Posts Global Market steel consumption 30 17 July 2026

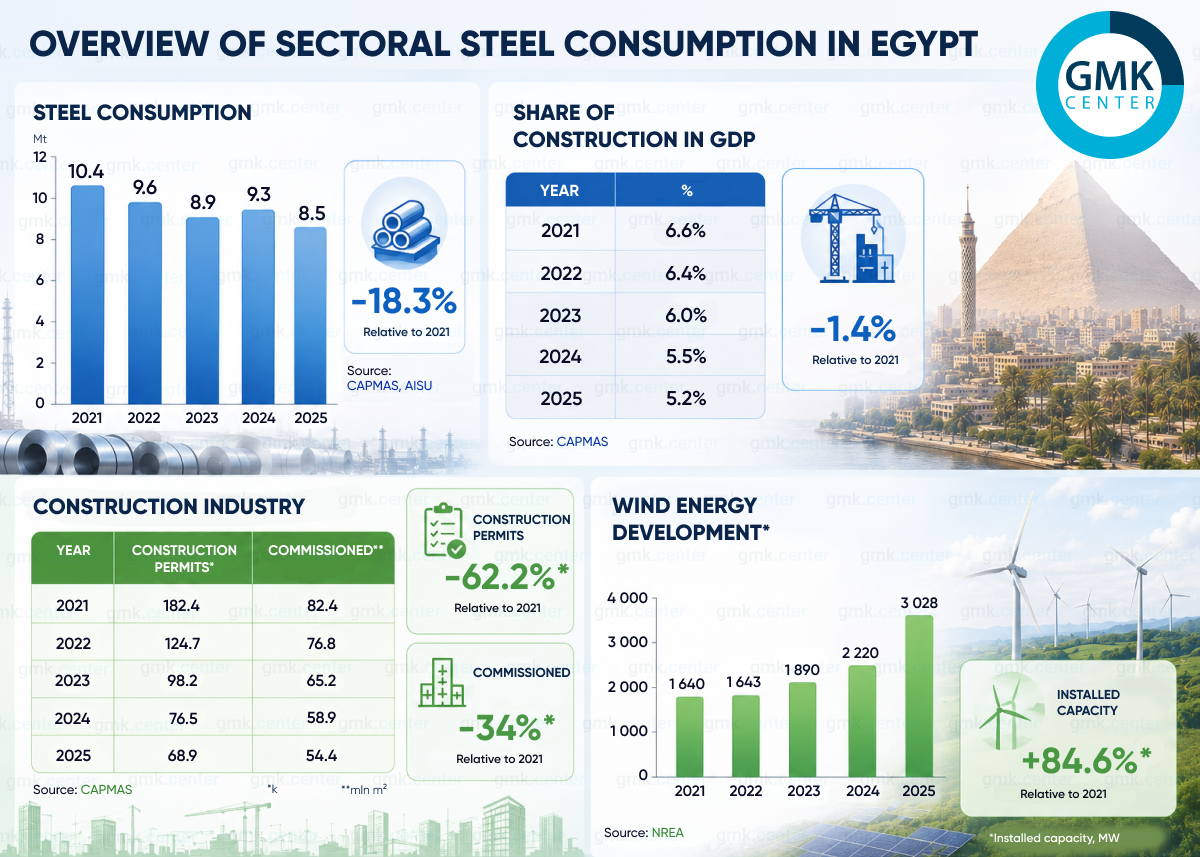

Domestic demand for finished steel is set to fall by 1.8% – to 8.35 million tonnes in 2026

The exchange rate of the Egyptian pound plummeted from $/15.7 EGP in 2022 to $/47 EGP in 2025. To overcome the currency crisis, the authorities were forced to turn to the IMF. In exchange for loans totalling $/8 billion, the Egyptian government had to agree to a radical increase in public spending, which was the main driver of steel sales.

Structure of steel demand

Flat steel products account for only 18–22% of consumption. The Egyptian industry consists of the assembly of household appliances, minibuses and commercial vehicles. Thanks to government localisation programmes, it is growing slowly, but is not yet a powerful driver of steel demand on a par with the construction sector.

