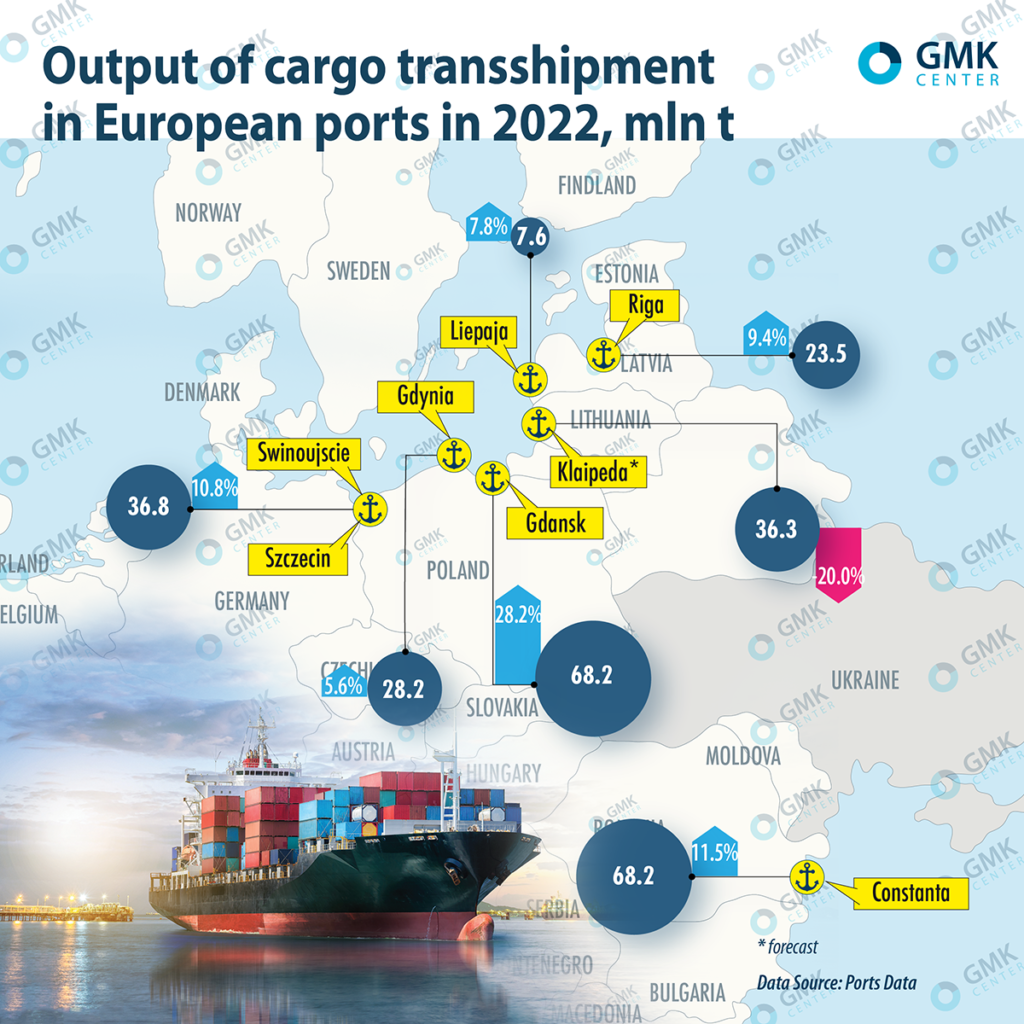

Ukrainian steel exporters were forced to redirect cargo flows to EU seaports: to Romania (Constanta), Bulgaria (Burgas), Poland (Gdynia, Gdansk, Szczecin-Swinoujscie), Croatia (Rijeka, Ploče), Germany (Hamburg, Bremerhaven, Bremen), as well as the Netherlands (Rotterdam). In particular, Metinvest company in 2022 had to refocus on European port terminals: Rijeka, Ploce, Constanta, Swinoujscie, Szczecin, Gdansk, Gdynia.

According to Andryi Myagkov, in the first few months of the war, the vast majority of goods from Ukraine poured into the nearest countries with access to maritime navigation, since these were the shortest routes and, therefore, the cheapest.

