Posts Industry Ukraine’s iron and steel industry 18 16 July 2026

Ukraine celebrates Metallurgists’ Day

For the fifth year running, full-scale war has been putting Ukraine’s iron and steel inudustry – the true ‘economic backbone’ and mainstay of our state – to the test. Although production volumes have fallen by two-thirds compared with the pre-war period, the sector is showing signs of a difficult but steady stabilisation. Steel enterprises remain among the largest taxpayers, employers and investors, sustaining regions near the front line. The iron and steel sector not only finances defence and generates foreign currency revenue, but also directly supplies special-purpose steel to the defence industry.

The sector is currently forced to adapt to international protectionism, strict European quotas and carbon border adjustment mechanisms (CBAM). At the same time, companies continue to invest in sustaining production, creating unique ecosystems for the reintegration of veterans, whilst simultaneously overcoming an unprecedented labour shortage and energy challenges.

The backbone of the economy

As the full-scale war enters its fifth year, Ukraine’s steel industry is in a state that is difficult to define in a single word. Companies are striving, at great cost, to stabilise production volumes at a level three times lower than pre-war levels.

In 2025, Ukrainian steel companies increased production of pig iron and rolled steel by 11.2% year-on-year, to 7.9 million tonnes, and by 4.8% year-on-year – to 6.5 million tonnes respectively, whilst steel production over the same period fell by 2.2% year-on-year – to 7.4 million tonnes.

According to data from the Ukrmetallurgprom, Ukrainian steelmakers exported 4.1 million tonnes of steel products in 2025, a decrease of 1.1% year-on-year. The lion’s share of steel exports (82%) was destined for European Union markets.

However, despite everything, the iron and steel sector remains one of the largest and most important sectors of the Ukrainian economy. In 2025, the iron and steel sector accounted for 5.5% of Ukraine’s GDP — down from 7.2% the previous year, but this decline is attributable to objective factors: a reduction in steel production and iron ore mining, as well as the closure of the Pokrovske Mine, which had previously supplied 66% of the domestic coking coal market. Exports of iron and steel products reached $6.2 billion last year, or 15.2% of the country’s total exports.

The sector’s fiscal contribution is also significant: in 2025, the five largest steel companies paid $0.9 billion in taxes to budgets at various levels, equivalent to 1.4% of the country’s total tax revenue.

No less important is the sector’s indirect impact on the budget — through the multiplier effect of economic activity that it generates.

“The iron and steel sector generates a powerful multiplier effect in the economy: one job in the sector creates 7–8 additional jobs in related sectors. Accordingly, the sector’s contribution to the state budget consists not only of direct taxes paid by enterprises, but also of revenue from logistics infrastructure (Ukrainian Railways, ports) and tax receipts from a wide network of contractors and counterparties,” notes Oleksandr Kalenkov, President of Ukrmetallurgprom.

A healthy industry: why OECD recognition matters

In the spring of 2026, the Organisation for Economic Co-operation and Development (OECD) finally updated its statistics on Ukraine. It revised down its official estimate of our steel production capacity from 38.7 million tonnes to the actual figure of 8 million tonnes per year.

Why is this important? There is a huge global surplus of steel production capacity, which is why other countries (notably the EU) protect their markets with tariffs and quotas. For years, international reports had been citing outdated figures for Ukraine. Until 2014, we had 12 steelworks in operation; after 2014, nine remained; and after 2022, only six. Many enterprises have been destroyed or lost, and their restoration would require investments running into the billions, which are impossible during the war. However, documents still listed our capacity as enormous (42 million tonnes), even though actual production barely reached 7.4 million tonnes.

This overestimation of production capacity was detrimental to Ukraine. Now that the OECD has officially recognised the true state of affairs, it will be much more difficult for other countries to close their markets to Ukrainian steel products through trade restrictions.

