Posts Global Market Finland 570 20 May 2026

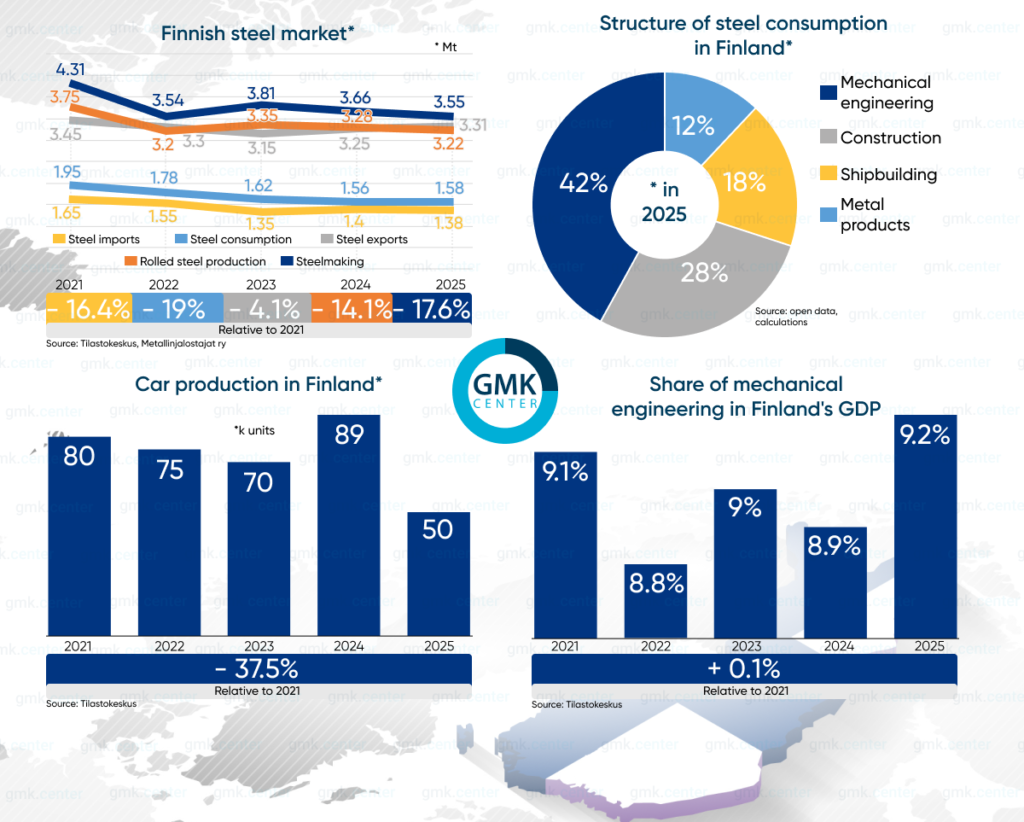

Over the past five years, steel production in Finland has fallen by 17.6%, while consumption has dropped by 19%