The Polish ports of Gdansk, Gdynia, Szczecin, as well as the Romanian port of Constanta were the most loaded with Ukrainian goods in 2022.

“We had to quickly redirect the cargo that was already at the sea to the ports of the EU countries, to form new logistics chains of steel supplies to Ukraine from countries far abroad. For the import of goods, we mainly used vehicles through the Polish ports of Gdynia and Gdansk or the Romanian Constanta. Our logisticians had to negotiate and control the forwarding of cargo from Odesa, Romania and Poland almost 24 hours a day. And in order not to overload one port, it was necessary to transport goods through several at once,” adds Oleksiy Didenko, head of the marketing department at Forteks company.

All foreign ports that are logistically accessible for Ukrainian exports and imports showed an increase in cargo transshipment in 2022, although the dynamics of processing iron and steel products was multidirectional.

The dynamics of transshipment by individual ports looks like this:

- Gdansk increased its total handling by 28.2% y/y – up to 68.2 million tons. At the same time, the port reduced the handling of dry bulk cargo, including iron ore, by 20% y/y. – to 3.6 million tons;

- Szczecin-Swinoujscie – transshipment growth by 10.8% y/y – up to 36.8 million tons. At the same time, iron ore transshipment increased by 11.4% y/y – up to 2.11 million tons;

- Riga – transshipment growth by 9.4% y/y – up to 23.5 mt. Iron ore transshipment increased by 16.8% y/y – up to 954.6 thousand tons, but the processing of ferrous metals decreased by 28.7% y/y – to 516.6 thousand tons;

- Liepaja – transshipment growth by 7.8% y/y – up to 7.6 million tons. Transshipment of iron and manganese ores increased by 11.5 times – up to 58.7 thousand tons, steel processing decreased by 43.3% y/y – to 9.5 thousand tons.

Now only Danube ports continue to operate in Ukraine, but they have relatively small capacities and cannot solve the existing logistical problems. They are already working at almost the maximum of their capabilities. The volume of cargo handling in the port of Reni in 2022 increased from 1.37 million tons in 2021 to 6.8 million tons, Izmail – from 4 million tons to 8.9 million tons, Ust-Dunaysk – from thousand tons to 785 thousand tons.

The port of Izmail has become the main export route for ferrous metal industry: 45% of ferrous metal products are exported through this port (data as of October 2022). The main directions of shipment from Izmail are the port of Constanta, Burgas (Bulgaria) and transportation along the Danube.

“Before the conclusion of the grain deal, our logistics through the Ukrainian Danube ports was impossible, since they were occupied with grain cargo. After the opening of the grain corridor, we were able to partially switch our imports to these ports,” notes Sergiy Krut, CEO of Metal Holding Trade.

In general, according to recent GMK Center’s research, the amount of losses from the blockade of seaports reaches $ 420 million per month. Every month, Ukraine cannot produce and export 1.3 million tons of iron ore, 151 thousand tons of pig iron, 192 thousand tons of semi-finished products and 218 thousand tons of finished steel products.

Port problems

For the first time after the start of the blockade, Ukrainian mining companies studied the effectiveness of new logistics routes, making test export deliveries.

“We studied the possibility of lengthening the delivery time to ports and calculated the costs of shipping products from the ports of Germany, Belgium, Holland and the Adriatic. The lengthening of the shoulder had a negative impact on the cost of delivery. Transit countries were added with their own transit conditions, transit rates, which significantly increased the cost of delivery per 1 ton of cargo. Profitability became negative,” says Andriy Myagkov.

Companies in the industry were forced to change the ports of unloading cargo due to the economic component of logistics.

“The port terminals of Germany, the Netherlands, the Baltic countries were under study, but they refused to work with these terminals due to the higher cost of logistics than in Poland and in the direction of the southern ports, as well as due to the lack of a sufficient number of rolling stock for the delivery of goods to the terminals of Germany, the Netherlands, the Baltic countries. Rolling stock operators were not ready to give their wagons for long routes outside of Poland and were mainly focused on the rapid turnover of wagons over short distances,” notes Metinvest.

