Posts Industry Ukraine’s iron and steel industry 6544 28 March 2023

Despite all the problems, industry enterprises are ready to restore production

The iron and steel complex of Ukraine suffered from the war significantly more than other sectors of the economy. Therefore, it is difficult to expect a quick return of production volumes from the industry to the pre-war level, since 40% of the steel capacities were seized or destroyed in Mariupol – steel plants Ilyich Iron and Steel Works and Azovstal. However, already now the key remaining enterprises of the industry are making plans to increase production compared to the difficult 4th quarter of 2022.

Signs of recovery

In 2022, the average annual capacity utilization of the industry was at the level of 30%, and in October-December it was only 15-20%. On average, steel enterprises were loaded by about 15%, mining – by 20%.

As electricity supplies stabilize, monthly production dynamics in early 2023 show the first signs of improvement in the industry. In February 2023, steel enterprises of Ukraine increased steel production by 49.3% m/m compared to January – up to 424 thousand tons, and the production of rolled products – by 30%, up to 334 thousand tons.

«The situation at the enterprises of the industry began to improve from the end of February, when there was an opportunity to stabilize the supply of electricity. This allowed enterprises to show the best results compared to the previous month. However, there was no significant increase in production volumes, as other problems remain unresolved, in particular, one of the main ones is logistical: the sea ports, through which in peacetime we exported 70% of steel products, remain closed to us, as before,» says Oleksandr Kalenkov, president of Ukrmetalurgprom.

Almost all enterprises in the industry work with different levels of workload. At present, the steel-smelting capacities of Metinvest’s enterprises are 60-65% loaded. For example, the Zaporizhstal steel plant in February 2023, compared to January, restored steel production by 32.8% – 119.4 thousand tons, rolled products – by 36.4%, up to 99.6 thousand tons. Also, in March, the enterprise began to withdraw blast furnace №2 from hot conservation and began to operate with three furnaces. The average current load of steel enterprises is 26%.

According to ArcelorMittal Kryviy Rih, the production situation has recently improved somewhat, but the level of capacity utilization still remains at the level of 25-30%. Industry enterprises are ready to increase production in conditions of stable electricity supplies and the allocation of sufficient limits.

“If electricity supplies are stable, and we maintain the logistical ability to transport products through Poland or southern Ukraine to Romania, we can return to the level of production at 50% of our capacity,” previously noted Mauro Longobardo, CEO of ArcelorMittal Kryviy Rih.

We can also note the restoration of mining facilities. Currently, all four mining and processing enterprises of Metinvest produce products and are loaded by 25-40%. The Group plans to increase the capacity of Minings to at least 30% of pre-war levels and focus primarily on the production of pellets.

In turn, Ferrexpo launched the second pelletizing line in March. In total, the company operates four lines. The current level of capacity utilization can reach 50%.

Taking into account the monthly dynamics (in February compared to January 2023), some indicators of steel products exports improved slightly:

- pig iron: growth by 31.1% – up to 177 thousand tons;

- iron ore: 31% increase to 1.2 mt;

- semi-finished products: growth by 80.6% – up to 69.2 thousand tons.

Despite logistical challenges and being close to the war zone, the industry has been able to adapt to difficult conditions and are making plans to resume production.

Factors to ensure the growth of iron and steel production in 2023

- Improved energy supply

After the autumn missile attacks on the energy infrastructure, as a result of which many steel enterprises were forced to suspend work, the situation has improved. The Ukrainian energy system has been operating for a month (with short interruptions in certain areas) without limiting the supply of electricity to all types of consumers. Now power generating enterprises have the necessary capacity to fully meet the needs of consumers.

- Debugging logistics

From the very beginning of the war, the steel companies faced the acute problem of reorganizing supply chains and introducing new logistics routes. In many ways, companies in the industry succeeded in rebuilding their export logistics through European seaports, Ukrainian ports on the Danube, to increase the use of vehicles.

- European restart

The main market for Ukrainian iron and steel products remains European, so the situation in the Ukrainian steel industry will largely depend on the economy of the EU. Ukrainian enterprises supply iron ore, semi-finished products and finished products to the European Union.

In 2023, European steelmakers will massively resume production at previously stopped blast furnaces and increase the output of steel products. According to the Platts agency, since the beginning of this year, nine large European companies announced about restarting or restoring capacities.

