Posts Global Market steel consumption 491 27 May 2026

Sales of finished steel are expected to rise to 1.72 million tons in 2026

The Norwegian steel market is resilient to external shocks. Its consumption pattern differs from the traditional pan-European model. Restructuring of procurement in key sectors creates a false impression of a decline. However, the economy’s actual steel intensity is on the rise.

Industry overview

The sole steel producer is the EAF plant in Mo-i-Rana. It specializes in rebar and wire rod, with a steelmaking capacity of up to 900,000 tons per year. It uses local scrap (100% self-sufficiency) and green energy from local hydroelectric power plants for production. Its products are considered among the most environmentally friendly in Europe—specific emissions amount to 0.2 tons.

The plant was previously known as Celsa Armeringsstål. In 2025, the Spanish Celsa Group sold its Scandinavian and British assets to the Czech company Sev.en Global Investments. The plant now operates under the 7 Steel Nordic brand.

Between 2021 and 2024, the Spanish company carried out a comprehensive pre-sale modernization at Mo-i-Rana.

* The EAF scrap charging system was completely reconstructed.

* The Hot Charging system has been implemented. Instead of being cooled in the storage yard, the hot continuously cast billet is transferred directly via an enclosed conveyor to the rolling mill’s reheating furnace. This saves tons of gas during the final reheating phase before rebar rolling.

* Baghouse filters with activated carbon injection were deployed to replace the legacy gas cleaning system, radically reducing fugitive emissions.

* The closed-loop water recycling system was upgraded with advanced filtration and cooling technologies, minimizing wastewater discharge into the Ranfjord.

At Celsa Armeringsstål, a digital footprint for finished products was introduced for the first time in Northern Europe. Now, a buyer (for example, a developer in Oslo) can use a QR code to see the exact amount of CO2 emissions for their specific batch of rebar. This allows the product to be sold at a premium for its environmental credentials.

The total investment in these projects amounts to €23.22 million, and in the context of decarbonization, they represent Best Available Technology (BAT). Sev.en Global Investments was directly involved in the hydrogen transition at Mo-i-Rana. Under its management, the plant commissioned a new rolling mill reheating furnace in 2025 capable of operating on both natural gas and hydrogen. The budget reached €28 million.

The 7 Steel Nordic plant is technically ready to receive hydrogen, but its supply on an industrial scale is delayed. The state-owned energy company Statkraft is responsible for the construction of the hydrogen hub at Mo Industripark (where the EAF plant is also located). It is postponing the launch due to the rising cost of electrolysers.

Until hydrogen is available in the required volumes, 7 Steel Nordic uses biogas for preheating steel, confirming its green status.

The impact of government policy

The government is not limiting itself to building hydrogen infrastructure for the steel industry (such as the aforementioned Hydrogen Hub Mo). It is prepared to fund up to 50% of the cost of any project that guarantees a radical reduction in CO2 emissions. The main instruments of this policy are:

- Enova, a state-owned fund under the Ministry of Climate and Energy. It provided €10.5 million for a new heating furnace in Mo-i-Rana as a grant. The state’s share of the project’s costs is 37.5%.

- The IPCEI (Important Projects of Common European Interest) program. Norway is part of the European Economic Area, so the national government funds industrial projects that have been granted IPCEI Hydrogen status. In particular, the chemical company Yara received €10.5 million to develop the production of green ammonia.

- The state-run Innovation Norway fund provides low-interest green loans and grants to medium-sized companies—such as steel processors Nordic Steel and Sverdrup Steel. Over the past 3–4 years, they have collectively invested €15–25 million in expanding production facilities, purchasing Bystronic automated laser cutting systems and robotic welding stations, and implementing Environmental Product Declarations (EPDs). The government co-financed these projects to make it easier for Norwegian companies to win international tenders.

- Compensation for industrial companies’ indirect CO₂ emissions costs (ETS Compensation) resulting from the addition of the cost of carbon allowances (EU ETS) to the energy tariff.