Port of Constanta

According to the GMK Center, the Romanian port of Constanta is currently the main seaport for Ukrainian iron and steel exports. Ukrainian products are brought to Constanta by road and rail, as well as by barges from the Ukrainian Danube ports of Reni and Izmail. The export of iron ore through Constanta started in May 2022. According to the port, sea and river transportation through Constanta of iron ore and various types of steel products for the period from February 24 to October 5, 2022, amounted to 1.3 million tons.

On the other hand, Centravis refused to use Constanta in 2022 due to too high workload and constant transfers of loading/unloading of the company’s containers. Also, logistics through this port is complicated by problems with the railway infrastructure and the summer-autumn low water level on the Danube, which does not allow barges to accept a full load.

At the beginning of 2022 it was impossible to transport cargo to Odesa. Forteks mainly considered ports in Romania and Turkiye, but both of these options eventually disappeared.

“At the start of the war, there were long queues in the ports of Romania and Turkiye, as well as difficulties with the export of steel by road and the lack of access to the railway in Turkiye. The workload was very high in Constanta: the cargo could stand for more than a month, waiting for unloading, and this is an extra cost. As a result, they decided to redirect those ships that come from China and India to Gdynia and Gdansk, and one ship that was already in the Black Sea was unloaded in Constanta. Now we ship our cargoes to Gdansk, as the efficiency of the ports in Poland is higher, and the number of days of free downtime is 3 times more (21 days of free storage instead of 7 in Romania). In addition, it is convenient to deliver the goods to a warehouse in Lviv later,” says Oleksiy Didenko.

According to Metinvest, first of all, the ports of Europe are focused on imports and have not previously worked with steel cargo, in particular with pig iron and billets (a new type of cargo, new technology, large volumes). As a result, there is a shortage of personnel, equipment for transshipment (loading/unloading), storage space for the accumulation of ship lots.

“By mid-2022, due to long queues both at the border and at the approaches to ports, additional costs arose due to idle wagons, storage of goods awaiting transshipment at terminals, idle ships,” Metinvest emphasizes.

In turn, Centravis faced the following logistical problems in 2022:

- lack of space in the repacking warehouses due to the high load on European ports (a large influx of cargo, including from Ukraine);

- high traffic in US ports. Vessels with containers arrived in the United States and stood in front of the ports for a long time at anchor, waiting for mooring and unloading.

Iron dead end

After the blocking of seaports, a significant part of Ukrainian exports moved to the railroad. Rail traffic through western border crossings grew significantly in 2022:

- export – by 12.4% y/y, up to 34 million tons;

- imports – by 71% y/y, up to 5.8 million tons.

At the same time, it quickly became clear that neither the Ukrainian nor the European railway infrastructure was ready to accept and process the available volume of cargo from Ukraine.

“Everyone, without exception, faced the problem of limited capacity of European ports. The ports were not ready for a multiple increase in demand, the port and railway infrastructures could not cope with the influx of cargo,” Andriy Myagkov explains.

Rail transportation is possible through 13 railway border crossings with European countries: Poland, Slovakia, Hungary, Romania and through Moldova to Romania. The volume of rail freight traffic between Ukraine and Poland increased by 36.7% y/y last year – up to 16.9 million tons of cargo, and between Ukraine and Romania – almost twice, up to 3.3 million tons.

Five crossings are most actively used for the export of steel products: Chop-Cherna and Uzhgorod – to Slovakia, Izov and Mostyska-2 – to Poland, Batevo – to Hungary. In total, they account for 94% of exports by rail. According to the GMK Center, the share of rail transport in the export transportation of steel products was 40% as of October 2022.

The main infrastructure problems for Ukrainian exports in 2022 include the following:

- Limited capacity of border crossings and certain sections of European railways. The main problem is the different railway gauges in Ukraine and Europe and, accordingly, the need to rearrange the wagon bogies. According to Ukrzaliznytsia, the nominal capacity of all border crossings is more than 3,400 wagons per day, while according to GMK Center – 1,800;

- Initial lack of integration between the railway structures of Ukraine and neighboring countries;

- Lack of wagons from European rail carriers;

- Lack of sufficient transshipment capacity at the border;

- Duplication of control procedures in Ukraine and European countries.