Demand for flat steel is being driven by the development of the wind energy sector. The year 2025 proved to be a breakthrough year, with 808 MW of new wind farms commissioned. The largest contribution came from the launch of the 650 MW Red Sea Wind Energy project in the Gulf of Suez. Steel consumption per 1 MW amounts to around 100–120 tonnes. This consists primarily of thick plate for wind turbine towers and heavy reinforcing bars for their foundations.

Construction accounts for 78–82% of the country’s total steel consumption. The 2022 devaluation and the increase in the CBE’s policy rate from 8.25% – to 16.25% led to a sharp slowdown in the sector. Financing the construction of new projects through loans became prohibitively expensive not only for businesses but also for the government itself.

State funding is of paramount importance, as infrastructure accounts for 53% of all construction work currently underway. Infrastructure projects worth over $30 million collectively account for 34.5% of the total market volume. Notable among these are projects to develop irrigation systems in the south of the country, New Toshka and Sharq El Owainat. Residential construction accounts for 34% of this volume.

In view of this, the largest consumers of rolled steel in the country are property developers. These include the state-owned corporation Arab Contractors, the state-owned companies Main Development Company and City Edge Developments, and the private construction holding companies Orascom Construction, Hassan Allam, Dorra and SIAC.

The impact of the currency crisis on steel consumption

The devaluation of 2024 did not deal such a severe blow to the construction sector as in 2022, even despite the CBE raising its policy rate to a record 27.25%. By then, Egypt’s flagship construction project, the New Administrative Capital (NAC), had moved on to the stage of interior finishing of the buildings. However, the sector managed to stay afloat, continuing to generate steady demand.

A lifeline came in the form of a government agreement with the UAE’s sovereign wealth fund (ADQ) to build the city of Ras El Hekma on the Mediterranean coast. The total area will exceed 170 km², making it twice the size of Barcelona. The first district, Wadi Yemm, covering an area of 50 km², is currently under construction.

Once completed, the city is projected to attract 8 million tourists annually. But it will not merely be a seasonal resort; rather, it will be a year-round ‘smart’ and environmentally sustainable metropolis. The cost of its construction will reach $110 billion, of which $35 billion will be direct investment from ADQ. The project includes the construction of a high-speed railway line to Cairo.

Despite the currency crisis, the government increased budgetary investment in construction by 82% in 2025, to $790 million. However, these figures are nowhere near what they used to be.

New loans were also secured from the European Bank for Reconstruction and Development, the African Development Bank and the International Finance Corporation. As a result, work resumed under the ‘New Urban Communities Administration’ (NUCA) programme (the state-owned company operating the project bears the same name).

NUCA’s aim is to ‘relieve’ the overpopulated Nile Delta by relocating people to the desert and the coast. To this end, plans are in place to build 40 ‘smart’ 4G cities. Fourteen of these are currently under construction, including NAC. All 14 of these cities are being built to a single standard: 100% digital governance, ‘smart’ energy grids, mandatory use of renewable energy, a well-developed public transport network and a focus on environmental sustainability.

Among them, New Alamein is particularly noteworthy — a year-round metropolis with a population of 3 million, serving as the administrative, educational and business centre of the Mediterranean coast. The city covers an area of over 200 km². It is home to the Egyptian President’s summer residence, the Cabinet building and government offices. The city is home to three international universities, a vast library, an opera house and a History Museum.

All these facilities, along with a row of 25 residential skyscrapers over 40 storeys high, form part of the first phase of the project, which has been fully completed. Work is currently underway on the second and third phases, including the Latin Quarter — a large residential area featuring classical Mediterranean architecture. The construction of all these buildings requires a colossal amount of rolled steel.

It is worth noting that Ras El Hekma will be located next to New Alamein, but it is not part of NUCA. Its parameters are set out in an intergovernmental agreement between Egypt and the UAE.

Outlook for steel demand

The gradual increase in localisation will encourage household appliance and bus assembly plants to manufacture an increasing number of components in Egypt. This paves the way for higher demand for flat steel products. It is likely that this demand will be fully met by Ezz Steel’s new production capacity.

