Posts Global Market ArcelorMittal 2366 11 August 2025

Structural challenges, high energy costs, and shifting global trade flows are reshaping local steel sector

Poland has long been recognized as a key industrial hub in Central Europe, with steel production serving as one of the foundational pillars of its economy. For decades, the country maintained a robust steel sector, supported by capacities of steel mills and skilled labor force. Polish steel was not only a symbol of national industrial strength, but also an important component of regional supply chains.

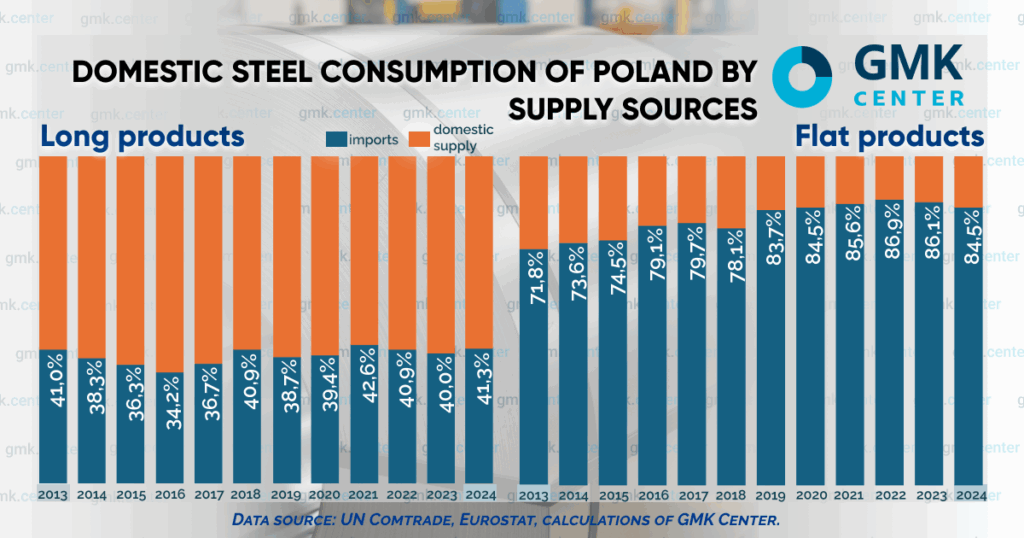

However, over the past decade, Poland has cut its crude steel output by 22.8% – a sharper decline than the 16.6% drop recorded in the EU. As a result, an increasing share of domestic steel demand is now filled by imports. In 2024, imports accounted for 84.5% of Poland’s consumption of flat finished steel products. For long steel products, imports covered 41.3% of domestic demand.

The persistently high share of imports, particularly in the flat steel segment, points to a structural crisis in Poland’s steel industry. As a result, the country is undergoing a profound transition from a steel-producing nation to a steel-consuming one increasingly reliant on foreign suppliers. To understand the drivers behind this transformation, it is essential to examine the broader factors shaping the Polish and European steel industry landscape.

ArcelorMittal Poland

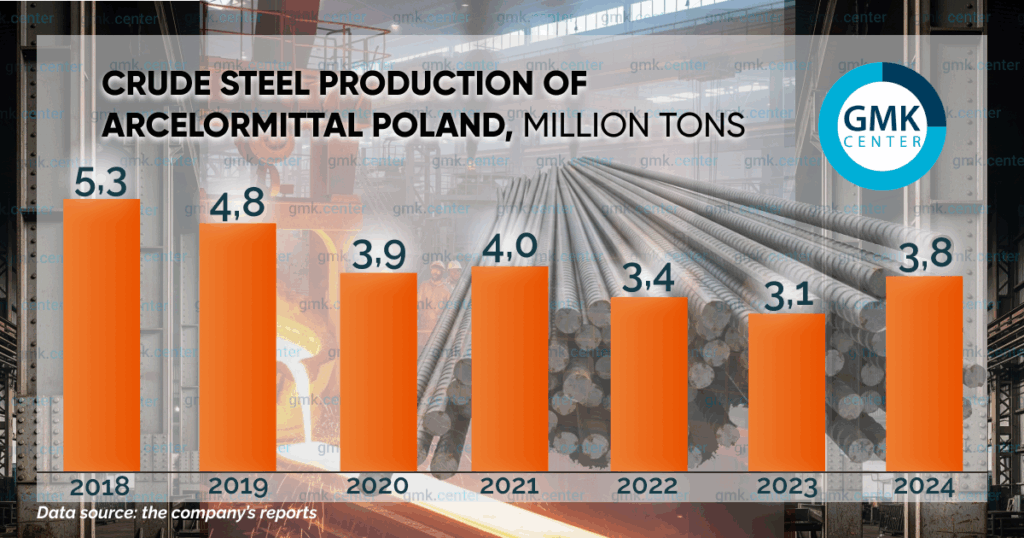

In fact, Poland has become a victim of corporate optimization inside ArcelorMittal, with its steel production shifting to other countries. ArcelorMittal Poland, which is the country’s largest steel producer, accounts for more than half of national crude steel output. The company operates production facilities in Dąbrowa Górnicza, Kraków, Sosnowiec, Świętochłowice, Chorzów, and Zdzieszowice. ArcelorMittal acquired these plants during the privatization process. Its first years of ownership coincided with a global steel market boom (2004-2007), delivering strong production and financial performance. However, conditions later deteriorated. Between 2018 and 2024, ArcelorMittal Poland’s crude steel output declined by 28.3%.

Instead of developing local production, ArcelorMittal suspend Polish facilities. In particular, in 2020 ArcelorMittal closed BF-BOF operations at Kraków plant, remaining Dabrowa Gornicza as the only own operating integrated steel plant. In July 2024, ArcelorMittal permanently closed the coke oven battery in Kraków, followed by the shutdown of coke oven battery No. 6 at the Zdzieszowice plant in December 2024.

