Posts Global Market Türkiye 19334 19 February 2024

Local companies focus on the domestic market and expect to continue exporting to the EU after the introduction of CBAM

Turkiye is the eighth largest steel producer in the world. Over the past two years, its steel production and exports have declined due to global and domestic challenges. However, Turkish companies continue to invest in the expansion of production capacity, counting on the needs of the domestic market.

Production dynamics

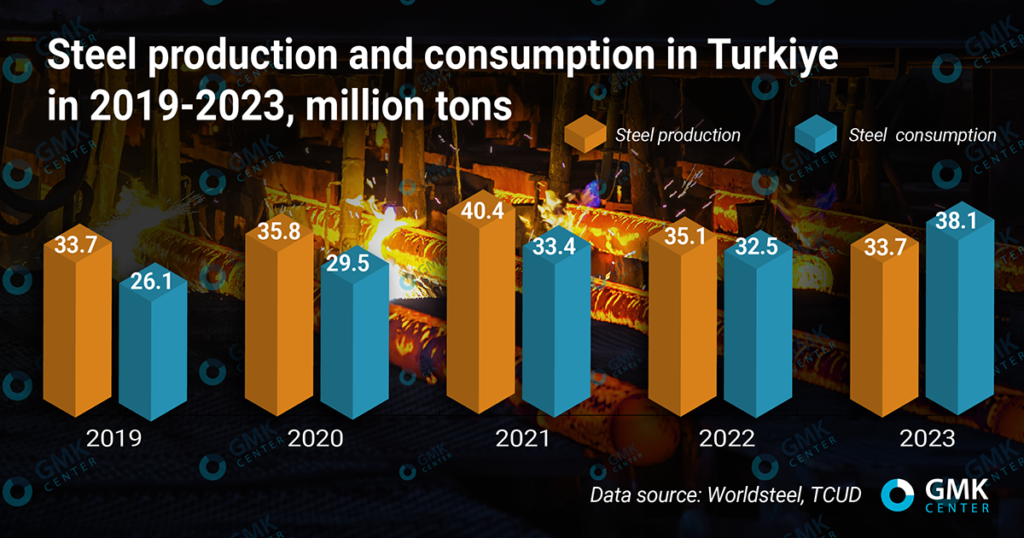

For the second year in a row, the Turkish steel industry has been on a downward trend, with Turkiye retaining its 8th place in the world ranking of steel producers. According to the Worldsteel Association, Turkish steelmakers will produce 33.7 million tons of steel in 2023 (down 4% y/y) and 35.1 million tons in 2022 (-12.9% y/y).

The decline in Turkiye’s steel production in 2022-2023 is due to macroeconomic instability, which has led to high uncertainty in the domestic market. As part of the fight against high inflation, which stood at 64.8% annualized in December-2023, the Turkish Central Bank raised the policy rate seven consecutive times during the past year. It rose to 42.5% per annum at the end of the year from 8.5% in June (the rate was raised to 45% per annum in January-2024).

However, the tightening of monetary policy did not help prevent the devaluation of the lira, which lost about 60% of its value against the dollar in 2023. On the one hand, the devaluation of the national currency restrains the inflow of imports, which become more expensive. On the other hand, the devaluation of the Turkish lira indicates serious problems in the economy, which also restrains growth of the domestic steel consumption.

Turkish steel industry is based on electric arc furnaces (in 2022, 71.5% of the country’s steel is produced by them), so rising electricity prices remain a major unfavorable factor for the steel industry. According to the Turkish Steel Exporters’ Union (CIB), electricity prices in Turkiye rose sharply in 2022 and accounted for 27% of steel mills’ production costs compared to 8% in 2021. Subsequently, gas and electricity prices for industry were slightly reduced in late 2022 and early 2023, but it was not possible to fully mitigate the impact of this factor on production costs.

Other factors affecting steel production and consumption in Turkiye include the increase in VAT on steel products from 18% to 20%. This decision has a negative impact on the prospects of the domestic market, as it means higher prices for rolled steel products.