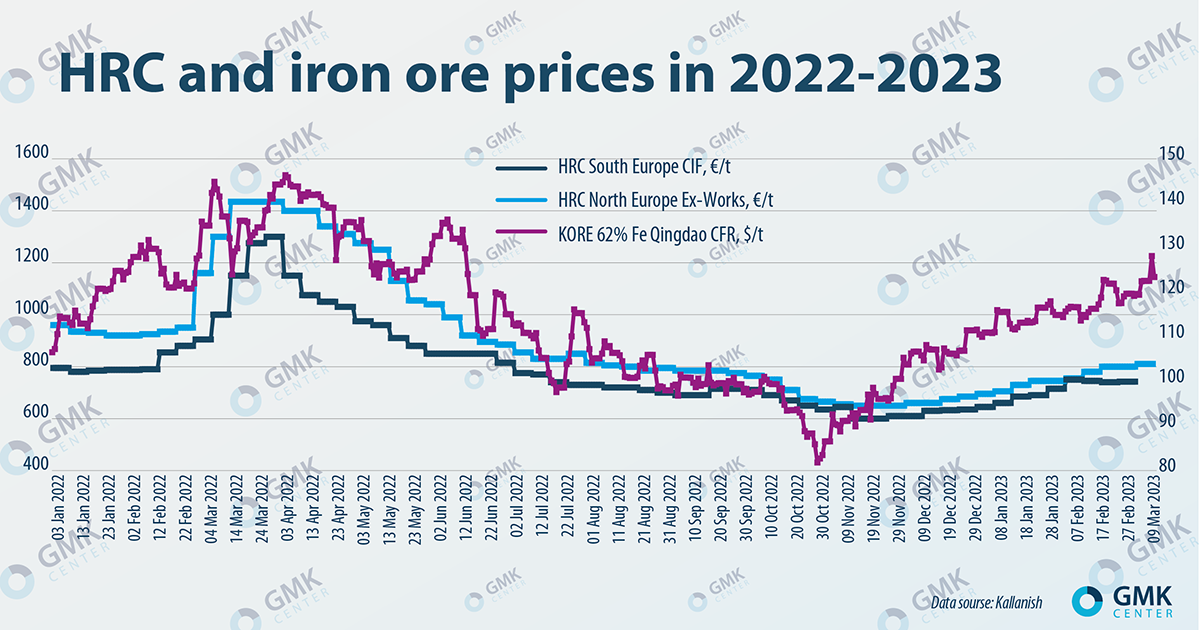

- Rising prices for steel and iron ore

The reason for the restoration of the work of European steel capacities is that by December European distributors had already depleted the stocks accumulated in the first half of 2022. The need to replenish balances leads to temporary shortages and higher prices.

According to Platts, European stelmakers say there are good portfolios of orders and stable demand, which allows for further price increases.

“Conjuncture on foreign steel markets has already partially improved, but global demand for steel products is unlikely to grow significantly until the geopolitical situation in the world stabilizes. Taking everything into account, I think that prices for steel products in the foreseeable future, if they grow, then only slightly,” emphasizes Kalenkov.

Amid a recovery in production, demand in Europe for iron ore is also increasing. The European market is a priority for Ukrainian iron ore companies due to the blocking of the Black Sea ports. Iron ore exports will also be supported by rising prices for raw materials, which is fueled by expectations of an increase in demand for steel in China. Analysts at Goldman Sachs predict possible iron ore prices to average $150 per ton.

Challenges and risks with a negative impact on iron and steel production in 2023

- Intensification of hostilities near production facilities

The main risk is the possible intensification of hostilities and the conduct of rocket and artillery attacks on the regions of Zaporizhzhia, Kryvyi Rih, Nikopol, Dnipro, Kamianske, where operating enterprises of the industry are located. This can lead to damage to production facilities and energy infrastructure, and stop logistics.

- Logistical difficulties

Logistics challenges remain the same as they were in 2022, when new logistics routes becoming longer and more expensive, limiting exports.

According to the results of GMK Center’s research (as of November 2022), the cost of delivery of Ukrainian steel products to the port of destination increased by 3-4 times, and the average distance to the port of departure for Ukrainian exporters increased by 5 times. In some cases, logistics costs have become equal to or exceed the cost of production.

Despite all the efforts of Ukrainian Railways (UZ) and the Ministry of Infrastructure, western rail and, to a lesser extent, road crossings, as well as access to European seaports remain a bottleneck.

Industry enterprises have partially redirected their exports and imports to Ukrainian ports on the Danube (Izmail), but their transshipment capabilities are limited. Moreover, in March, UZ imposed restrictions on the transportation of grain to Izmail due to the critical situation with the accumulation of wagons (the queue is 17 days).

The logistical problems of the industry will remain relevant until the opening of the Black Sea ports and for the export of iron and steel products, and not just the agro-industrial complex. According to the results of GMK Center’s research, blocking ports costs Ukraine $420 million in lost export earnings every month. The Ukrainian authorities are trying to agree on the inclusion of steel products exports in the grain deal, but there is no visible progress on this issue yet.