- The Hovedregelen mechanism. These are amendments to the Public Procurement Regulations (Anskaffelsesforskriften) and the Regulations on Procurement in the Utility and Energy Sectors (Forsyningsforskriften), approved by the Norwegian Ministry of Trade, Industry, and Fisheries in 2023.

Under Hovedregelen, in any public tenders (construction of roads, bridges, tunnels, hospitals), the weight of environmental criteria (carbon footprint) must account for at least 30% of the total bid evaluation. In this way, the state guarantees domestic sales for local producers who have invested in environmental sustainability.

Energy sector

Energy-intensive industries account for 40% of total energy consumption. These primarily include the aluminum plants of Norsk Hydro and Alcoa, as well as the ferroalloy plants of Elkem and Eramet. 7 Steel Nordic also belongs to this sector.

The residential and commercial sector consumes 55% of domestic energy. This high figure is due to the complete absence of centralized heating powered by natural gas or coal: individual electric heating is used almost everywhere. The remaining 5% goes to the transportation sector.

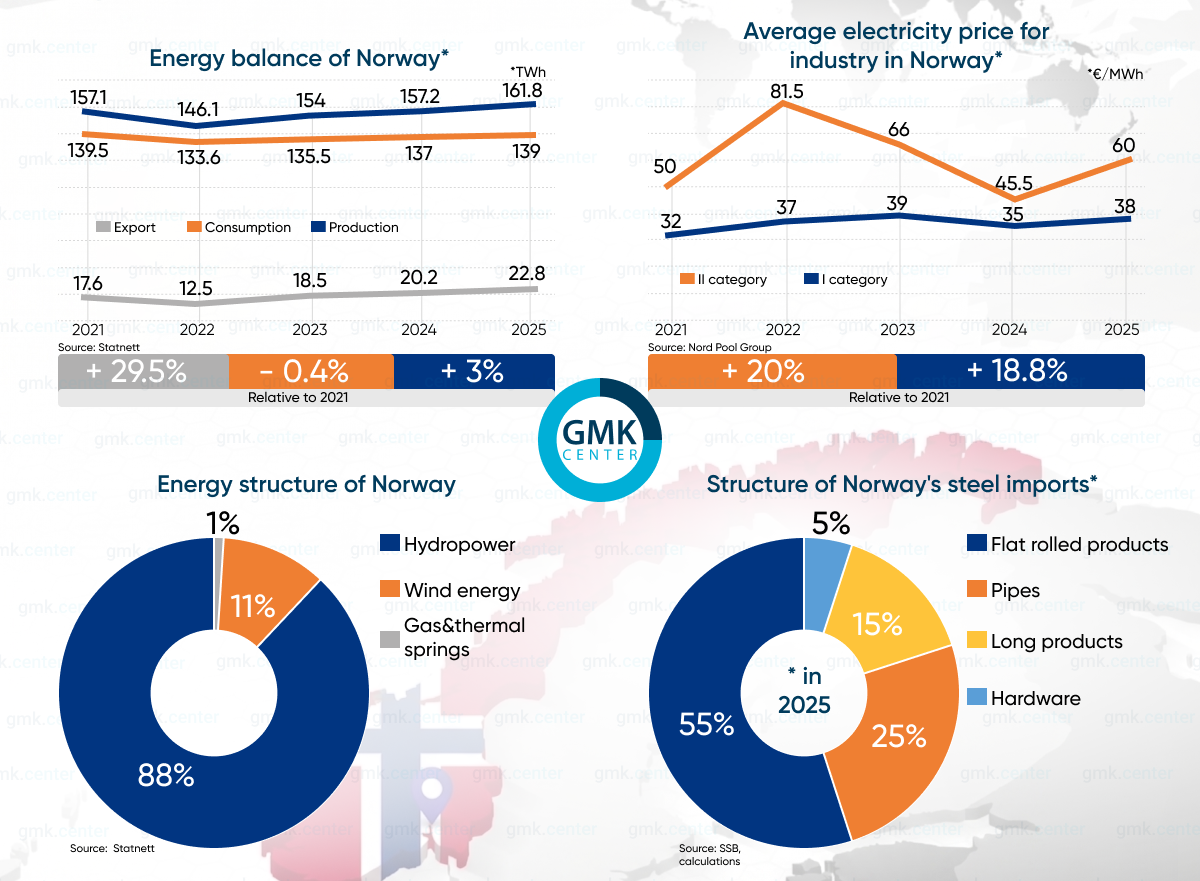

Hydropower is the backbone of the energy system, comprising about 1,800 hydroelectric power plants, plus a vast network of reservoirs. These account for approximately 50% of all pumped-storage capacity in Europe. The energy mix is stable, but electricity production fluctuates depending on weather conditions (precipitation and wind).

This led to a sharp decline in production and exports in 2022, which was an unusually dry year in Norway. In contrast, 2025 set a record for these metrics thanks to significant snowfall and rainfall early in the year. However, the country remains a stable net exporter of electricity even in relatively unfavorable years. For now, at least.

Consulting firm DNV notes that demand for electricity in Norway is growing six times faster than new generating capacity is being added. The domestic market is being filled by new customers: data centers and electrification projects for offshore oil and gas platforms. And soon, traditional industrial consumers, including 7 Steel Nordic, will have to compete for megawatts with the IT sector and the oil and gas industry. This will mark the end of the era of cheap electricity for Norway.

This is the main reason why the Scandinavian Blastr Green Steel project was split into two parts. Initially, the entire H2-DRI-EAF complex was supposed to be built in Norway. Later, it was decided to locate the EAF plant in Finland and keep H2-DRI production in Norway. Investors fear that by 2030, Norway could shift from being a net exporter of electricity to an importer during peak winter periods. This would undoubtedly “kill” the profitability of future hydrogen steel.

