News Global Market iron ore prices 111 15 July 2026

Raw material offers (KORE 62% Fe/Qingdao) have risen again to three-figure levels following a decline in June

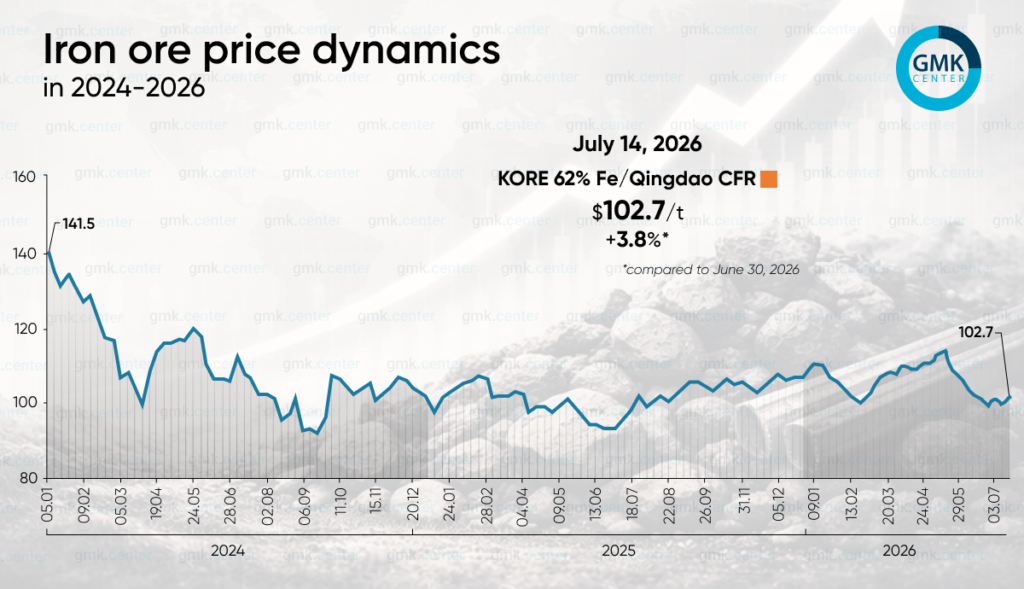

Prices for iron ore (KORE 62% Fe/Qingdao) had recovered to $102.73/t CFR as of 14 July 2026, following a sharp decline in June. In particular, at the end of last month, offers fell to their lowest level since August 2025 – $99/t CFR. The price is currently 3.8 per cent higher than on 30 June.

The first half of July was characterised by high volatility in the global iron ore market. Despite persistently weak fundamentals, prices managed to rise above the psychological threshold of $100/t due to a number of factors linked to supply risks and activity in China.

At the start of the month, the market remained under pressure from reports of further cuts to steel production in China. The deterioration in steelmakers’ financial results, driven by high coking coal costs and weak seasonal demand for steel, forced mills to cut production and postpone raw material purchases. Rising steel inventories and expectations of further accumulation of ore stocks in Chinese ports exerted additional downward pressure, whilst global supply remained sufficient thanks to high export volumes from leading producers.

At the same time, the market repeatedly received short-term support from news regarding potential supply disruptions. Initially, positive sentiment was driven by reports that China Mineral Resources Group (CMRG) intended to restrict the acceptance of certain low-grade Fortescue products, fuelling speculation about the availability of specific ore grades. Later, traders’ attention shifted to a possible strike by BHP workers at Port Hedland – one of Australia’s largest export hubs. Although market participants doubted that the protest would significantly affect physical deliveries, the very risk of disruptions supported futures prices.

Data from Chinese customs provided a further positive factor. In June, iron ore imports into the country rose by 15.3 per cent compared with the previous month, and by 6.3 per cent year-on-year for the first half of the year, confirming that purchasing levels remained high despite the challenging situation in the domestic steel market.

At the same time, long-term expectations remain subdued. Analysts forecast further pressure on prices due to an increase in global supply, particularly driven by new projects in Guinea, as well as the centralisation of China’s iron ore procurement through the CMRG, which strengthens the bargaining position of Chinese consumers.

In the near term, price trends will depend on how the situation surrounding BHP actually unfolds, the production policies of Chinese steelmakers, and the pace of restocking in China. If the risks of supply disruptions do not materialise and the reduction in steel output continues, the potential for further price rises will be limited, and prices are likely to fluctuate around the $100/t level.

-

Opinions Industry steel consumption

13 July 2026

15 July 2026

15 July 2026

15 July 2026