Posts Global Market sanctions 2087 18 September 2025

Some MEPs and steel companies demand to remove exemptions from sanctions against steel from Russian Federation

The EU continues to import Russian slabs, which is causing growing discontent among MEPs and European steel companies. Despite 18 sanctions packages, the EU remains dependent on Russian semi-finished products. In particular, in 2024 63% of slabs imports were from Russia.

In recent months, European politicians and industrialists have been demanding a complete ban on imports of Russian iron and steel products.

European sanctions impasse

According to experts, the European sanctions policy has many shortcomings. Part of these shortcomings stems from the EU decision-making procedure. When making general decisions, the EU is too often forced to make compromises, taking into account the positions of individual industries and countries that care about their economies.

A classic example is the import of Russian slabs. At the end of 2023, the 12th package of sanctions was adopted, by which the EU actually eased restrictions on imports of slabs from Russia, which had been imposed just a year earlier – in October 2022 as part of the 8th package. Initially, slab imports were supposed to stop on October 1, 2024, but they were postponed (given a new transition period) until the end of September 2028.

The main beneficiary of the relaxation of imports of Russian slabs is NLMK Europe (a subsidiary of Russia’s NLMK), which has five rolling facilities – two sites in Belgium and three plants in Denmark, France and Italy with a total capacity of 3.1 million tons of finished steel products per year.

Trade statistics only confirms this fact. The largest consumers of slabs from Russia in January-June this year were: Belgium – 688.5 thousand tons, Italy – 435.8 thousand tons and the Czech Republic – 370.3 thousand tons. In addition, Italy was the largest importer of Russian pig iron over the same period (524.6 thousand tons).

For their part, the authorities of the above-mentioned countries had previously supported the position of NLMK Europe in every possible way, arguing that they were concerned about the preservation of jobs and the economic condition of the regions. The company itself justifies its position by the impossibility to quickly find other suppliers with products having similar price and quality.а

However, the latter argument is disputed. According to Laurent Plasman, CMO of ArcelorMittal Europe, slabs are widely available on international markets, so there is no reason to keep importing Russian slabs.

Moreover, US Steel Košice refutes the claim that Russian slabs are unique and argues that there is substantial idle capacity in Europe to produce these products. Therefore, the only adequate argument in favor of Russian slabs is their low price compared to offers of other suppliers.

The situation is similar for the import of Russian pig iron to the EU (it will be discontinued from 2026). The annual quota for its supply to the EU in the amount of 700 thousand tons was exhausted at a record pace just in the first quarter of this year. The largest importers were approximately the same countries as in the case of slab imports – Italy (524.6 thousand tons), Latvia (87.3 thousand tons) and Belgium (31.1 thousand tons). It is noteworthy that European consumers were eager to buy Russian pig iron, while Ukrainian exporters were forced to supply their products to the USA.

However, despite the efforts of major companies and industry associations, the EU steel industry was unable to overcome the pressure of the countries beneficiaries of slab imports from Russia. The EUROFER Association has repeatedly opposed the expansion of supplies, as consumers of Russian slabs in Europe get a price advantage over other suppliers.

In particular, Russian slabs are processed in the EU and sold as European products, but at lower prices. The price difference with similar German products is up to 50%.

«While German companies are discussing overcapacity and even plant closures, Russia has increased its market share from 53% to 62% during the war,» emphasizes Gunnar Groebler, CEO of Salzgitter AG.

This inconsistent EU sanctions policy directly contributes to the financing of the Russian economy and the overall build-up of military capabilities directed against the EU, as well as disrupting competition in the European steel market.