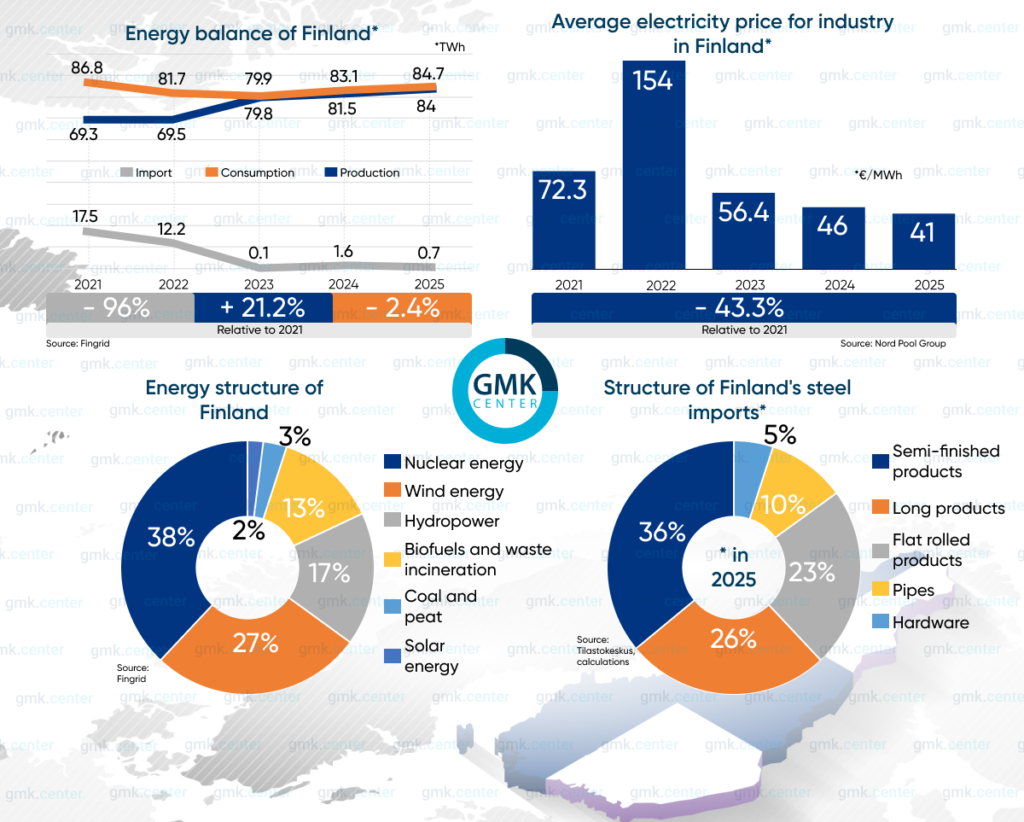

Electricity in Finland is among the cheapest in the EU. Despite this, the European energy crisis has significantly worsened the situation in the local market. Steel producers in Finland have suffered due to their export focus on the European Union, while consumers have been affected by their dependence on European imports, which have risen sharply in price.

Industry overview

The flagship carbon steel producer is the integrated plant in Raah, with an annual capacity of 2.6 million tons. It specializes in coils and sheets for the machinery industry and is part of the Swedish SSAB Group.

The key facility of the Finnish Outokumpu Group is located in Tornio. Thanks to vertical integration of production, it is one of the world’s most efficient stainless steel mills. It produces cold-rolled coils, with an annual capacity of 1.2 million tons.

A niche but important player is the EAF plant in Imatra, which is part of the Japanese company Ovako (a subsidiary of Nippon Steel). The plant’s steelmaking capacity is 575,000 tons per year (nominally), and its rolling capacity is 200,000 tons. It specializes in premium long products for complex engineering solutions in mechanical engineering and other industries.

Blastr Green Steel deserves special attention. This is a future H2-DRI-EAF plant with an annual capacity of 2.5 million tons of steel. The project is currently in the environmental assessment phase and undergoing negotiations with investors. Its stated cost is €4 billion. According to local media reports, the project is facing difficulties in securing full financing and connecting to the power grid.

Finnish steel mills are focusing their investments primarily on the decarbonization of steel production.

- SSAB Raahe has planned an EAF transition by 2030. The project is currently in the active engineering phase, and site preparation for the EAF construction is underway. The project is estimated to cost approximately €2 billion. Between 2021 and 2023, SSAB modernized its rolling mill in Raahe, improving surface quality and expanding its product range of advanced high-strength steels (AHSS). The cost amounted to €100 million. The modernization of rolling capacity for AHSS is ongoing.

- In 2024–2025, Outokumpu built a bio-coke battery in Tornio that runs on wood waste. The project cost €30 million. In 2022–2023, the bright annealing line at the same site was modernized: energy efficiency was improved and the control system was digitized. The cost was €20 million.

- In 2023–2025, Ovako replaced the heating furnaces at its plant in Imatra. New steel reheating units can use H2 instead of NG prior to rolling. This helped reduce specific CO2 emissions to 0.231 t. The project cost €15–20 million. In 2021–2022, the plant installed a vacuum degassing unit costing €7 million. This has improved the purity of steels for the automotive industry

Another notable initiative is the project to build a hydrogen hub in Raahe. Its electrolysis capacity is expected to be at least 70 MW. SSAB is not participating in the project (it is operated by P2X Solutions, a company controlled by the Swiss group Alpiq AG), but will become the main buyer of its products. After the steel mill in Raahe is fully decarbonized, it will need about 150,000 tons of green H2 per year.

