shutterstock")

Posts State macroeconomics 575 25 May 2026

Amid rising inflation, Ukraine faces the threat of a recession and, under certain circumstances, stagflation

The first quarter of 2026 confirmed alarming trends in the Ukrainian economy: real GDP contracted, business activity fell to a three-year low, and inflationary pressures are mounting. Against this backdrop, the government submitted a new 15-year strategy, “Economy of the Future,” for consideration, but experts have questioned its feasibility. At the same time, concerns are rising about the risk of stagflation—a combination of economic decline and persistent inflation.

A negative start of the year

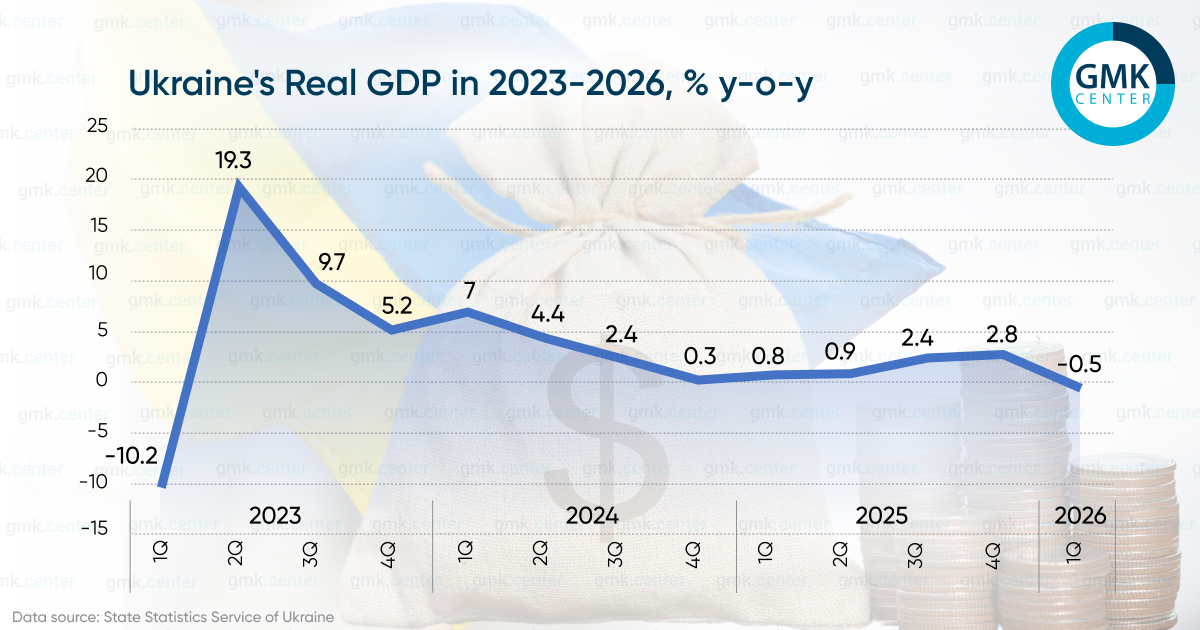

As expected, the Ukrainian economy contracted at the start of the year. According to a preliminary estimate by the State Statistics Service, real GDP fell by 0.5% year-on-year in the first quarter, or by 0.7% compared to the previous quarter (seasonally adjusted). At the same time, the National Bank of Ukraine assessed economic growth for the same period differently—as a 0.2% year-on-year increase.

Commenting on the State Statistics Service’s data, Ukrainian Prime Minister Yulia Svyrydenko was quick to assure that Ukraine’s GDP grew by 0.9% year-on-year in April, which helped reduce the economic decline for January–April to 0.2% year-on-year.

The Ministry of Economy’s calculations and forecasts should be treated with caution: previously, the ministry estimated GDP growth in 2025 at 2.2% year-on-year, while data from the State Statistics Service and the National Bank of Ukraine showed an increase of only 1.8% year-on-year.