For now, the situation remains favorable for steelmakers. The surplus of cheap hydropower allows the plant in Mo-i-Rana to include a minimal energy component in the cost of steel.

Industrial consumers in Norway are divided into two categories. The first includes energy-intensive industries (7 Steel Nordic, aluminum and ferroalloy plants), and the second includes all others. The lower electricity price for Category I consumers is the result of long-term PPAs with hydroelectric power plants, signed 10–20 years in advance. This protects steelmakers from panic on the spot energy exchange.

An important feature of the Norwegian energy market is its geographical division. As in Sweden and Finland, the southern region (energy zones NO1, NO2, NO5) is connected to Germany and the UK, partially importing expensive European electricity from there. Zone NO4, where 7 Steel Nordic is located, is situated in the north. There is always a surplus of electricity here, as there are no overland power lines for export to Sweden or undersea lines to the UK and continental Europe.

In 2022–2023, the spot price in northern Norway could be €10–15/MWh. In the south, steel processors Nordic Steel and Sverdrup Steel paid €100/MWh, while German steelmakers paid up to €250/MWh.

Market profile

Norway is a net importer of steel. Demand for flat-rolled products and pipes is entirely met by foreign suppliers. The main sources are Germany, Sweden, the Netherlands, and the United Kingdom.

Shaped steel for construction is imported from Germany, from ArcelorMittal plants in Spain and Luxembourg, and from British Steel in Scunthorpe. Light-gauge shaped steel and special profiles come from SSAB plants in Sweden. Polish manufacturers supply prefabricated steel structures. Imports account for 80–85% of total steel consumption.

Norwegian steel exports have traditionally been focused on Sweden and Denmark. In 2025, shipments to Germany and the Czech Republic began. There, Norwegian rebar and wire rod outperform competitors thanks to their ultra-low carbon footprint.

The export breakthrough occurred after new owners took over Armeringsstål. At that time, the plant, now operating under the 7 Steel Nordic brand, was able to certify its products to the ČSN 42 0139 standard and win tenders to supply rebar for the construction of the Czech D11 and D35 highways. It is also used on construction sites in Prague, Brno, and Ostrava. Sev.en Global Investments has identified the Czech Republic as a new priority sales market.