Design work is currently underway to integrate the hub with local heating networks and the SSAB plant. Environmental impact studies required to obtain an environmental permit are also being conducted. According to P2X Solutions’ estimates, this will take about a year.

The impact of government policy

The Finnish government understands that, without its support, steelmakers cannot afford the massive capital expenditures required for the green transition. Therefore, it uses a co-investment model to provide support, which helps mitigate risks. Its main components include:

- A direct tax credit of 20% of the investment amount in Net Zero projects (including zero-emission steel), but not exceeding €150 million per project. This is the most powerful tool launched by the government of Petteri Orpo in 2024–2025.

- Direct grant funding through the state agency Business Finland. In April 2026, €20 million was allocated to SSAB for the Sustainable World through Steels program. It involves creating a network of over 200 partners (universities, startups) to develop new technologies for EAF steelmaking. SSAB is allocating an additional €30 million for these purposes.

In 2021-2023, Outokumpu received €10–15 million in grants from the agency to support the digitalization of production processes in its mining division and improve energy efficiency.

- Preferential loans from the state-run Ilmastorahasto Climate Fund in the amount of €4–40 million, but not exceeding 50% of project costs. The fund provided financing for a bio-coke battery in Tornio and P2X Solutions projects for the production of green H2.

- Grants from the EU Innovation Fund. These cover up to 60% of additional costs associated with decarbonization. In 2025, Finnish companies submitted applications totaling over €840 million (including hydrogen hubs for the steel sector). The Finnish government is actively lobbying for these applications.

Total state support for the Finnish steel sector through 2030 (including tax incentives) is estimated at €500–700 million. This covers 25–30% of the industry’s decarbonization costs. An important nuance: the Finnish government does not simply give money to businesses; it creates a financial “lever.” For every euro of state grants, companies are required to attract 2–3 euros in private investment.

The energy component

The structure of Finland’s energy sector provides an ideal foundation for green steel. That is why SSAB and Outokumpu are so confident about the transition to electric arc furnaces (EAFs): the country has both the necessary capacity and low electricity prices. Thanks to a surplus of wind energy and a stable nuclear power base, Finland regularly recorded hours with negative electricity prices, down to minus €10/MWh, in 2024–2025. In 2025, the average industrial tariff fell by 9%, while electricity prices in continental Europe rose again.

Dependence on electricity imports, which accounted for 20% of consumption in 2021, has virtually disappeared since 2023. This occurred following the commissioning of Power Unit No. 3 at the Olkiluoto NPP (which houses Europe’s most powerful nuclear reactor, rated at 1.6 GW) in 2023 and the addition of 1 GW of installed wind power capacity in 2024. In 2025, wind power accounted for 57% of total generation.

The share of zero-emission electricity in total generation reached 96% in 2025. Also in 2025, a legislative ban on the use of coal in the electricity sector came into effect in Finland.

The commissioning of the Aurora Line power transmission line between the Swedish Messaure substation and the Finnish Pyhänselkä substation, which took place in early 2026, was of significant importance. The Finnish side gained an additional 800 MW of electricity transmission capacity from Sweden.

First, this created a backup channel for uninterrupted green power supply to future EAFs during periods of calm weather. Second, it allowed the price of electricity for industry, including steel sector, to be “decoupled” from the European wholesale energy market Nord Pool and “pegged” to the Swedish energy regions SE1 and SE2, which offer the cheapest electricity.

As in Sweden, Finland has a system of state compensation for industrial enterprises’ indirect CO2 emission costs (ETS Compensation) arising from the inclusion of the cost of carbon allowances (EU ETS) in electricity tariffs. The total compensation for 2021–2025 amounted to €687 million. Additionally, Finland levies an energy tax on industrial enterprises at the lowest rate in Europe, €0.5/MWh. By comparison, Finnish households pay €22.5/MWh.

As a result, the Finnish steel industry now relies entirely on domestic power generation, obtaining electricity at reasonable prices.