Investment against all odds

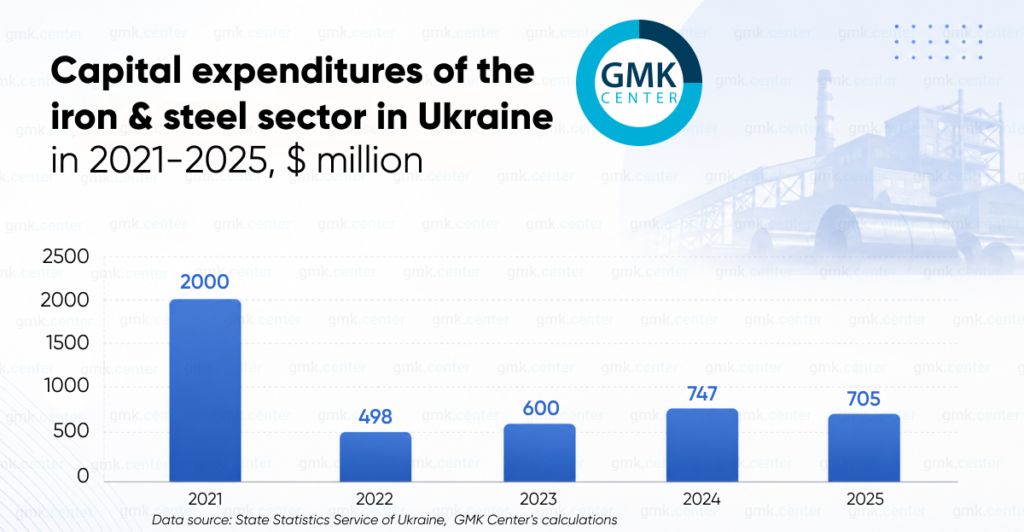

The Ukrainian iron and steel sector continues to invest significantly. According to GMK Center estimates, capital expenditure by Ukrainian iron and steel companies amounted to $705 million in 2025 (-5.5% year-on-year), and $126 million in the first quarter of 2026 (-7.0% year-on-year). Overall, the sector accounts for around 17% of total capital investment in industry.

Companies are channelling funds towards energy independence and maintaining production capacity. These are not development investments in the traditional sense — for the most part, they are investments aimed at sustaining current operational activities

Companies are channelling funds towards energy independence and maintaining production capacity. These are not development investments in the traditional sense — for the most part, they are investments aimed at sustaining current operational activities

Although a significant number of development projects have been put on hold due to the war, companies in the sector are not ceasing to think about the future.

Ukraine possesses some of the world’s largest reserves of magnetite ore (5 billion tonnes), suitable for beneficiation to an iron content of 68–70%; it has the potential to supply up to 20 million tonnes of raw material for DRI production to the global market each year. Combined with the expected demand for steel for post-war reconstruction — estimated at 1–3 million tonnes annually — this provides additional long-term motivation to preserve and develop production capacity today.

«Ukraine will play a key role in the green transformation of the EU steel industry. Ukraine can ensure the supply of DR-pellets to new DRI/EAF plants producing green steel in the EU. According to our estimates, Ukraine can supply 5–7 million tonnes of high-quality raw materials to modern European enterprises,» notes Stanislav Zinchenko, CEO of the GMK Center.

However, the start of 2026 has already shown just how fragile any positive momentum in the sector is. Due to the CBAM, Ukrainian steelmakers lost over 1.1 million tonnes of export orders from the EU in the first quarter of 2026, leading to a reduction in production and job losses in the sector. In particular, ArcelorMittal Kryvyi Rih cut 3,400 jobs in its foundry and mechanical production facilities and in the blooming mill. The company’s planned capital expenditure for 2026 will fall by 23% year-on-year, to $108 million.

A second setback came on July 1, when the EU introduced a new steel import safeguard regime. Under the new system, the country-specific quotas allocated to Ukrainian suppliers are about 60% below their actual shipment volumes in the corresponding product categories in 2025. Ukraine’s annual losses from steel exports could reach 1.3–1.5 million tonnes.

It is important to emphasise that these losses (from the CBAM and import quotas) are linked to regulatory changes in the EU, which is the main destination for exports of steel products. In other words, Ukrainian companies have no direct influence over these factors and are currently unable to make decisions that would offset this negative impact.

At the same time, companies state that even under severe pressure, they will continue to invest in maintaining equipment and in specific development projects, as this is a key condition for remaining competitive in export markets.

Social safety net: wages and veterans’ programmes

The iron and steel sector traditionally offers the highest wages among Ukraine’s industrial sectors — and this is one of the main factors retaining skilled workers in industrial regions near the front line. According to the Federation of Metallurgists of Ukraine, the average wage at companies in the sector rose by 7% to nearly 30,000 UAH — 20% higher than the national average at the end of last year. As a rule, every spring, companies in the sector carry out campaigns to increase their employees’ salaries by an average of 10–15%, which is higher than the rate of inflation.

Steel companies are consciously creating attractive working conditions by investing not only in the wage bill but also in production safety — a factor that is critically important given the constant shelling of energy and industrial infrastructure.

A distinct and, arguably, the most humane aspect of the iron and steel sector’s social responsibility is its systematic work with veterans. Companies in the sector are recognised leaders in this field.

Interpipe’s veteran reintegration programme was recognised in 2025 as the country’s best HR project (HR Brand Award). Its greatest strength lies in rejecting one-size-fits-all solutions in favor of a highly personalized approach. The company’s support service, which has evolved from a volunteer headquarters in 2014 into a fully-fledged department with permanent staff, a budget and clear responsibilities, provides individual support for every serviceman. Once servicemen return to civilian life, the company provides comprehensive medical, legal and psychological support. The service currently looks after nearly 1,500 people, and the company now employs over 200 veterans in total.