The earthquake that occurred in February 2023 also had a negative impact on the Turkish steel industry, as one third of steel plants were forced to temporarily halt production. Subsequently, it was expected that mills would be able to at least partially recover losses as demand for steel products for construction projects aimed at overcoming the consequences of the earthquake would increase.

Consumption of rolled steel products did rise in 2023 (up 17.1% y/y – to 38.1 million tons compared to 2022), but this additional demand did not help avoid a 4% y/y drop in steel production. Turkish steelmakers complain that the increase in demand was covered by imported steel products. According to the Turkish Steel Producers Association (TCUD), steel imports to Turkiye increased by 15.5% y/y in 2023.

The decline in Turkiye’s steel production in 2022-2023 also led to a decrease in ferrous scrap consumption and imports. According to SteelMint, Turkiye’s ferrous scrap consumption in 2023 fell 6% y/y – to 27 million tons compared to 2022. According to the Turkish Statistical Institute (TUIK), the country reduced its scrap imports by 10% year-on-year – to 18.83 million tons in 2023. The top five largest suppliers include the US and European countries (the Netherlands, Belgium, the UK, Romania).

The European Steel Association is pushing for stricter controls on scrap exports. The first steps in this direction have already been taken – from January 2024, a new Waste Shipment Regulation will come into force, which sets technical barriers for scrap exports to countries outside the Organization for Economic Cooperation and Development (OECD). In case of further tightening of conditions for scrap exports from the EU, Turkiye risks facing a shortage of raw materials for its own steel industry.

Export-import

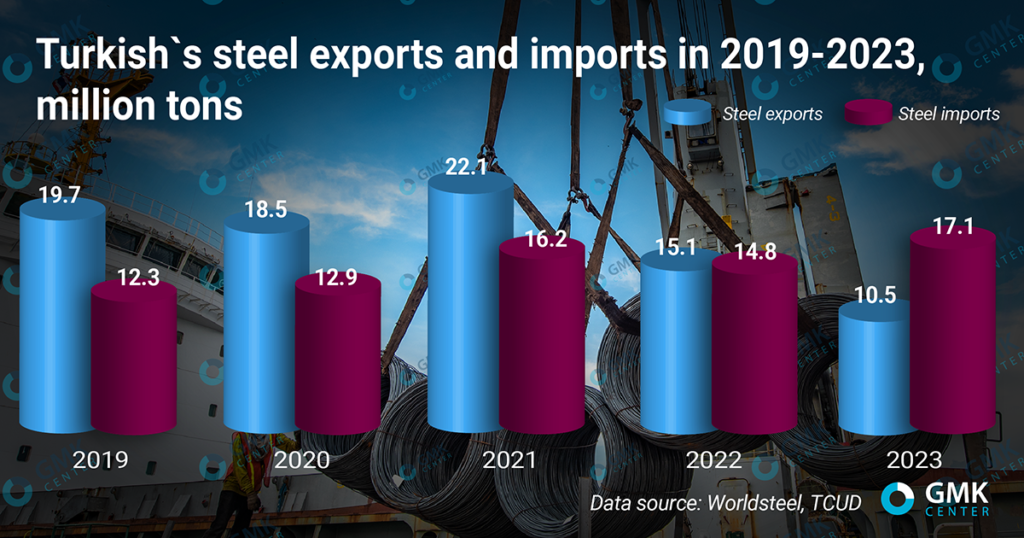

For the second year in a row, Turkiye’s steel exports have shown a negative trend. According to the Turkish Steel Association (TCUD), the country’s steel exports fell by 30.6% year-on-year in 2023 – to 10.5 million tons. Export revenue decreased by 40.7% year-on-year – to $8.3 billion. In 2022, steel exports from Turkiye decreased by 23.5% year-on-year – to 15.1 million tons.

In January-November 2023, imports of steel (including semi-finished products) to the European Union from Turkiye decreased by 51% y/y (average monthly imports for 11 months of 2023 – 199 thousand tons). In 2022 import of Turkish rolled steel products to the European market decreased by 6% – to 4.33 million tons. Its share in the EU market in 2022 amounted to 15%.