Market overview

Finnish crude steel production and rolled steel production reached an all-time high in 2021. This is important to consider when analyzing the trends of recent years. Also significant is the fact that during that record year, mills built up large inventories of semi-finished products. Consequently, the decline in rolled steel production in 2022 was not as significant as the drop in steel production. The same situation recurred in 2025.

The 3% decline in steel production in 2025 is due to a deliberate reduction in the production of standard steel grades. Finnish mills have shifted away from the most energy-intensive and low-margin products in favor of premium grades. For SSAB, this is partly due to preparations for the replacement of the BF-BOF with an EAF in Raahe.

Despite this, the capacity utilization rate of steelmaking facilities in Finland in 2025 stood at 80.7%, compared to the pan-European average of 72%. This ratio indicates the high competitiveness of Finnish steel mills. In 2025, they exported over 65% of all rolled steel produced. The main destinations were Germany, the Netherlands, and the United States.

Interestingly, the “fewer tons, higher margins” strategy allowed Finnish steelmakers to increase exports in physical terms in 2025. The growth was driven by the AHSS segment. The main surprise of 2025 was a 12–19% increase in sales to the U.S. across various product lines. This occurred despite the 25–50% tariffs on steel imports imposed by the Donald Trump administration. In terms of growth rates, shipments to the U.S. have surpassed those to Germany, the traditional sales market.

Flat-rolled products account for 92% of total production in Finland, with the remaining 8% consisting of premium-segment long-rolled products. Local companies purchase rebar and shaped rolled products for construction exclusively from abroad. Shaped steel accounts for 60–65% of steel imports.

Until 2022, the main supplier was Russia’s Severstal. Subsequently, Finnish builders switched to rebar and shaped steel from Poland and Germany. Prefabricated steel structures are imported from Estonia. There, construction steel from non-EU countries is processed and then shipped to Finland as European-made products.

In euro terms, a significant portion of imports consists of premium-grade steel. It is purchased by Finnish engineering companies Wärtsilä and Valmet from the Swedish Ovako mills. Nevertheless, Finland firmly maintains its status as a net steel exporter—both in physical and monetary terms.

Demand for flat steel

Steel sales have been steadily declining over the past five years. At the same time, the share of flat steel in the consumption mix has been growing. Demand from the machinery manufacturing sector has remained stable, as indicated by the sector’s contribution to national GDP. The sector is strongly export-oriented, accounting for 50% of Finland’s exports.

Domestic consumption of sheet steel is primarily met by the local SSAB, making the market self-sufficient. Major buyers:

- Meyer Turku Shipyard. Builds the world’s largest cruise liners.

- Metso, a global leader in the production of crushers, mills, and conveyors for the mining industry.

- Hiab and Kalmar – major manufacturers of lifting and transport equipment. Hiab specializes in loader cranes, Kalmar in port loaders.

- Ponsse is a global leader in the production of forestry machinery.

- Patria is a major manufacturer of military armored vehicles.

Together, these five players account for 60–70% of flat steel sales in Finland. Also worth noting is the plant in Suolahti, which is part of the American corporation AGCO. The facility produces over 8,000 agricultural tractors per year.

Another major buyer is the Valmet Automotive plant in Uusikaupunki. It used to manufacture passenger cars for third-party customers. For many years, the company operated under a contract with Mercedes-Benz AG, but the current agreement expired at the end of 2025, and the German automaker chose not to renew it. This explains the decline in Finnish automobile production in 2025.

A niche player in the automotive industry is Sisu Auto. It manufactures heavy-duty trucks for the forestry industry and for military purposes. Production volumes here are stable—up to 1,000 units per year.

Amid stable demand from the machinery manufacturing sector and a decline in the automotive industry, shipbuilding and wind energy helped boost sales of flat-rolled steel.

- Under its contract with Royal Caribbean, Meyer Turku completed the construction of two Icon-class cruise ships and began building two more in 2025. The agreement calls for the construction of five ships. Each Icon-class ship requires 50,000–60,000 tons of heavy-gauge steel.

- Rauma Marine Constructions, the second-largest shipyard, completed a major order for a series of ferries for Tasmania in 2025.