Metinvest, one of the largest private employers of demobilised personnel in Ukraine, has established a comprehensive reintegration ecosystem covering medical, psychological and physical rehabilitation, social adaptation, retraining, legal support and financial assistance. Veterans have access to free education and retraining at Metinvest Polytechnic, the company’s own university.

ArcelorMittal Kryvyi Rih’s veteran reintegration programme is one of the key elements of the plant’s social strategy. Hundreds of veterans have already returned to the company, where a comprehensive support ecosystem is in place for them: ranging from individual medical care or physiotherapy at the company’s own sanatoriums to psychological adaptation. A key advantage is the well-developed programme of retraining and free reskilling at the company’s modern training centre, which enables veterans to quickly master new technical professions or adapt their skills to civilian work.

Critical challenges

Despite these positive developments, the sector continues to operate on the edge of profitability due to two factors that industry experts and business leaders consistently identify as its greatest challenges.

- Energy shock.

Ukrainian steelworks pay the highest price for electricity in Europe — this is not a statistical anomaly, but a structural problem affecting competitiveness. According to estimates by the GMK Center, around 93% of steel in the EU is produced in countries where spot market electricity prices are lower than in Ukraine. This is particularly challenging for iron ore concentrate producers, as electricity accounts for up to 60 percent of their production costs.

Moreover, energy tariffs are constantly rising. For instance, from 1 July this year, Ukrenergo’s dispatch control tariff increased by 7.8%; this is already the third increase in electricity tariffs in 2026. A similar situation – high costs and constantly rising tariffs – is also observed in gas supplies to industrial consumers.

The energy crisis stems from extensive Russian attacks that have damaged power generation and natural gas production facilities, as well as electricity and gas transmission and distribution networks. Last year alone, the energy sector lost around 9 GW of generating capacity and half of its gas production volumes. This is forcing the country to import energy resources. Consequently, import prices are driving sky-high domestic tariffs.

The consequences have been substantial. Energy shortages and damage to Ukraine’s centralized power infrastructure have repeatedly disrupted production, forcing steelmakers to suspend operations and continually adjust their production schedules. Notably, Interpipe Steel’s EAF complex has been operating under persistent power shortages for the four months, beginning in late 2025.

- Staff shortage.

The second existential problem facing the sector is a staff shortage, amounting to around 20% of requirements. The reasons are twofold. Firstly, geography: most enterprises are located in frontline regions, from which there is a constant outflow of the population due to security risks. Secondly, mobilisation: the nature of heavy physical labour in the steel industry means that the sector has traditionally relied on a male workforce, and mobilisation processes are literally draining away skilled staff, whose training requires years of practical experience.

The challenge is compounded by periodic changes to, and interruptions in, the system that grants military service deferments to essential employees, including at companies officially designated by the Ministry of Economy as critical to the national economy. Industry representatives warn that without a stable and predictable deferment mechanism, enterprises may be unable to maintain full-scale operations or reliably fulfill defense contracts.

Instead of a conclusion

Ukraine’s iron and steel sector is not merely an economic sector. It represents tens of thousands of jobs in single-industry towns in frontline regions. It generates foreign exchange earnings that sustain the state and local budgets and fund defence.

At the same time, it is a literal component of national security — from the steel used for defence contracts to the taxes that fund the army.

‘The range of steel products manufactured by Ukrainian plants covers the entire range of products required for the construction of fortifications, as well as armour and special steels for the defence industry. Having our own production base mitigates the logistical risks and delays inherent in imports. Domestic production ensures direct and prompt deliveries, which is critically important for the defence sector,” emphasises Oleksandr Kalenkov.

For the fifth year running, the iron and steel sector has remained the country’s true ‘economic backbone’, whilst the nation has been living under conditions of full-scale war for the same length of time. The Ukrainian steel industry is currently characterised by its ability to simultaneously survive, invest and uphold social responsibility at a time when most of its global competitors receive state support, whilst Ukrainian enterprises are fighting for survival on their own.

To preserve this foundation for the country’s future recovery, the state should listen to the sector, first and foremost, on two key issues: a stable and predictable policy for retaining skilled personnel, and a fair tariff and energy policy that will work to support the competitiveness of the Ukrainian steel industry.

“Ukraine’s steel industry is part of the European market. Our iron and steel sector has a future, come what may. Proof of this lies in the unique production culture and technical expertise that have helped domestic steelmakers launch over 100 new product types into production since the start of the war. Incidentally, steel is a key material for recovery during the post-war reconstruction process. The iron and steel sector is, and will remain, the backbone of Ukraine’s economy!” — concludes Stanislav Zinchenko.

-

OpinionsIndustrysteel consumption

13 July 2026

24 June 2026

18 June 2026

15 June 2026