The reduction in steel exports from Turkiye is due to:

- Energy price differentials around the world. Higher electricity prices in Turkiye have reduced the competitiveness of local producers, while companies from other countries with cheaper energy sources have been able to increase supplies to foreign markets.

- Active protectionist policies in key export markets. The EU and the US continue to protect local producers from the influx of imports through duties and quotas. In the US, Section 232 (25% duty) applies to Turkish steel products. Export opportunities to the EU are limited by a quota system. In addition, the EU has an anti-dumping duty on Turkish hot-rolled sheets.

- Increased steel exports from China due to decreased domestic consumption. China is again faced with overproduction of steel, the surplus of which is “pushed” to external markets. This has a negative impact on prices and export opportunities for other countries.

- Continued supply of steel products from Russia with reputational discounts. Russian suppliers offer lower prices for their steel products to interest consumers in foreign markets. Such supplies, as in the case of increased steel exports from China, also have a negative impact on prices and export prospects of other countries.

Turkiye has not imposed sanctions against Russia, so Turkish companies continue to work with Russian producers, in particular Turkiye imports pig iron and steel semi-finished products from Russia.

«Turkiye has the opportunity to process these raw materials and get higher value-added products that can be exported to the EU and other countries. Of course, the EU sanctions policy includes a ban on imports of steel products made with Russian steel. However, we do not know how the verification mechanism works in practice and how effective it is,» says GMK Center analyst, Andriy Glushchenko.

In addition, Turkish producers may use Russian semi-finished products to produce products for the domestic market, while products made of other raw materials may be exported to the EU. Russian raw materials can thus increase export opportunities from Turkiye.

Currently, this practice has not become widespread. As shown above, steel exports from Turkiye to the EU are falling, Turkish suppliers are losing price competition in the EU market. At the same time, Turkiye is facing an influx of imports. The significant imports has led Turkish industry associations (TCUD, CIB) to demand that the authorities take measures to protect the domestic market.

As a result, in 2022 Turkiye imposed import duties on hot-rolled steel from the EU. In May 2023, import duties on certain types of flat rolled products were raised by an average of 7%. In particular, for hot-rolled coil – from 9% to 15%, cold-rolled coil – from 10% to 17%, alloyed hot-rolled coil – from 6% to 14%. TCUD positively assessed the impact of this measure on the work of Turkish steelmakers.

In 2024, the trend to strengthen trade protection continues: in January, duty rates on certain types of flat rolled products were raised, and a temporary duty on imports of wire rod was introduced. In the near term, anti-dumping duties may be introduced on hot-rolled coils from China, Japan, India and the Russian Federation. A review of anti-dumping measures on welded stainless steel pipes from China and Taiwan has also been initiated.

Steel prospects

Analysts expect the Turkish steel market to improve this year, driven by global growth in steel demand, lower interest rates in the world and others. In its October-2023 report, the Worldsteel Association forecasts steel consumption in Turkiye to grow by 5% – to 40.6 million tons in 2024.

«Turkish steel demand is expected to grow in 2024. Steel demand will benefit from the earthquake-related construction activities and the abandonment of its unconventional monetary policy that drove foreign investment out of the country.,» Worldsteel said.

The TCUD association predicts domestic steel demand will grow in 2024, supporting investment and new capacity coming online in the second half of 2023. In general, Turkish producers Kardemir, Yıldız, Colakoglu Metalurji, Hasçelik have planned multi-million dollar investments in new production capacity for 2024 and beyond. Turkish companies want to increase the production of higher value-added products for domestic needs due to difficulties with exports.

Turkiye has a large and growing domestic market, so the future prospects of its steel industry will be based on meeting its needs. Potentially, Turkiye has a chance to continue exporting to the EU, as after the introduction of CBAM scrap-based steel production gives Turkish steelmakers an advantage in the European market compared to other importers.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

17 July 2026

14 July 2026

16 June 2026