Posts Global Market steel consumption 518 10 June 2026

Consumption of finished steel is set to rise to 1.43–1.45 million tonnes in 2026

The trend in steel sales in Denmark shows little correlation with developments in the country’s economy. Despite large-scale government investment in infrastructure and the expansion of the wind energy sector, demand for finished rolled steel remains stagnant. The explanation lies in a shift in consumption patterns, which no longer reflect the actual demand for steel.

Industry overview

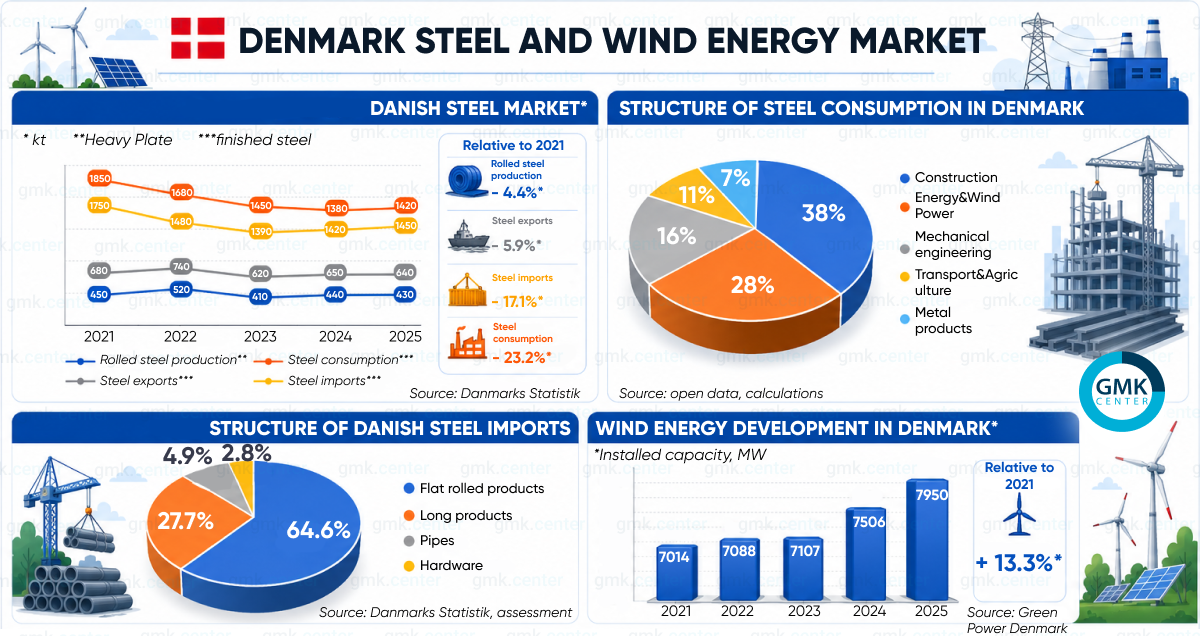

The sole rolled steel producer is the NLMK DanSteel (NDS) rolling mill, with an annual capacity of 750,000 tonnes. It specialises in heavy plate for the wind energy and shipbuilding sectors.

The total investment by the Russian NLMK Group in the Danish asset since its purchase in 2002 has exceeded €200 million. By 2021, a large-scale modernisation had been completed here, with capacity increasing from 500,000 to 750,000 tonnes. The rolling mill underwent a major overhaul. It can now process ultra-heavy slabs up to 260 mm thick.

In 2022–2023, the plant upgraded its fuel supply system and heating furnace injectors — against the backdrop of soaring European energy prices. This created the technical capability to replace natural gas with biomethane.

Denmark is one of Europe’s leading producers of biomethane, which is why NDS was able to purchase certified biogas. This reduced Scope 1 emissions by 20–25%.

The Duferco Danish Steel AS (DDS) rolling mill, with an annual capacity of 500,000 tonnes, is located on the same site as NDS. This plant produced long products until June 2025, after which it ceased operations following a decision by its owners, the Swiss group Duferco. According to the plant’s CEO, Giuliano Bo, it had been making losses for 14 out of the 19 years it was part of Duferco.

The European energy crisis of 2022–2025 hit DDS much harder than NDS, due to the higher energy intensity of its production. At the same time, DDS faced sales difficulties against a backdrop of falling construction activity in Denmark and Germany. This was compounded by an increase in cheap rebar imports from South-East Asia.

Finally, NDS, thanks to its exemption from EU anti-Russian sanctions, receives cheap slabs from Lipetsk. DDS was forced to purchase European billets, which had risen sharply in price. Consequently, the resumption of operations at Duferco Danish Steel is not anticipated in the foreseeable future.

Impact of government policy

In Denmark, the state does not provide financial support for steelworks decarbonisation projects, as is the case in Sweden, Finland, and Norway.