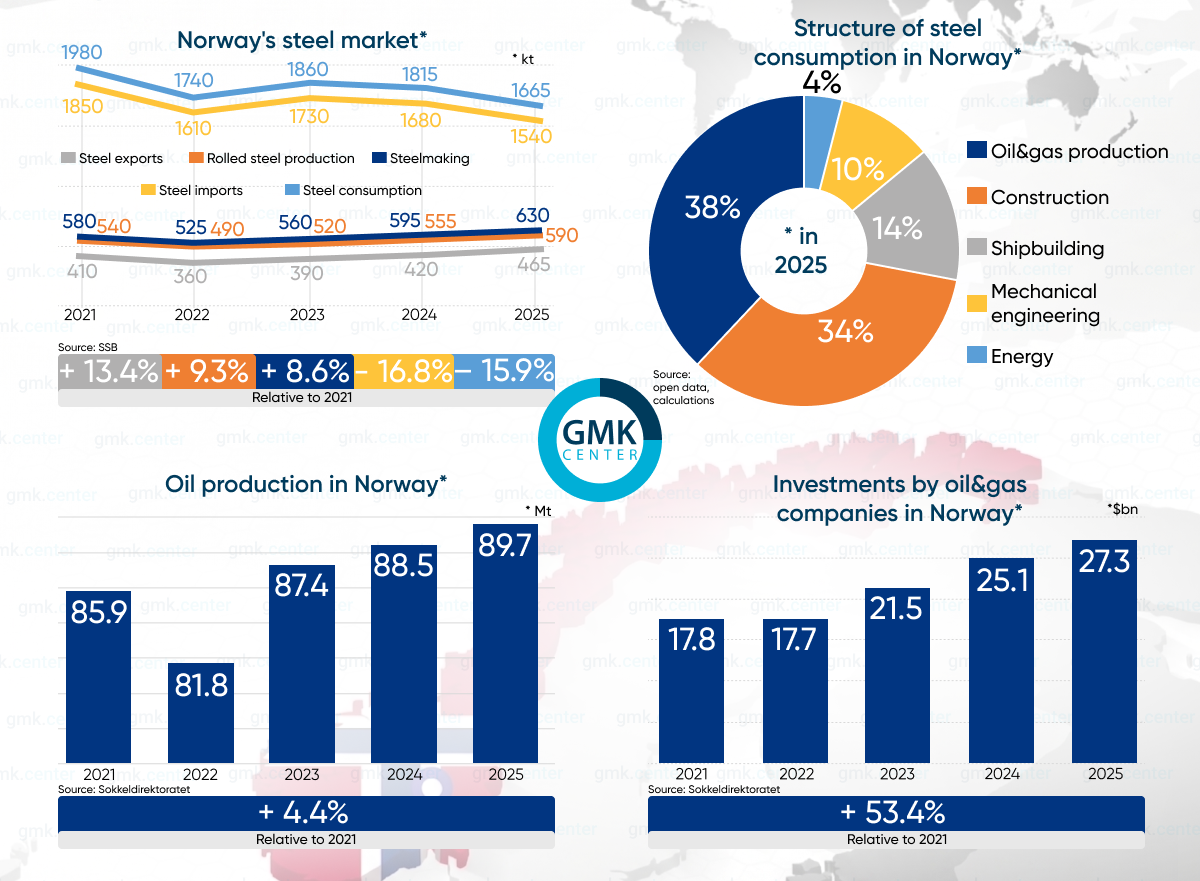

Consequently, in 2025, Norwegian crude and rolled steel production, as well as exports, achieved their best performance in recent years, despite a contraction in the domestic market.

Consumption of flat steel

The structure of steel demand in Norway differs from that of most European countries, where traditional machinery manufacturing and construction dominate. Here, the market is driven by offshore oil and gas production, as the construction of floating drilling platforms requires enormous quantities of sheet steel and pipes.

Heavy machinery manufacturing is also linked to this sector. Local plants specialize in hydraulic cranes for drilling platforms and other deck equipment.

