Opinions Industry macroeconomics 451 28 May 2026

The impact of the war in the Middle East on Ukraine’s economy in 2026: the NBU’s perspective

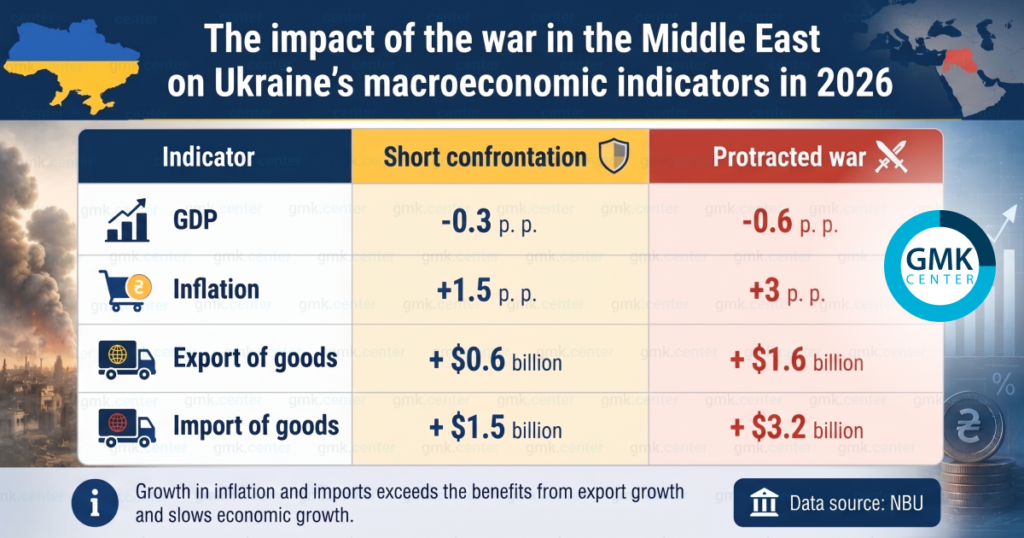

Depending on the scenario, the direct impact of rising energy and fertilizer prices is estimated at $1.5–3.2 billion

Volodymyr Lepushinsky, Deputy Governor of the National Bank of Ukraine (NBU), discussed the scenarios and potential impacts of the war in the Persian Gulf on the Ukrainian economy during his remarks at the online discussion “Global Signals – Implications for Ukraine: Economic Outlook 2026,” hosted by the Vox Ukraine think tank. The GMK Center presents the text of his remarks.

Current oil prices: context and risks

Hostilities and the blockade of the Strait of Hormuz (which accounted for 25% of seaborne oil shipments and 20% of LNG shipments prior to the war) have destabilized global energy markets, increased global inflation, and slowed economic activity.

Current oil prices, despite their significant increase, are not unprecedented from a historical perspective. The global economy has already been operating under comparatively high prices for a long time. Taking into account changes in the dollar’s purchasing power over the relevant period, current prices do not reach record levels.

At the same time, the risks remain significant. In particular, there is a likelihood of further price increases, as well as the possibility of the military conflict dragging on, which could lead not only to high prices but also to a physical shortage of energy resources. This combination of factors creates an extremely risky environment for global and national economies.

Forecast scenarios

We are considering two baseline scenarios.

- A time-limited conflict

The first scenario assumes that the military conflict will last for a relatively limited period of time. Starting in the second half of this year, a gradual downward price correction is expected—with Brent crude at $100/barrel in the second quarter and $80/barrel in the fourth quarter. However, it will take several years to return to pre-war price levels.

A certain natural compensator for Ukraine will be the rise in prices for domestic exports, primarily agricultural products. As global costs for agricultural producers rise, food prices will also increase, which will partially offset the negative effects for Ukraine. However, this factor will not be able to fully compensate for the losses from expensive energy sources.

- Prolonged and more intense price pressure

The second scenario envisages a greater impact on prices and more prolonged instability—with Brent crude at $150 per barrel in the second quarter and $100 per barrel in the fourth quarter. In a global context, this would mean a slowdown in growth among Ukraine’s major trading partners.

First and foremost, the revision of forecasts concerns the Eurozone, which is a net importer of oil and gas. Accordingly, its economic growth prospects are significantly deteriorating, and inflation will rise. Central banks’ monetary policy will become tighter.

Currently, most analysts believe that the current events will be of a temporary nature.

Impact on Ukraine’s economy

Inflationary effects

As an importer of energy resources, Ukraine is facing increased inflationary pressure from rising energy prices. An additional factor is the global rise in food prices. Secondary effects are already gradually emerging, but it will take up to six months for higher prices to be fully passed on to consumer prices.

Given the nature of supply shocks, the impact on inflation is expected to be relatively short-term. Against the backdrop of an already high base of comparison, inflation will begin to decline in 2027.

Impact on the real economy

Higher-priced energy and fertilizers will lead to a slowdown in economic growth. In particular, reduced fertilizer application due to high costs will, in the medium term, result in lower crop yields. An additional negative factor is the slowdown in growth rates in Ukraine’s major trading partners.

Foreign trade balance

The foreign trade deficit is widening. Depending on which scenario plays out, the direct impact of rising oil, gas, and fertilizer prices is estimated to range from $1.5 billion to $3.2 billion.

The deficit is partially offset by rising prices for Ukrainian agricultural exports.

Forecast indicators for the end of the year

The NBU has halted the cycle of policy rate cuts and is ready to respond to changes in external conditions.

The inflation forecast for the end of this year projects an acceleration to 9.4%. Currently, inflation is expected to remain below 10%, but this forecast may be revised due to changes in the underlying assumptions.

The relatively lower level of the indicator compared to initial expectations is primarily due to first-quarter results. The economic situation in the first quarter turned out to be worse than initial forecasts—mainly due to energy shortages and the destruction of critical infrastructure.

GDP growth for the current year is estimated at 1.3% year-on-year.

Despite the widening trade deficit, maintaining international reserves at a sufficiently high level provides opportunities to sustain the stability of the foreign exchange market and macrofinancial stability overall.