Discussions on toughening sanctions

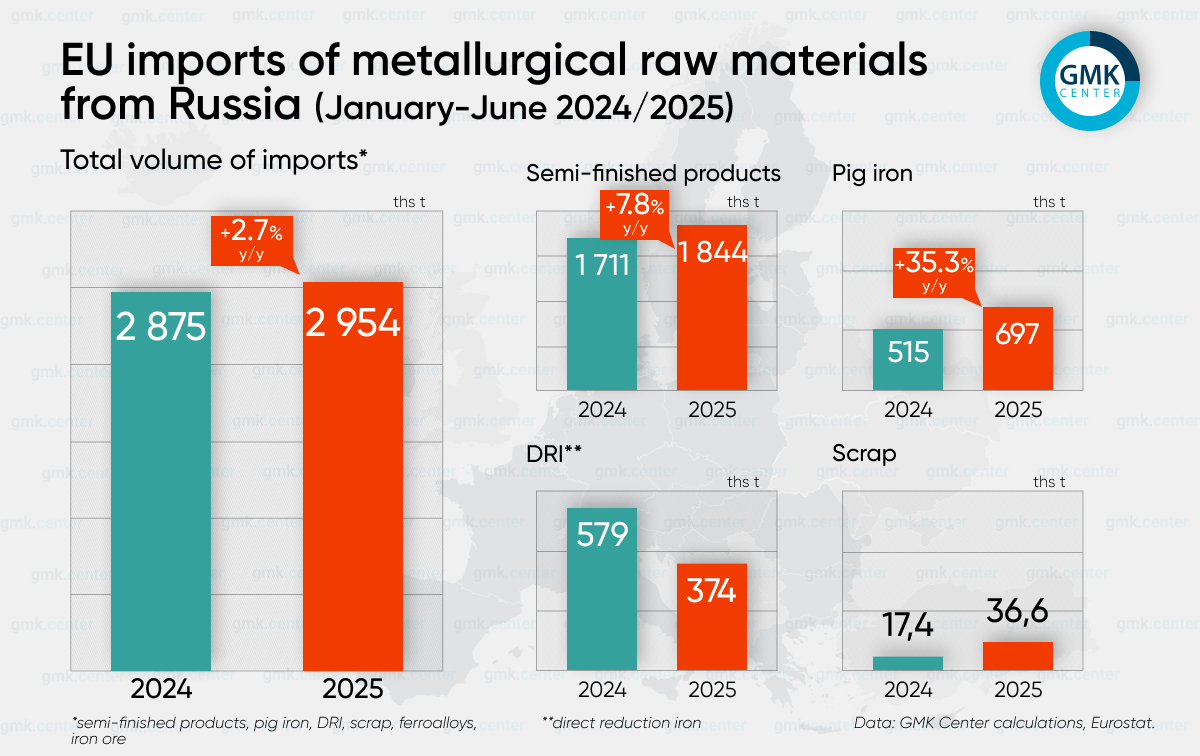

In 1H2025, the EU totally importedof 2.95 million tons (+2.7% y/y) of steel products from Russia worth €1.22 billion (-12.7% y/y). The key items of European steel imports from Russia in January-June were:

- semi-finished products (slabs) – 1.84 million tons (+7.8% y/y) worth €837.3 million (-5.6% y/y);

- pig iron – 697,000 tons (+35.3% y/y) worth €254.4 million (+21.9% y/y);

- direct reduced iron (DRI) – 374,200 tons (-35.4% y/y) worth €116.5 million (-41.2% y/y).

At present, the European steel industry is facing several huge problems at the same time, which put it on the verge of survival. These include high energy prices, an influx of cheap imports from Asia, a sharp increase in U.S. tariffs for European steel products and other factors.

Supplies of cheap semi-finished products from Russia only further imbalance the competition and worsen the positions of European companies. Therefore, European policy is increasingly calling for a revision of approaches to the import of Russian slabs.

On June 17, 2025, a group of 44 MEPs from different political factions sent a letter of concern to the President of the European Commission Ursula von der Leyen and the head of the European Council António Costa, calling for decisive action to completely ban imports of Russian steel products into the EU.

«The loophole kept for the import of certain quota of Iron and Steel Products from Russia is gross policy incoherence benefiting Putin’s regime and few industrial players, while harming peace, security and prosperity at large. It is laughing in the face of the European Steel Action Plan that European Commission presented earlier this year,» the letter said.

Similar statements are being made at the level of the European steel industry. Companies point out that it is immoral to support Russian imports of slabs against the backdrop of the war in Ukraine and the general situation in the European steel industry.

«It is simply outrageous that the EU continues to allow large-scale steel imports from Russia while our domestic industry suffers. We are cutting jobs and at the same time funding Russia’s war economy by buying slabs. I cannot explain this to any of my employees,» said Dennis Grimm, CEO of Thyssenkrupp Steel.

Industry representatives also criticize the practice of making the overall sanctions policy against Russian slabs weak and gutless because of the search for compromises with EU member states.

Accelerating the adoption of pan-European decisions, as a rule, requires the emergence and influence of strong triggers, which should have the character of a shock. The latest such fact was the flight of several dozen drones into Polish territory.

«As long as individual EU states insist on their exemptions, the system will remain intact. Europe is discussing 20 drones while transferring the funds that make these actions possible every day,» Gunnar Groebler explains.

The decision is overdue

This is not to say that the EU is not coming to the right conclusions and solutions. It just takes a long time to realize the problem and then to consult and agree on positions.

In the difficult market situation in the EU, the presence of Russian steel products is increasingly difficult to justify. At the end of last year, 63% of slab imports to the EU, or 3.15 million tons, were Russian products. In other words, the EU is heavily dependent on imports of semi-finished products from the very country it considers a threat to its security and against which it has imposed 18 sanctions packages.

«By continuing to import Russian slabs, we are pushing the European steel industry to stop production. Has importing Russian slabs become more important than protecting the European steel industry?» says Denis Parein, commercial director of ArcelorMittal Europe’s thick plate business.

Against this background, making a quick and unambiguous decision on importing Russian slabs is fully in line with the EU’s strategic autonomy and security objectives, which are reflected in the EU Steel and Metals Action Plan.

According to Kerstin Maria Rippel, Managing Director of the German Steel Association (WV Stahl), this loophole must finally be closed: if not by sanctions, then by effective EU tariffs on Russian slabs. The main thing is that this decision should not be drowned in endless discussions, which are so typical of the European bureaucracy.

-

OpinionsGlobal Marketmacroeconomics

28 May 2026

27 May 2026

20 May 2026

14 May 2026