- Lack of staff

The industry faces the problem of shortage of personnel. Some of the employees became internally displaced persons or went abroad. A large part is subject to mobilization. At steel enterprises, approximately 8-12% of the current number of personnel were mobilized or became volunteers.

Companies are experiencing or may experience difficulties, especially when resuming production. In part, companies in the industry solve their problems with personnel through external recruitment, transfer of employees from other assets, or internal selection of employees within the same enterprise.

“Now the enterprises of the industry are working on only a small part of their production capabilities. At the same time, they try to prevent mass layoffs and continue to pay salaries to their employees. There is no acute shortage of personnel in the industry now, but after our victory and the opening of borders for men liable for military service, an outflow of personnel abroad is possible – many of them will want to reunite with their families, who have long settled in European cities,” explains Olexander Kalenkov.

- Scrap shortage

Due to the fighting in the industrial regions, where there was the highest share of the collection, the volume of scrap collection has significantly decreased. In 2022, this figure decreased by 75.9% compared to 2021 – to 996.7 thousand tons. Already in the first two months of 2023, scrap collection decreased by 70.7% y/y – to 152.2 thousand tons.

“Now there are no tools in sight to activate the collection of scrap metal. Mechanical engineering, for the most part, is idle, scrap collection capacities have been lost in a number of regions, and the personnel potential (people who collect scrap by hand) has decreased due to mobilization, emigration, etc. Therefore, forecasts for 2023 are not encouraging. In the optimistic scenario, the collection of scrap will be about 800 thousand tons, in the pessimistic scenario – 600 thousand tons. At the same time, the need for steelmakers in the base scenario will reach 1 million tons,” says head of the analytical center CMD-Ukraine Igor Guzhva.

In addition to everything, the export of scrap metal also increased. If in 2022 this indicator decreased by 11.4 times y/y – to 53.6 thousand tons, then in January-February 2023, exports increased by 3.5 times – up to 24.8 thousand tons. The general market situation in Europe contributes to an increase in the export of this raw material this year.

“The economy of scrap metal exports is becoming more attractive. The improvement in the European steel market and the rise in scrap prices in the EU countries up to €430-450 per ton creates good prospects for increasing scrap metal exports to Europe. At the same time, domestic prices are now at the level of €200-230 per ton. The increase in the price level has activated the harvesting market, but domestic demand has not grown significantly, so we expect an increase in export deliveries,” – notes Volodymyr Bublei, president of UAVtormet.

Export growth threatens with a shortage of raw materials for Ukrainian steel plants, which are making plans to resume production. Unfortunately, from March 16, the plant Interpipe Steel has already suspended work due to a shortage of scrap metal. According to Olexander Kalenkov, as a result of a drop in the level of scrap collection and an increase in the export of this strategic raw material in the second quarter of this year, we expect a shortage of scrap at the level of 100 thousand tons, and now these warehouses are empty.

“The export of scrap metal from Ukraine is simply disastrous for our steel enterprises. It is possible that they will not be able to produce the planned volumes of steel. In the worst case, we will have to stop the power. Therefore, the situation is complicated, it is necessary to make decisions at the state level, up to a return to the idea of banning exports for the period of hostilities. Moreover, the state needs to strengthen control over the fact that the scrap supplied to the EU is intended for the end user. The fact is that often exports to the EU are purely nominal in order to get rid of duties, since raw materials are subsequently re-exported, possibly to Turkiye. This is a task for diplomats, trade investigations are not ruled out,” Guzhva emphasizes.

The potential of iron and steel complex of Ukraine

Despite the war and the loss of capacity, strategic investors see potential in the Ukrainian steel sector, and the industry of green steel after the war is able to attract tens of billions of dollars of investment. It is expected that in the conditions of post-war recovery, Ukrainian steel industry will be modernized to better standards. However, for this, it is already now necessary to take care of the guaranteed availability of raw materials – scrap metal.

The post-war reconstruction of Ukraine will require a huge amount of steel products. Therefore, it is already important for the industry to receive support in the form of opening ports for export, extending the regime for the abolition of trade restrictions in the markets of developed countries, reducing logistics and energy tariffs, etc. Enterprises in the industry can restore production, which will automatically increase foreign exchange earnings and revenues to budgets, and will help strengthen the exchange rate of hryvnia and employment growth, will create a positive multiplier effect for other sectors of the economy.

-

OpinionsIndustrysteel consumption

13 July 2026

21 July 2026

16 July 2026

24 June 2026