Key factors behind the economic contraction in the first quarter:

- Power shortages. As a result of shelling targeting energy infrastructure in January, many industrial enterprises partially or completely suspended operations. Consequently, industrial output declined by 1.1% year-on-year in the first quarter.

- Cold winter. Low temperatures halted work at most construction sites, leading to a 4.7% year-on-year decline in construction activity in January–March.

- Rising energy costs. Following the escalation of tensions in the Persian Gulf, prices for gas and petroleum products in Ukraine rose significantly. At the same time, the electricity shortage led to higher electricity prices.

- Impact of CBAM. Ukraine did not receive a deferral or exemption from the Carbon Border Adjustment Mechanism (CBAM), which led to the loss of 1.1 million tons of export orders from the EU for steel products and a 7–9% reduction in steel and rolled steel production.

- Restrictions on maritime logistics. Due to electricity shortages and damage to port infrastructure caused by constant shelling, the physical volume of maritime exports has significantly decreased.

“The economic downturn in the first quarter is a completely predictable outcome: growth had been slowing since 2024. Current economic policy, combined with frustration over the protracted war, is fueling persistent business pessimism—primarily among companies not tied to the defense sector,” noted economic expert Danylo Monin in a comment to GMK Center.

Another sign of the collapse in business activity is the decline in the business activity recovery index. According to estimates by the Institute for Economic Research and Policy Consulting (IER), this index deteriorated significantly, falling to −0.11 in April (compared to 0 in February and March). This is the lowest index value since March 2023.

The situation in the business environment shows a noticeable cooling: only 5.6% of surveyed companies say their business is doing better than a year ago, although as recently as March this figure was nearly four times higher—19.6%. At the same time, 19.6% of respondents report a deterioration in their business conditions. The vast majority of entrepreneurs—as many as 74.8%—have not noticed any changes at all compared to last year; their share has increased significantly from 60.8% in March.

In other words, Ukrainian businesses retain the ability to adapt to new conditions and maintain production processes, yet they are demonstrating increasingly poor operational resilience, as the overall business situation in the country has deteriorated significantly in recent times.

“The Ukrainian economy is showing signs of adaptive recovery but remains vulnerable to three key shocks: military risks, import dependence, and currency-inflationary pressures,” notes Bohdan Danylyshyn, Chairman of the Board of the National Bank of Ukraine from 2016 to 2022.

At the same time, inflationary pressure is mounting, fueled by devaluation risks, rising import costs, and a fiscal deficit financed primarily by external transfers.

“After a period of deceleration, inflation began to accelerate—due to rising energy prices, the consequences of shelling, rising fuel prices amid the war in the Middle East, the previous weakening of the hryvnia, and accelerated wage growth. In March, inflation reached 7.9% year-on-year. The NBU expects inflation to rise to 9.4% by the end of 2026,” according to the NBU’s April Inflation Report.

Another strategy as a «way out» of the crisis

Along with the release of dismal macroeconomic statistics for the first quarter, the government unveiled a new 15-year economic strategy titled «Economy of the Future.» The document calls for achieving an average annual GDP growth rate of 6% and increasing the share of investment in GDP to 24–30% per year, up from 16% before the war.

“For now, the figure of 6% average annual growth seems like an ambitious plan that we would very much like to see become a reality. However, achieving this target requires the simultaneous fulfillment of several conditions: sustainable external financing of at least $15–20 billion per year, large-scale deregulation and judicial reform to attract private capital, the restoration of human capital through the return of migrants, as well as security stability to revitalize the investment cycle,” said Dmytro Churin, director of the analytical department at investment firm Eavex Capital, in a comment to GMK Center.

Currently, the economic strategy is effectively represented by just four slides in a presentation. According to the experts surveyed, this initiative gives the impression of an attempt to pass off minimally developed material as the result of prolonged work by large teams.