Another significant sector is shipbuilding. Norwegian shipyards have focused on a high-tech specialized fleet: research and expedition vessels, and automated electric port ferries.

The largest consumers of flat steel in Norway:

- VARD Group, part of the Italian shipbuilding conglomerate Fincantieri. Construction of large-tonnage support vessels for offshore wind energy, research vessels, cruise liners, and specialized platforms. Includes the shipyards Vard Langsten, Vard Brattvaag, and Vard Søviknes.

- Aibel AS, which operates a massive shipyard in Haugesund. Here, modules for drilling platforms and floating substations for offshore wind farms are assembled.

- Aker Solutions, whose plants in Verdal and Egersund manufacture steel jackets for drilling platforms and floating wind turbines.

- Nordic Steel, the largest specialized center for precision sheet steel processing. A leading supplier to Norway’s defense, aerospace, and construction industries.

- Tibnor AS and BE Group, large steel service centers. They engage in steelworking and supply finished blanks to small and medium-sized Norwegian engineering and construction companies.

Norway’s oil and gas sector is on the rise, as evidenced by data on oil production and corporate investment. At the same time, direct capital construction and the development of new facilities accounted for about 60% of total expenditures. Despite this, apparent steel consumption has declined. Why is that?

The offshore sector (VARD, Aibel, Aker Solutions) is indeed currently experiencing peak capacity utilization. However, over the past five years, market participants have radically changed their procurement structure. Instead of importing rolled steel and assembling structures domestically, Norwegian customers are increasingly purchasing ready-made modules. This is necessary to reduce domestic labor costs.

Large sections of ship hulls for VARD shipyards are often welded at their own subsidiary shipyard in Romania (Vard Tulcea) and shipped to Norway by sea for final assembly. Heavy bridge spans and trusses are now shipped ready-made from Poland or the Baltic states.

Overall, this leads to a decline in apparent consumption—after all, the steel mill shipped the steel plate not to Norway, but to a Polish or Romanian plant. Formally, the steel was “absorbed” by the Polish or Romanian economies, and it arrived in Norway already as a high-tech finished product.

Therefore, the trend in apparent consumption does not indicate a physical lack of demand for steel, but rather a profound transformation of supply chains. The primary stage of steel processing (cutting, welding, assembling sections) has been shifted outside Norway.

Wind energy is not a driver of steel demand. Protests against the construction of onshore wind farms were so massive that in 2019 the government imposed a three-year moratorium on issuing new permits. However, even after its expiration, the situation remained unchanged. In 2023–2025, the rejection rate of new wind farm projects by municipalities reached nearly 100%.

Offshore wind energy is in its early stages. Only the state-owned oil and gas giant Equinor has its own floating wind farm with a capacity of 95 MW, but it is not connected to the national grid. The purpose of this wind farm is to supply electricity to the Snorre and Gullfaks offshore platforms.