Over the past 5 years, the installed capacity of Finnish wind farms has nearly tripled. Since 2021, the industry have been experiencing a real boom. In November 2025, the number of wind turbines in operation exceeded the psychological threshold of 2,000 units.

Demand for long products

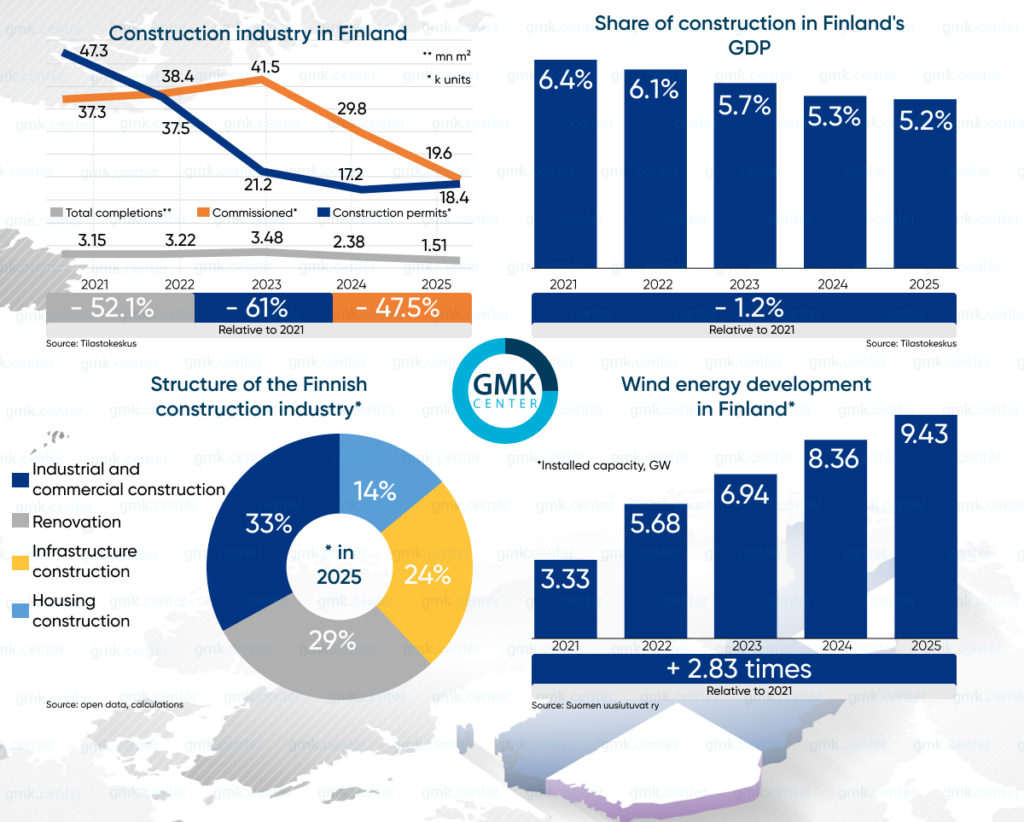

Finland’s construction sector, the main consumer, faced the consequences of the European Central Bank’s interest rate hikes in 2022–2025, which led to a drop in housing demand. This was compounded by a sharp rise in the cost of imported rebar and shaped steel from Germany and Poland.

This resulted in a record number of bankruptcies among small developers. In 2023—782, in 2024—747, and in 2025—768. By comparison, during the prosperous 2010s, an average of 450–500 companies closed annually in Finland’s construction sector.

In 2024–2025, the number of new residential construction starts fell to levels last seen in the 1990s. Compared to 2021, the market has shrunk threefold—to the physical minimum necessary to maintain the existing housing stock. In Helsinki and Tampere, the housing shortage has become critical.

In 2025, renovation projects accounted for around 50% of all completed residential construction work. Unlike new construction, building insulation projects involve very limited steel consumption.

As a result, long-product consumption fell from approximately 0.82 million tons in 2021 to 0.44 million tons in 2025. The decline would have been even steeper without government infrastructure projects and investment in data center construction.