Decarbonisation of the steel industry in Denmark is indirectly supported through the implementation of the European Industrial Accelerator Act. Under this legislation, at least 25% of the steel used in the construction of wind farms and infrastructure with state involvement must have a low carbon footprint.

As a pure re-roller, NDS’s Scope 1 and 2 emissions are relatively low. The greatest challenge by 2030 will be Scope 3 — the high carbon footprint of Russian slab. The main issue the plant in Frederiksværk needs to resolve is where to find a new, greener supplier of semi-finished products.

The energy component

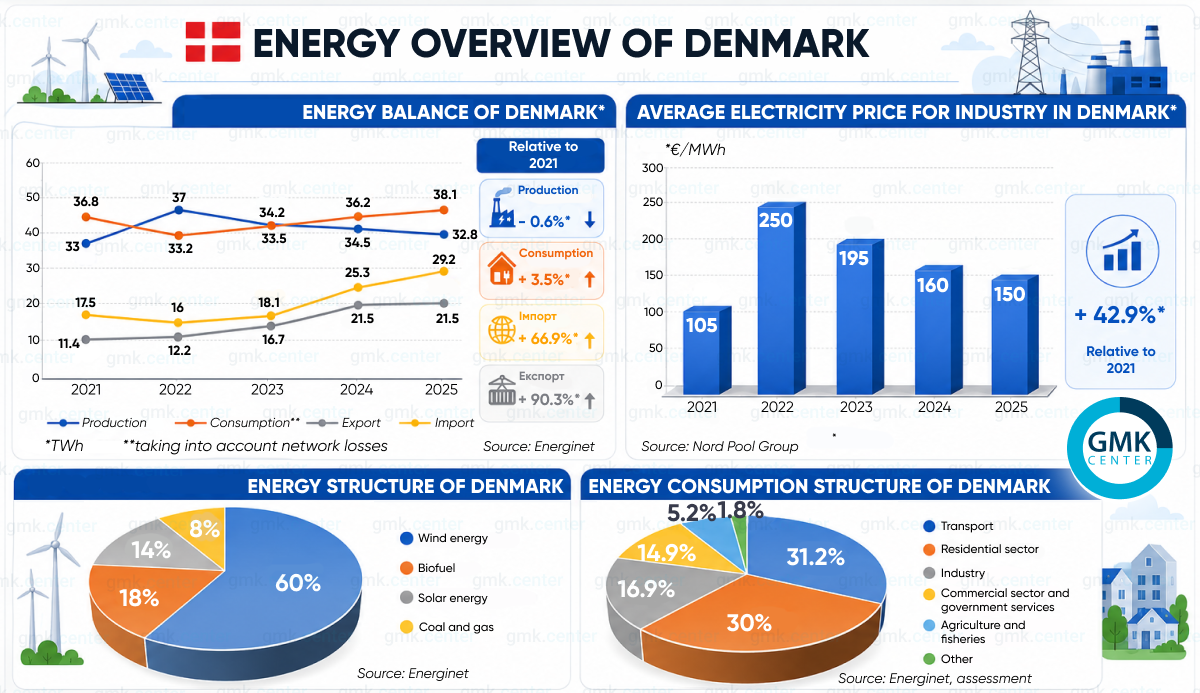

Wind power is the cornerstone of Denmark’s energy balance. Hence its inevitable volatility. When the wind blows, Denmark floods Germany, the Netherlands, and the UK with cheap electricity. When the wind drops, Danish industry survives on imports from Sweden and Norway.

For the DanSteel plant, this means extreme price fluctuations. During periods of peak wind, the cost of electricity drops to zero or even goes into negative territory. But during windless winter weeks, it can soar to €200–400/MWh. Therefore, the resumption of electric steelmaking at Frederiksværk does not appear feasible.

In Denmark’s energy consumption breakdown, industry ranks a modest third. In neighbouring Sweden and Finland, the industrial sector accounts for twice that share. And very soon, Danish factories will have to compete for megawatts with new consumers from the IT sector.

According to estimates by the Danish grid operator Energinet, by the end of the 2020s, data centres will account for 15–20% of the country’s energy consumption. For metalworking and rolling mills, this means an additional premium on energy market prices. Especially on windless days.

The final cost of electricity for industrial consumers in Denmark is high by Scandinavian standards. This is the case even with relatively moderate base prices on the Nord Pool wholesale energy exchange. The reason lies in heavily inflated grid charges, distribution tariffs and specific environmental taxes. The state passes the latter on to the non-domestic sector.

Market profile

A key feature of the Danish steel balance is that rolled steel production is disconnected from the structure of domestic consumption. NDS operates almost entirely on the export market. Demand from the engineering, wind energy and construction sectors is met by imports.

