Infographics Ukraine’s iron and steel industry 708 23 April 2026

Declining production, rising imports, and uncertainty surrounding the CBAM are jeopardizing the industry’s future

Ukraine’s iron and steel sector continues to be negatively impacted by the war, as evidenced by a further decline in production volumes and a reduction in the sector’s contribution to the country’s GDP. This is stated in the GMK Center’s study, “The contribution of the iron and steel sector to Ukraine’s economy in 2025.”

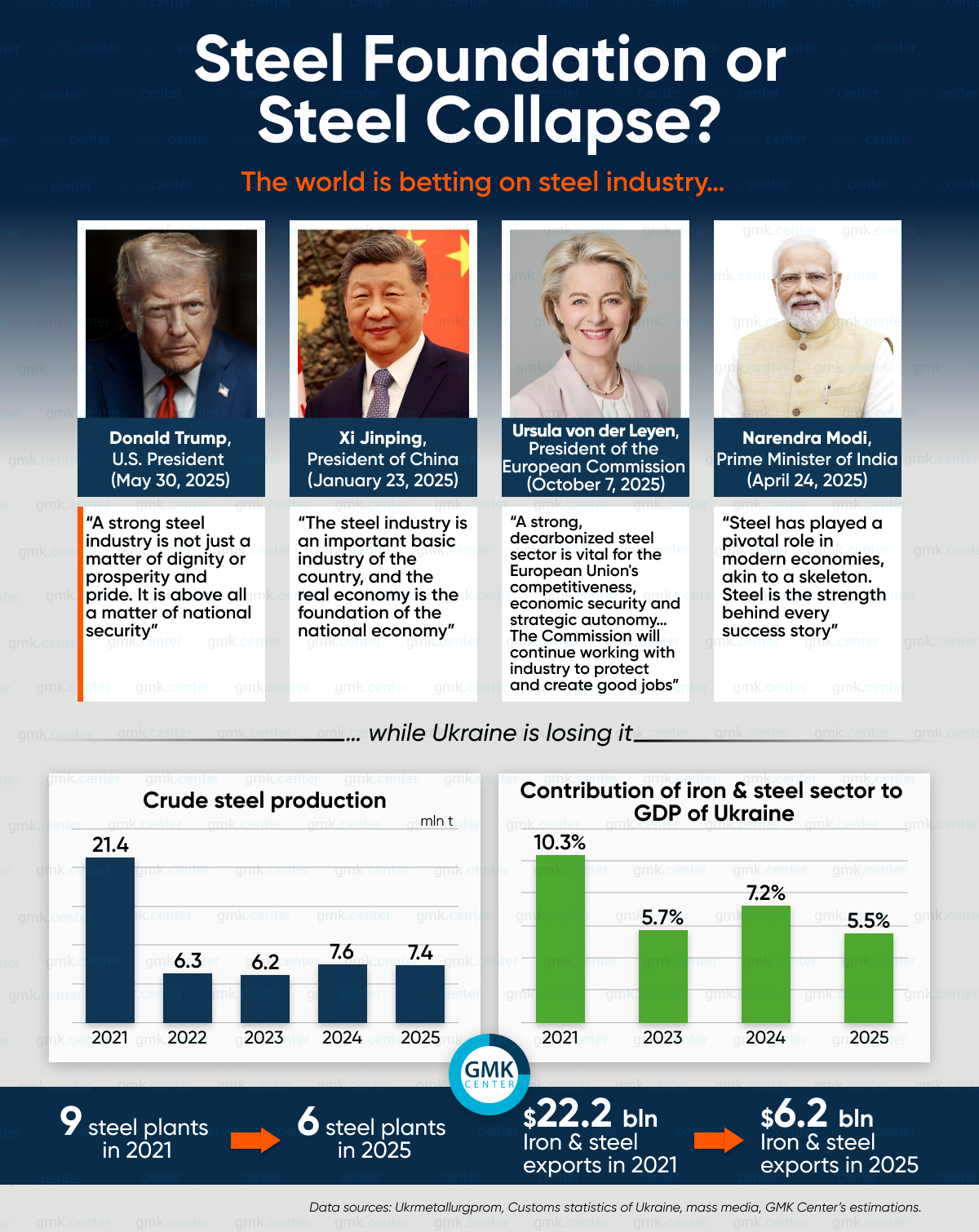

Steel production in Ukraine in 2025 fell by 2.2% – to 7.4 million tons, indicating a deterioration in the industry’s condition. This is 65.4% less than before Russia’s full-scale invasion, when nine steel enterprises were operating in Ukraine. Currently, only six such enterprises remain in territory controlled by Ukraine.

The iron and steel sector’s contribution to Ukraine’s GDP fell from 10.3% in 2021 to 5.5% in 2025. The main factors behind this decline in economic impact were reduced steel and iron ore production, as well as the suspension of coking coal mining in Pokrovsk. The Pokrovsk Mine Administration was the main source of coking coal in Ukraine, supplying 66% of the domestic market in 2024. As a result of its shutdown, Ukraine was forced to increase coking coal imports by 91.6% year-on-year in 2025.

Exports of products from Ukraine’s iron and steel sector in monetary terms in 2025 were 72.1% lower than in 2021 and 3.1% lower than in 2024. Chinese and Russian exports have displaced Ukrainian products from traditional markets in the Middle East and North Africa (MENA) region, Turkey, and other regions that were key destinations in 2024 following the opening of the “maritime corridor.” Currently, Ukrainian exporters, facing a wide range of challenges related to the war, are unable to compete effectively in global markets.

In 2025, in an effort to survive, Ukrainian companies had virtually no alternative but the EU—the only remaining key market. In 2025, the European Union absorbed 50% of all steel produced in Ukraine. The full implementation of the CBAM mechanism in 2026 calls into question the survival of Ukraine’s iron and steel industry, as Ukraine has not received any exemptions from this mechanism.

In the domestic market, Ukrainian producers are also facing growing competition from imports. Specifically, steel imports rose by 32.1% year-over-year in 2025 and by 19.0% in January–February 2026. In 2025, the share of imports in Ukraine’s steel consumption reached 40%, and in the first two months of 2026, this figure rose to 50.0%.

The decline of Ukraine’s steel industry is occurring against the backdrop of leading global economies—including the U.S., the EU, Canada, the UK, India, and China—actively supporting their national steel sectors through trade restrictions, CBAM, energy subsidies, and other forms of support. World leaders are increasingly emphasizing that steel sector is the foundation of national security and strategic economic autonomy, while Ukraine continues to lose its industrial potential.

-

Opinions Industry steel consumption

13 July 2026

20 July 2026

06 July 2026

01 July 2026