Outlook for flat-product consumption

Shipbuilding remains the key driver. As of May 2026, the volume of new contracts for Finnish shipyards had increased by 18% compared to the previous year. Overall, the order book exceeds €10 billion.

- At Meyer Turku, the order book is filled through 2028–2030.

- Rauma Marine Constructions has begun work on a government contract to build four Pohjanmaa-class corvettes for the Finnish Navy. Delivery is scheduled for 2026–2029. The company has also received an order from the U.S. Coast Guard (USCG) to build two icebreakers under the ICE Pact international agreement. Delivery of the vessels is expected in 2029.

- Helsinki Shipyard, the third-largest shipyard, is also involved in this project through its parent company Davie. It will build two icebreakers for the USCG and one Polar Max heavy icebreaker for the Canadian Coast Guard (CCG).

Finland’s state program to modernize its icebreaker fleet, approved by the government in 2025, is unlikely to impact steel sales in 2026. The tender for the first icebreaker was announced in February and will conclude this fall. There is no doubt that one of the local shipyards will win the contract. However, actual purchases of steel sheets for the construction of this vessel are not expected until December at the earliest.

All of this allows us to forecast full capacity utilization of Finnish shipbuilding facilities for the next four years and guarantees stable consumption of sheet steel.

The continued expansion of the wind power sector will increase demand for flat-rolled steel. According to plans by the system operator Fingrid, the capacity of onshore wind farms is expected to reach 15–18 GW by 2030. An additional factor is the launch of offshore wind farm construction projects, which require significantly more steel.

Until now, offshore wind power has been virtually nonexistent in Finland. As of early 2026, its capacity stood at just 44 MW. However, by 2030, this figure is expected to rise to 1 GW—an increase of approximately 25 times.

Finnish utility companies, for their part, are promoting the development of wind energy. In 2025, they signed a record number of PPAs for the purchase of electricity from future wind farms. In other words, these facilities have not yet been built, but their output is already contracted for 10–15 years in advance.

With such long-term guaranteed buyers in place, energy companies have no trouble securing financing for construction. Additionally, the government has extended tax incentives for large green investments (€50 million and up) through the end of 2027. All of this makes Fingrid’s plans entirely realistic.

Demand for sheet steel from the automotive industry is expected to return to at least pre-crisis levels thanks to the agreement with Patria signed at the end of 2025. Valmet Automotive has announced that it will begin producing armored vehicles starting in 2026.

No figures have been disclosed, but it is worth noting the €400 million increase in Finland’s defense budget in 2026—bringing it to €6 billion. As announced, part of these funds will go toward replacing obsolete armored vehicles in the Army.

These factors, together with stable demand from the heavy machinery sector, support a forecast for flat steel consumption to increase by 2.6% in 2026, reaching 1.17 million tons.

Outlook for long-rolled consumption

The infrastructure sector will remain the main consumer of long products. In 2026, the Finnish government allocated €3.78 billion for the development of transportation networks. The most steel-intensive projects include:

- Modernization of the 116-km Riihimäki–Tampere railway line. In addition to replacing the track superstructure (rails and ties), the project includes the construction of new passing loops and signal boxes in Lempäälä, Kuurila, Leteensuo, and Turenki. Expenditures in 2026 will amount to €1.2 billion.

- Modernization of Highway 9. This includes, in particular, the construction of multi-level interchanges on the “Alasjärvi-Suinola” and “Tampere-Jyväskylä” sections, as well as a new bridge in the Lievestuore area. Expenditures for 2026 have been approved at €900 million.

- The «Military Mobility» program. This involves reinforcing existing bridges and roads to accommodate heavy military equipment. €200 million will be spent on these purposes in 2026.

Long-rolled consumption is projected to grow by 2.2%. Due to a 7% increase in the number of new building permits in 2025, the completion of new buildings in 2026 is expected to rise to 26.5–27 million m². The main driver will be the industrial sector (construction of data centers and green steel facilities), while the residential sector will continue to stagnate.

Overall, steel consumption is expected to rise to 1.62–1.65 million tons. This is very modest growth and still 15% below pre-crisis levels in 2021. However, a recovery trend is already visible.

-

02 July 2026

16 June 2026

10 June 2026

27 May 2026