Foreign orders are estimated to account for 80–85% of NDS’s order book. The main customers are heavy engineering and steel structure plants in Germany and Sweden, as well as shipyards in Belgium and the Netherlands. This explains the growth in domestic production in 2022, despite a slump in steel consumption in Denmark itself.

HRC, CRC, HDG, shaped steel and reinforcing bars are sourced from Germany (ThyssenKrupp and Salzgitter), Sweden (SSAB), Finland (Outokumpu), Poland (ArcelorMittal Poland and CMC Poland) and the Netherlands (Tata Steel IJmuiden). Import volumes consistently exceed consumption due to re-export following further processing at local steel service centres (SSCs).

These centres purchase coils and sections, cut them to precise dimensions, stamp, profile, apply protective coatings or convert them into assembly units. After this, the steel changes its customs status and is shipped to engineering plants in Sweden, Norway, and Germany as a finished commercial product. This scheme determines the dominance of flat steel in the import structure.

Consumption of flat-rolled steel

Heavy plate accounts for 45–50% of sales. This is due to Denmark’s global leadership in the wind energy sector. Vestas Wind Systems AS manufactures and supplies wind turbine equipment to many European countries. Heavy plate steel is primarily used in its production. The support towers may be manufactured by local steel structure plants, but the company manufactures the wind turbines themselves without localisation.

The next largest consumer is the engineering sector. This includes SSC, which manufactures frame structures for Swedish automotive giants (Scania and Volvo Trucks). In the statistics, they are listed as the ‘automotive supply chain’, although Denmark has no domestic car manufacturing industry.

The top five largest steel consumers include:

- Vestas Wind Systems AS, manufacturer of wind turbines and towers for onshore wind farms.

- Titan Wind Energy (Europe) and CS Wind Offshore (Bladt Industries) specialise in wind turbine towers, foundations, and platforms for offshore wind farms, as well as floating substation units.

- Højbjerg Maskinfabrik AS (HMF Group), manufactures heavy-duty hydraulic mobile cranes. These are mounted on chassis from Swedish manufacturers Scania and Volvo, and German manufacturer MAN.

- Ib Andresen Industri AS, a manufacturer of steel sections and stamped components for third-party customers, including car manufacturers.

Grundfos AS, a global leader in the manufacture of pumping equipment.

The construction of its wind farms in Denmark in 2022–2023 was put on hold due to rising prices for finished steel. The industry operated exclusively on export contracts and the replacement of old turbines at existing wind farms. In 2024–2025, the increase in steel consumption was driven by the construction of the Vesterhav Nord and Vesterhav Syd offshore wind farms with a combined capacity of 350 MW.

Consumption of long products

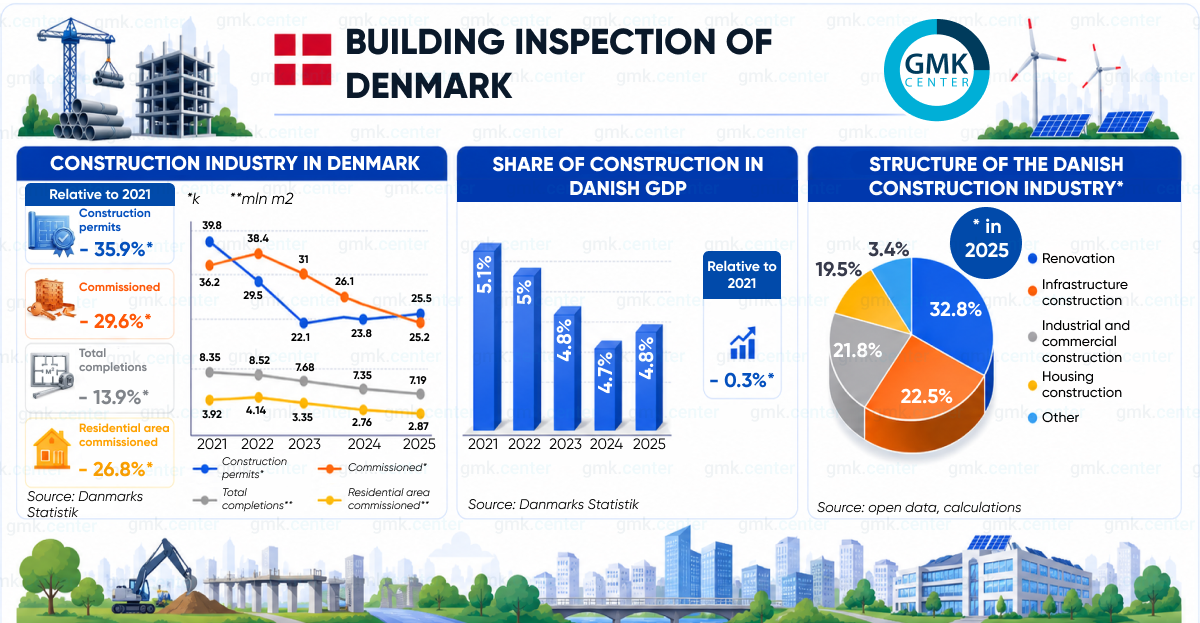

The construction industry, the main consumer of long products, plunged into crisis following Nationalbanken’s base rate hikes in 2022–2023. This dealt a blow to housing construction. Between the peak year of 2022 and the crisis year of 2024, the residential property market contracted by 1.38 million m². For a country the size of Denmark, this represents a colossal drop in construction activity, which has affected sales of reinforcing bars and shaped steel.