All this led to the fact that raicars with export products stood in lines at the border of Ukraine with the EU (their peak was in June last year – more than 40 thousand wagons), as well as in European ports. According to Ukrainian iron and steel companies, during this period, queue delays were up to 60 days. By the end of 2022, the problem of wagon queues has slightly eased, but the issue of capacity at the border will again become relevant with the improvement in the global commodity markets and the growth in demand for rail transportation.

Also, Ukrainian exporters must take into account the cargo flows of European countries. For example, in Poland, an important indicator is coal cargo flows. At the end of 2022, the Port of Gdansk increased coal transshipment by 2.75 times y/y – up to 13.2 million tons, oil – by 34.9% y/y. However, part of the cargo flow of imported coal will go to the ports of the Baltic countries, in particular to Riga, where there are reserves of transshipment and storage facilities.

According to the GMK Center, the companies of the Ukrainian iron and steel complex associated certain hopes with deliveries through the ports of Lithuania, in particular Klaipeda. However, they have not been implemented yet: in order to deliver the wagons to Lithuania via Poland, the bogies will have to be changed twice, because Poland has a narrow gauge, while Lithuania has a wide one. There are two options for solving the problem: the construction of a wide railway track in Poland to connect the borders of Ukraine and Lithuania, as well as the creation of a platform for rearranging wagons on narrow bogies in Lithuania. However, Poland does not want to build a 300 km wide railway, the transition cannot take place without EU co-financing, but the EU plans do not provide for subsidizing the expansion of railway infrastructure.

Export on wheels

Before the full-scale war, road transport for the transportation of ferrous metal products was not widely used. However, in the face of restrictions on the supply of iron and steel products by sea and by rail, companies in the industry partially switched to exporting products by road. Total road transport exports grew by 32.4% y/y in 2022 – up to 12 million tons.

Trucking of steel products

“We mainly use vehicles. After the start of a full-scale war, we tried the railway, but it is unprofitable and not very convenient,” notes Andriy Krasyuk, CEO of production at Centravis.

The following checkpoints are mainly used for export: Yagodyn – Dorogusk (Poland), Rava-Ruska – Grebenne (Poland), Krakovets – Korkhova (Poland), Shegini – Medyka (Poland), Chop (Tysa) – Zakhon (Hungary), Uzhgorod – Vyshne Nemecke (Slovakia). Most of the cargo passes through Poland, as this country is a transit point for delivery to most countries in northern and western Europe.

“If earlier our containers went to Odesa, now we have moved to Gdansk and Gdynia, to a lesser extent – to Rotterdam and even Hamburg. From there, we already transport by road and to a lesser extent on railway platforms,” notes Sergiy Krut.

The growth in the use of motor vehicles was also facilitated by the fact that by the end of 2022, the supply of road transport to Europe and from the EU countries increased, and the cost of auto delivery decreased (compared to the first months of the war).

On the other hand, last fall, shippers faced long queues at road border crossings, which led to delays in transit. According to the GMK Center, trucks stood at checkpoints for 2 to 5 days, and the average delivery time to EU countries at the end of last year was 10-15 days.

Logistical difficulties

The war forced iron and steel companies to completely rebuild their export logistics. According to the results of GMK Center’s research (as of November 2022):

- the cost of delivery of Ukrainian steel products to the port of destination increased by an average of 3-4 times;

- the average distance to the port of departure for Ukrainian exporters increased by 5 times;

- Ukrainian steel products are delivered to European buyers by rail in an average of 18 days.

All opportunities for Ukraine to increase the production and export of ferrous metal products are associated with access to ports. Even during the war, 60% of steel products from Ukraine are delivered to end consumers by sea. Therefore, an increase in the load and production of Ukrainian steel enterprises, the restart of idle capacities, and an increase in exports are possible only if Ukrainian Black Sea ports are unblocked.

-

OpinionsIndustrysteel consumption

13 July 2026

16 July 2026

24 June 2026

18 June 2026