Posts Industry capital investment 221 24 June 2026

Investment in the steel sector rose by 40% y/y

In 2025, capital investment by Ukrainian iron and steel companies had risen for the first time since the start of the full-scale war, increasing by 17.5 per cent to $579 million. Companies were actively investing in energy independence, maintaining production capacity and even acquiring overseas assets. However, the start of 2026 brought new challenges: the introduction of the CBAM and trade restrictions are jeopardising further development, turning strategic investments into a fierce struggle for the sector’s survival.

Long-awaited growth

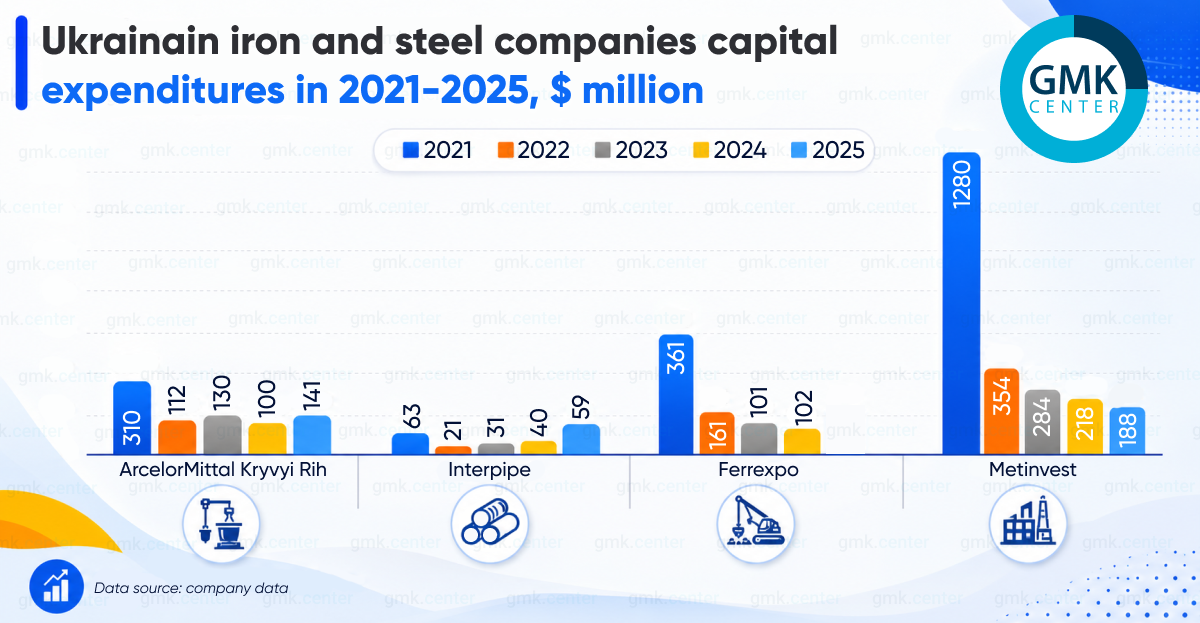

According to GMK Center’s estimates, capital expenditure by Ukrainian iron and steelncompanies rose for the first time since the start of the full-scale war in 2025. Last year, this figure rose by 17.5% year-on-year – $579 million. Capital investment in the steel sector jumped by 40% year-on-year – to $370 million, although investment in iron ore mining fell by 9% year-on-year – to $209 million. It should be noted that in 2021, before the war, these figures stood at $904 million and $942 million respectively.

In 2025, Metinvest Group invested $188 million (-14% year-on-year) in production capacity. Of this, $101 million (+25% year-on-year) was invested in steel production, and $85 million (-34% year-on-year) in mining operations.

According to Oleksandr Vodovoz, Head of the CEO’s Office at Metinvest Group, the company currently invests an average of $250–280 million a year in both projects to support production capacity and strategic initiatives, such as alternative energy. At the same time, against the backdrop of the war, Metinvest’s business planning horizon has been reduced to 2–3 months, as the Group’s enterprises operate in frontline regions.

The company’s largest investment areas in 2025 include the overhaul of the blast furnace at Kametstal, the implementation of a project to concentrate enrichment waste at SevGOK, and the enhancement of energy self-sufficiency, in particular the installation of gas piston power stations.

Metinvest’s priority for foreign investment is the construction of a ‘green’ steel plant in Italy. This country is the company’s main market, where it already operates two plants.

For its part, ArcelorMittal Kryvyi Rih’s capital expenditure rose by 42% last year — to $141.3 million from $99.6 million in 2024. The key areas of the company’s capital expenditure in 2025 were:

- Construction of the ‘Karta 3’ tailings storage facility — $33.6 million.

- Reconstruction of Quarry No. 3 — $9.5 million.

- Refurbishment of coke oven battery No. 5 — $7.6 million.

- Additional measures to improve health and safety performance — $7.3 million.

- Modernisation of the diesel locomotive fleet — $6.3 million.

Interpipe’s capital expenditure rose by almost 49% last year, to $59.4 million. The company completed the construction of a new heat treatment facility in Nikopol, with a total cost of over $40 million, and continued to invest in equipment for the finishing of pipe products.