Demand for steel was driven by the infrastructure sector and industrial construction. Major infrastructure projects involving vast quantities of steel structures include:

- Construction of the Fehmarnbelt Fixed Link tunnel. It will run along the seabed of the Baltic Sea and connect the Danish island of Lolland with the German island of Fehmarn. The project spans 18 km and includes a four-lane motorway and two electrified railway lines. The total budget is €7 billion.

- The creation of the 275-hectare artificial island of Lynetteholm in Copenhagen. Here, vast quantities of steel sheet piling are being used to form the island’s outer perimeter. It serves a dual purpose: protecting the city from storm surges and creating a residential area for 35,000 people. The cost of phase one of the works is €2.7 billion.

- Construction of the new 4 km-long Storstrøm Bridge. It will connect the islands of Zealand and Falster. Plans include the construction of a dual-carriageway motorway and a high-speed railway line.

Reconstruction of the 115 km ‘Ringsted–Redby’ railway line. Construction of a second track, electrification, and widening of the Gulborgsund and Masnedsund bridges. - Construction of the M4 metro line in Copenhagen.

The increase in industrial space commissioned is driven by the construction of data centres and the strategy of Danish pharmaceutical giant Novo Nordisk. It is building new factories in Odense and Hillerød, as well as expanding its existing facility in Kalundborg. The total cost of these projects is €6.53 billion.

Outlook for steel demand

The specific characteristics of the Danish economy suggest that steel consumption is set to rise to 1.43–1.45 million tonnes by 2026. In this scenario, sales of flat steel products will increase by 2.5–3%, reaching 740–770 thousand tonnes.

Danish demand for sheet steel is linked to the wind energy sector and the global power generation machinery industry, rather than the traditional automotive sector. Sales trends are driven not by the availability of car loans, but by entirely different factors.

- Production of wind turbines, towers, and foundations for wind farms remains stable, ensuring continued demand for heavy plate. The capacity of Danish wind farms is expected to increase to 8.82 GW by the end of 2026.

The growth driver is the construction of Thor, Denmark’s largest offshore wind farm with a capacity of 1.1 GW. Turbine installation has already begun there. Local manufacturers of towers and steel structures (Welcon, Bladt Industries) are fully booked with orders for this project.

- Continued modernisation of existing wind farms. The installation of new turbines with a capacity of up to 15 MW requires the replacement of tower foundations. Of the 5,600 operational turbines, 1,800 have reached the end of their 20-year service life (or will do so in 2026–2027).

- Whilst the European engineering sector is declining, Danish companies (Grundfos and Danfoss) remain confident thanks to global demand for energy-efficient equipment and industrial heat pumps.

The projected 2.7% increase in construction output in Denmark (in monetary terms) by the end of 2026 suggests a 2% rise in demand for long products, to 610–630 thousand tonnes.

Residential construction remains under pressure from the Nationalbank’s high policy rate. The drivers are previously launched infrastructure projects: the continuation of the Fehmarnbelt Fixed Link tunnel, the construction of the Storstrøm Bridge, and works on Lynetteholm Island.

Industrial construction will maintain positive momentum thanks to the commissioning of new data centres. According to a forecast by the Danish association Datacenterindustrien, data centre capacity will grow from 556 MW in 2025 to 608 MW by the end of 2026. The main project is the construction of the 200 MW Thylander data centre in Esbjerg. The completion of phase I is now entering the final stages.

An important point to note. Given the above, the demand for steel in Denmark could have been significantly higher. However, as in Norway, local manufacturers try wherever possible to outsource primary metal processing, retaining only the finishing and assembly stages.

For example, all 72 massive monopiles for the Thor wind farm were manufactured at the German EEW SPC plant in Rostock. The wind tower sections were produced at German and Spanish facilities. Statistically, these huge volumes of finished steel were credited to Germany and Spain. They had no impact whatsoever on the sales figures of Danish steel traders.

As a result, the Danish and Norwegian ‘green’ energy boom is fuelling the markets in Poland, Romania, Germany, and the Baltic states, boosting rolled steel sales in these countries. Denmark itself remains a modest local market in terms of steel sales.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

17 July 2026

14 July 2026

16 June 2026