Consumption of long steel

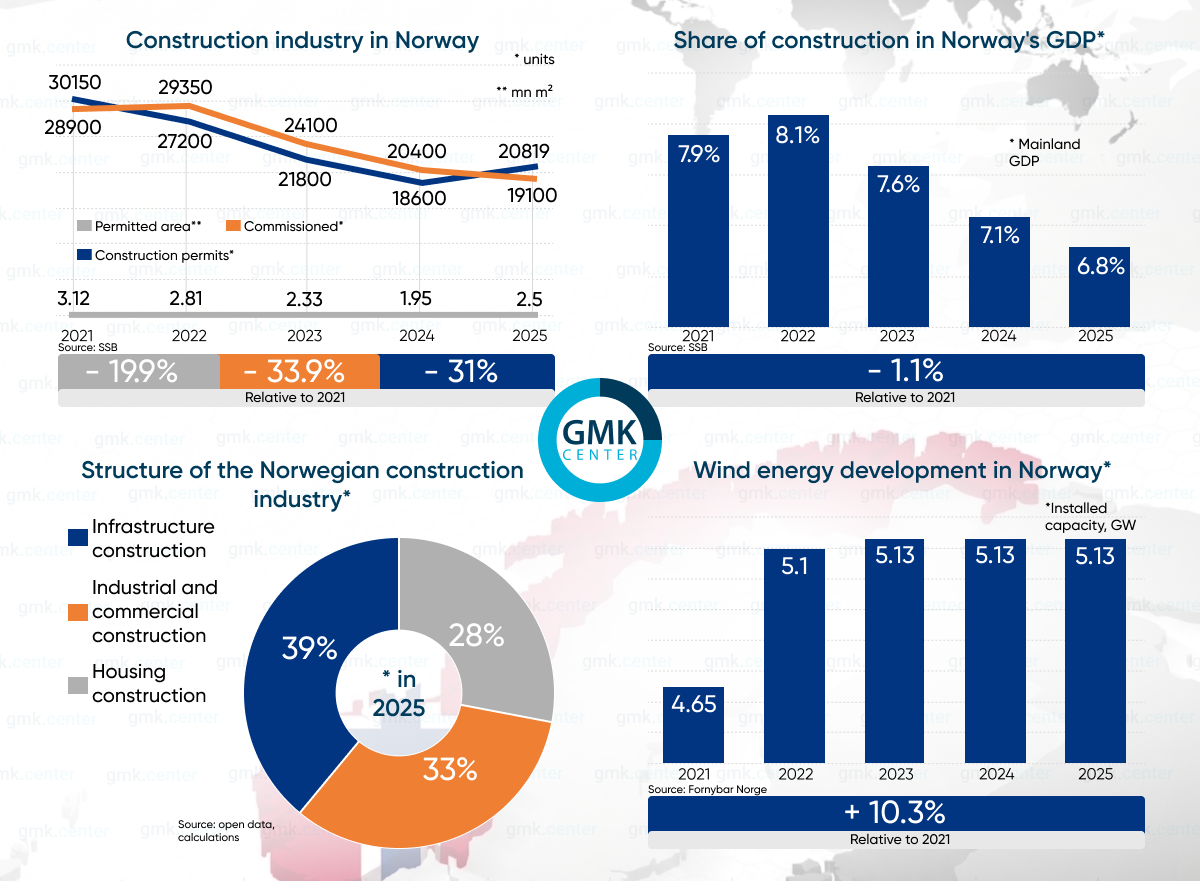

Residential construction is the very sector that is dragging down demand for long products. Norges Bank’s key interest rate rose from 0% to 4.5% between 2021 and 2023. Mortgage loans became unaffordable, and developers faced a sales crisis. The market hit bottom in 2024, when the number of new building permits fell by nearly half compared to 2021.

In 2025, positive momentum emerged for the first time in the past five years. This was aided by Norges Bank’s rate cut to 4%. However, the number of building permits issued is still one-third lower than in pre-crisis 2021.

The infrastructure sector partially offset this decline by purchasing more expensive specialized rebar and profiles with an ultra-low carbon footprint for the construction of bridges, tunnels, and roads.

Among the most significant projects for 2021–2025 in terms of steel consumption:

- Construction of the Follobanen high-speed rail line, connecting Oslo with neighboring regions. It includes the longest railway tunnel in Scandinavia—the 20-kilometer-long double-track Blixtunnelen.

- Modernization of the Vestfoldbanen and Dovrebanen lines. New double-track sections and tunnels were built here (for example, the Drammen-Kobbervikdalen project).

- Reconstruction of the E39 coastal highway between Kristiansand and Trondheim. This includes the Rogfast project—the construction of a 26.7-km twin-tube undersea tunnel. This is an unprecedented engineering feat, with the tunnel descending to a depth of 392 m below sea level.

- Upgrading of the E6 highway connecting the north and south of the country. Dozens of multi-billion-kroner (NOK) contracts have been implemented here to increase capacity to four lanes, straighten sections, and construct new bridges and tunnels in the Trøndelag and Innlandet regions.