However, the activities of companies in the sector – and, consequently, their investments – are hampered by administrative restrictions imposed by the state. In the case of Ferrexpo, the non-reimbursement of $80 million in VAT (as at the end of March) led the company to suspend operations at two pellet production lines back in May last year; it is now forced to seek ways to raise at least $100 million to support its working capital.

The non-refund of VAT was the direct cause of last year’s 47 per cent year-on-year drop in pellet output to 3.2 million tonnes. Due to issues with the audit of last year’s financial results, Ferrexpo has not publicly disclosed the level of capital investment for 2025. To put this into context: in 2023 and 2024, the company’s investments amounted to around $100 million, whereas in 2021, before the war, they stood at $361 million.

Investment trends

The main investment trends in the iron and steel sector during wartime can be summarized as follows:

- Funding to support production (repairs and maintenance), rather than strategic objectives.

“The Group continued to adopt a balanced approach to investment, based on the specific needs of each asset. In line with its priorities, maintenance accounted for 72% of total expenditure (82% in 2024), with the remainder allocated to strategic projects,” according to Metinvest’s report.

- A decline in investment in the mining sector.

This is due to the combined effect of numerous factors that are reducing iron ore mining activity. External factors include low prices on the world market, which have made the operations of some Ukrainian iron ore mines unprofitable. Internal factors include high electricity prices (the reason for the Ingulets Iron Ore Mine’s nearly two-year shutdown), logistical difficulties at the end of last year following shelling of port infrastructure, energy shortages and the failure to refund VAT to certain producers, causing them to lose working capital. Ultimately, iron ore production in Ukraine fell by 3.3 per cent year-on-year in 2025, to 43.2 million tonnes.

- Energy independence projects.

A new capital-intensive area of focus has been the financing of the procurement and installation of various types of generating capacity, together with the associated infrastructure. Metinvest has already installed gas-piston power stations with a total capacity of 29 MW at its facilities. Plans include the construction of solar power stations with a capacity of 37 MW. Other companies in the sector are also implementing similar projects.

- Acquisition of overseas assets.

With a view to expanding its presence in the European market and diversifying its production capacity, two landmark deals involving ArcelorMittal’s Romanian assets were concluded in December 2025:

- Metinvest acquired Tubular Products Iasi S.A., a plant specialising in the production of small-diameter welded pipes. Zaporizhstal plans to supply up to 180,000 tonnes of hot-rolled steel to this plant this year. This will enable the plant to resume its normal production rhythm, as ArcelorMittal has faced problems in recent years with securing raw materials (billet) to meet its needs. The plant’s output (maximum capacity: 240,000 tonnes of tubular products per year) will primarily be in demand on the Romanian market.

- Interpipe has signed an agreement to acquire Tubular Products Roman S.A., which specialises in the production of seamless pipes. The deal was finalised on 31 March this year.

Investment prospects in the sector

The outlook for growth in capital investment had already become significantly more uncertain by the end of the first quarter of 2026 than it had been at the start of the year. Due to the impact of the CBAM, Ukrainian steelmakers had already lost over 1.1 million tonnes of export orders for steel products from the EU in the first quarter. This has led to a reduction in production and job losses in the sector.

A second blow to the steel industry could come from the launch, on 1 July, of a new system of safeguard measures in the EU market. The final form of the document and the nature of this decision’s impact on the Ukrainian steel industry have not yet been determined; however, there is very little to suggest that the impact will be moderate.

The combined impact of these two factors could lead to a sharp fall in production and, likely, a decline in investment. For example, due to the CBAM, ArcelorMittal Kryvyi Rih has halted production at its foundry and mechanical production facilities, as well as its blooming mill. Furthermore, ArcelorMittal Kryvyi Rih’s planned level of capital investment for 2026 stands at $108.3 million, which is 23 per cent less than last year.

‘At present, we have no investment plans. The company’s strategic plan is to survive, spending between $100 and $150 million each year on standard investments. By ‘standard investments’, I mean those that ensure business continuity at current production levels. These are what we call ‘survival investments’,” says Mauro Longobardo, CEO of ArcelorMittal Kryvyi Rih.

However, halting investment under the current conditions means losing competitiveness.

“In 2026, we will once again be investing in new equipment. Investment is a key component of remaining competitive in our main export markets. Furthermore, investment in new markets and products is crucial in terms of development, certification and promotion. These are the investments that are not immediately visible in the short term but which must be made now, because ‘the train will leave’ and it won’t wait for us,” emphasises Vitaliy Sueta, Director of Products and Resources at Interpipe.

In the long term, the Ukrainian iron and steel sector will inevitably feel the effects of a lack of prior capital investment. The situation is complicated by the protracted war, the global trend towards protectionism and the CBAM. Under such conditions, any ongoing investment in modernisation is critically important: it is precisely these investments that lay the foundations for the future production capacity and competitiveness of Ukrainian enterprises.

-

OpinionsIndustrysteel consumption

13 July 2026

18 June 2026

15 June 2026

02 June 2026