The emergence of new customers will boost demand. At the end of April 2026, the Shangyuan steel structures plant opened in Ain Sokhna, specialising in trusses, scaffolding, power line pylons and bridge spans. The plant has a capacity of 15,000 tonnes per year, but this is just one example. Also in Ain Sokhna, Massoud Steel began producing steel containers in March.

The government has ambitious plans for renewable energy this year. In total, 2.5 GW of new wind and solar power capacity is expected to come online. The flagship project is the construction of the world’s largest offshore wind farm, Ras Shokeir (900 MW), by the French group ENGIE. The bulk of the flat steel and reinforcing bars for this project will be supplied as early as the second half of 2026.

This provides grounds for forecasting a 1.8% increase in flat steel consumption by the end of 2026, to 2.85 million tonnes.

For the 2026–2027 financial years, the Egyptian government has, at the IMF’s request, ‘frozen’ direct budgetary allocations for the construction of new cities. This does not mean that construction has stopped. NUCA will finance the completion of construction through the sale of land plots to private developers and of completed properties on the northern coast. These are colossal sums: over the last two financial years, the value of transactions has reached $24 billion.

Industrial construction will help to sustain demand for steel. This relates primarily to the expansion into Egypt by the Chinese state-owned corporation CNCEC (China National Chemical Engineering Corporation). Its main project is the Red Sea Petrochemicals plant, currently under construction in Ain Sokhna, with a value of $1.7 billion.

In addition, CNCEC has secured contracts to build plants for soda ash and metallurgical silicon. To avoid having to transport steel structures for its Egyptian projects from China, the corporation signed a contract with the SCZone administration in January 2026 to build a $34 million steel structure plant. Its annual capacity will be 20,000 tonnes. Local steelworks will act as suppliers for the plant.

In the future, CNCEC plans to build a $250 million steel tank manufacturing plant specifically to meet the needs of soda ash and silicon production. Other major industrial projects currently under way include:

- The construction of the Alstom complex in Burg el-Arab. The first plant for the production of railway automation and cable systems has already reached the commissioning stage; construction of the second plant – a rolling stock manufacturing plant – is currently underway.

- Construction of the Kemet&Al Qalaa seamless steel pipe plant in Ain Sokhna, with a capacity of 250,000 tonnes per year. The project is valued at $3.5 billion.

- Construction of the Canal Sugar sugar refinery in Minya, with an annual capacity of 1 million tonnes. The project is valued at $1 billion.

- Construction of a €40 million railway carriage manufacturing plant in Burg el-Arab, in partnership with the Polish company Tabor. The plant’s annual production capacity is 300 freight and passenger carriages.

- Construction of a wind turbine manufacturing plant in SCZone. The plant’s future capacity is 2 GW; the Chinese engineering corporation SANY is investing $300 million in this project.

All of the above facilities, with the exception of Canal Sugar, will generate demand for flat steel products once completed. A key feature of this sector is that construction work continues even during Ramadan, unlike in residential construction. This ensures a stable supply for traders and steelworks.

Demand for long-length rolled steel will be supported by infrastructure development. The largest project is the construction of three high-speed railway lines for passenger transport. It is being carried out by a consortium comprising Arab Contractors, Orascom Construction and Siemens Mobility.

Work is currently in full swing on Line 1, ‘Ain – Sokhna – Cairo – Alexandria – Mersa Matruh’, which stretches 660 km. Track laying has been completed on 130 km of the route, whilst work on the construction of station complexes and 58 bridges and viaducts is 70% complete.

On the second line, ‘October City – Luxor – Aswan – Abu Simbel’, which is 1,100 km long, the completion rate for infrastructure works (embankments, bridge crossings under railway tracks) is estimated at approximately 40%.

At the same time, cuts to state funding at the IMF’s request will have a negative impact on the pace of work and steel consumption volumes. By the end of 2026, demand for long steel products is forecast to fall by 3.5%, to 5.5 million tonnes. Overall, finished steel consumption in Egypt will fall by 1.8% – to 8.35 million tonnes.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

14 July 2026

16 June 2026

10 June 2026