“There are sufficient grounds for such an assessment. The stated theses on economic liberalization in the complete absence of tax reform resemble selling a pig in a poke. If even now, with fiscal stimulus at $60 billion per year, the economy is in the red, and the forecast for government spending reaches 80% of GDP, there is no point in counting on improvement without a radical change in the economic model. The conclusion is obvious: beyond the four slides of wishful thinking, there is no real substance,” notes Danylo Monin.

According to Dmytro Churin, the focus should not be on what GDP growth figure to include in the strategy, but on how to launch mechanisms for sustainable economic growth in conjunction with the development of industrial production and the expansion of exports of goods and services with high added value.

Clearly, the timeline for achieving this strategy’s goals will not begin this year. In April, the NBU lowered its GDP growth forecast for 2026 to 1.3% year-on-year from the previous 1.8% year-on-year. The government’s forecast, as laid out in the 2026 state budget, currently projects 2.4% growth; however, it will most likely be revised downward by mid-year—in particular due to the negative impact of winter shelling on the energy sector.

The problems run deeper

Behind the development of yet another strategy lies a much deeper problem: the Ukrainian economy lacks growth drivers and a government economic policy designed to stimulate growth amid the war. Since the start of the full-scale invasion, economic management has been largely reactive, responding to existing challenges and mostly in “manual mode,” rather than consistently within the framework of systemic strategies. Moreover, the government’s practice of creating economic strategies resembles a mere formality: either the previous document has expired, or it is required by agreements with international partners.

Furthermore, no government official has personally reported to parliament or civil society for a long time—particularly regarding the reasons for the failure to implement previous strategies—and, accordingly, bears no personal responsibility. As a reminder: three years ago, then-Minister of Economy Yulia Svyrydenko presented a strategy for Ukraine’s recovery at the Ukraine Recovery Conference, in which she promised GDP growth to $1 trillion over 10 years at an average annual rate of 7.2%. Instead, in 2023, the economy grew by 5.3% year-on-year, in 2024 by 2.9% year-on-year, and in 2025 by 1.8% year-on-year.

Moreover, against the backdrop of rising inflation, Ukraine faces the threat of a recession with a possible transition to stagflation. In its forecast, the investment firm Capital Times expects Ukraine’s GDP to decline in the second and third quarters of this year by 2.3% y/y and 1.4% y/y, respectively. Although this completely contradicts the NBU’s forecast for the same period (growth of 1.7% y/y and 1.9% y/y, respectively), any contraction of the economy in the second quarter will already signify a recession (a decline in GDP for two consecutive quarters).

“A recession during wartime is the collapse of the military Keynesianism model (or evidence that this model was never actually implemented). To some extent, this is a death knell for the government’s economic bloc… The inability to utilize the tools of military Keynesianism (a broad range of tools and compensators in the form of high levels of government spending—ed.) is the real reason for the decline in GDP amid active hostilities. “If Ukraine were currently developing with a balanced foreign trade balance, we could be growing at a rate of over 5%,” says economist Oleksiy Kushch.

The “recession + inflation” formula, in turn, corresponds to the classic definition of stagflation.

“Classic stagflation involves a combination of falling domestic production and persistent inflation. Ukraine is at risk of precisely this scenario—especially if external financing dries up and the NBU’s monetary policy shifts toward lowering interest rates. For now, the NBU is maintaining a hardline stance, and this serves as a certain restraining factor for both inflation and the hryvnia exchange rate,” says Dmytro Churin.

Instead of adopting concrete anti-crisis measures amid an economic downturn and the emergence of critical long-term threats in the context of war, the government chose the traditional path—it presented yet another strategy with declarative goals that are detached from reality. Since this is not the first such precedent, there is only one conclusion: without a radical change in approaches to managing the economy during wartime, the government will not be able to reverse the negative economic trend that has already firmly taken hold.

Thus, the key problem remains not a lack of strategies, but the absence of effective drivers of economic growth and a systematic economic policy in the context of a protracted war.

-

OpinionsStatesteel consumption

13 July 2026

30 June 2026

02 March 2026

26 January 2026