- Modernization of power grids in connection with plans to electrify offshore oil and gas production platforms and the construction of new energy-intensive production facilities. The state-owned company Statnett carried out a large-scale program in 2021–2025 to lay new high-voltage power lines and build substations—particularly in the Vestland and Finnmark regions.

- Construction of a new 8-kilometer metro line in Oslo. It runs from the Majorstuen transit hub to the Fornebu peninsula, a suburban area.

Flat steel demand outlook

The Norwegian Offshore Directorate (Sokkeldirektoratet) forecasts a decline in investments in the oil and gas industry to $24.5–25.5 billion in 2026. Despite this, flat steel consumption in Norway will rise, exceeding 1 million tons for the first time in the last three years. Key drivers:

- The strategy of oil and gas companies is focused on decarbonization. They are cutting costs on drilling new wells, but at the same time are allocating significant budgets to electrify existing platforms from shore to reduce CO2 emissions and avoid paying substantial taxes on them.

To this end, massive distribution platforms and floating substations are being built at sea. Aibel and Aker Solutions are currently actively processing heavy plate for these projects.

- Full-scale deployment in 2026 of the Northern Lights project (a joint venture between Equinor, Shell, and TotalEnergies) for CO2 capture and storage beneath the North Sea seabed. Plans include the construction of large storage facilities and onshore terminals for CO2 liquefaction in Norway.

- A practical transition to the development of offshore wind energy. In January 2026, Norway, together with other North Sea countries, signed the “Wind Energy Investment Pact.” This serves as the foundation for the industry’s development. The Norwegian government has set a goal of achieving 30 GW of offshore wind capacity by 2040.

The tender for the development of the first offshore wind farm, Sørlige Nordsjø II, in the southern part of the North Sea has now been completed. The installed capacity of the first phase will be 1.5 GW. The Belgian-Swedish consortium Ventyr was selected as the winner, and commissioning is scheduled for 2030. The Worley Rosenberg shipyard in Stavanger has been selected as the contractor for the construction of the offshore substation.

Long steel demand outlook

The increase in approved residential floor space to 2.5 million m² by 2025 did not translate into a recovery in reinforcing bar demand from the residential construction sector in 2026. SSB and the analytical agency Prognosesenteret forecast a 2.5–2.7% increase in construction output for the current year, including a 2–2.5% rise in new housing construction. However, this will not lead to increased consumption—most new permits were issued for wooden cottages.

The institutional sector will support demand for long rolled steel. Here, volumes are projected to grow by 12% due to the construction of new public hospitals. As part of the National Health Plan (Og sykehusplan), the government has approved $2.7 billion in loans for these purposes. Funding in 2026 will amount to $750 million (for new and currently under-construction hospitals).

Growth in the infrastructure sector will be 2.7%. The road construction budget for 2026 has been increased to $2.26 billion compared to $1.83 billion in 2024. However, there is a caveat.

The additional production and funding volumes are accounted for by asphalt and earthwork projects. Total demand for long products will decline by 2–2.5%, to 780,000 tons.

The most significant infrastructure projects for steel consumption in 2026 are:

- Construction of the Ringeriksbanen railway line and the E16 highway between Oslo and Bergen. This year, plans call for the construction of 40 km of new double-track high-speed railway and 15 km of a four-lane highway on the “Skaret–Genefoss” section.

- Construction of the E18 (Western Corridor) Lysaker-Ramstadsletta highway. The route runs through densely populated areas, with most of it consisting of complex underground tunnels and interchanges. The concrete work here is characterized by extremely dense reinforcement.

- Continued construction of the Rogfast Tunnel — sustaining stable demand for steel; completion is scheduled for 2033.

- Continued construction of a new metro line in Oslo.

Overall, the capacity of Norway’s steel market will grow to 1.72 million tons in 2026, driven by the flat-rolled steel segment. This will require imports of 1.42 million tons, taking into account the projected production of 600,000 tons in Mu-i-Rana and the export plans of Sev.en Global Investments.

-

02 July 2026

16 June 2026

10 June 2026

20 May 2026