The company traditionally cites weak market conditions, insufficient protection against imports, and high carbon costs as key reasons for decreasing production and idling facilities. At the same time, nearly 37% of Poland’s flat steel imports originate from Germany, France, and Belgium – countries where ArcelorMittal operates plants specializing in flat-rolled products. This suggests that ArcelorMittal may be supplying the Polish market from its other European sites. In such case each shutdown of domestic steelmaking capacity in Poland opens way for more such imports.

Russian impact

Since the introduction of sanctions, Russia has emerged as a major destabilizing force in the European steel market, and now its actions continue to put pressure on prices. In 2021, Russia was the largest supplier of imported uncoated flat products to Poland, accounting for 20% of total imports. The ban on Russian finished steel introduced in 2022 could have potentially supported domestic production, but this did not materialize. The EU left the door open for continued imports of Russian semi-finished products, particularly slabs.

While the 8th sanctions package, adopted in October 2022, called for a full stop to Russian slab imports by October 1, 2024, the 12th package, adopted in October 2023, extended the timeline. Under the revised rules, Russian slab imports are allowed until the end of September 2028, though subject to quotas. For the period October 1, 2024 to September 30, 2025, the quota is set at 3.2 million tons, and it will be reduced to 3.0 million tons for the following 12-month period.

In 2024 the EU imported 3.1 mln tons of slabs from Russia, in 5m 2025 – 1.5 mln tons. The main importers of Russian slabs are Belgium (1.3 mln tons in 2024), Italy (0.7 mln tons), Czechia (0.5 mln tons), Denmark (0.5 mln tons).

The extension of these supplies was lobbied by European re-rolling plants whose business models rely on Russian slabs. Russian suppliers can offer so-called «reputational discounts,» with official price offers typically $20-30/t lower than those from other sources. However, the actual price gap may be even larger. Imports of Russian slabs provide buyers with a pricing advantage. Struggling to sell their finished products, they may push prices even lower, further straining the financial position of steel producers across Europe, and Poland is no exception.

Following the shutdown of its steelmaking units, the Kraków plant operated using slabs supplied from Dąbrowa Górnicza. However, this business model obviously loses out to both European integrated producers and re-rolling plants processing discounted Russian slabs. In general, Russian slab imports erodes the competitiveness of European steelmakers, damaging local crude steel production.

Indonesian factor

The current challenges facing the Polish steel market are not driven by a surge in import volumes. According to UN Comtrade data, during the 5m 2025, imports of flat finished steel products increased by only 1.0% year-on-year, while imports of long finished products declined by 0.9%. In other words, import levels have remained largely stable.

The real problem is cheap Asian imports which forces other suppliers to reduce their prices to stay competitive. In this context Indonesia has become the biggest trouble for European market. As a developing country, Indonesia is exempt from the EU’s steel safeguard measures. This allows Indonesian steel producers to export to the EU without restrictions.

Indonesian suppliers have adopted an aggressive pricing strategy: their HRC offers are €20-25/t lower than Turkish offers and €25-30/t below Indian ones. As a result, Indonesia is the most competitive source of HRC for European steel consumers. The sharp decline in HRC prices during May-June 2025 was largely driven by the actions of Indonesian suppliers.

Although Poland’s HRC imports from Indonesia rose by just 3.2% y-o-y in 5m 2025, total HRC shipments from Indonesia to the EU more than doubled, increasing 2.4 times. These low-cost imports put pressure on the European HRC market, undermining prices, squeezing the margins of local producers, and limiting their ability to increase production. Polish steelmakers are also feeling the impact, as they cannot remain isolated from broader European market conditions.

“Green” policy

Poland also faces some of the highest electricity prices in the EU, contributing to stagnation in the country’s steel industry. As a result, domestic production is increasingly being replaced by imports from other EU member states. According to data for 5m 2025, intra-EU deliveries accounted for 77% of Poland’s imports of long steel finished products and 75% of flat steel imports.

In 2024, the average day-ahead market price in Poland was €96/MWh, and as of early August 2025, it stands at around €80/MWh. This situation is largely driven by the country’s reliance on fossil fuel-based power generation, combined with EU green policies pushing member states to phase out carbon-intensive energy sources.

In Poland, 55% of electricity generation in the country is coal-based. Total share of fossil fuels in electricity generation reaches 69%. Under these conditions, a rapid refusal from fossil fuels is unrealistic. However, rising CO₂ prices in the EU are already putting financial pressure on power producers by driving up their carbon costs. Since the electricity sector does not receive free carbon allowances, higher CO₂ prices directly contribute to rising electricity prices.

High electricity prices make EAF-based steel production uncompetitive. Last year in Poland EAF capacities were utilized by only 58%, although BF-BOF capacities – by 77%. While the development of EAF capacities could be a foundation for decarbonizing Poland’s steel industry, high power costs are a major barrier. According to a Reuters forecast, electricity prices in Poland are expected to remain high, reaching €107/MWh by 2035, further damaging Polish economy.

Conclusions

Poland’s growing reliance on steel imports reflects deep-rooted structural challenges that erode the competitiveness of its steel sector and, more broadly, its economy. High energy costs, limited modernization, and persistent exposure to cheaper foreign supply have steadily weakened domestic steel production capacities. Current market conditions, such as aggressive pricing from non-EU suppliers, loopholes in steel safeguard measures and continued inflows of Russian semi-finished steel, put additional pressure on the market.

Since the core issues are systemic, safeguarding the future of Polish steel industry will require coordinated, long-term strategies at both corporate and governmental levels. It is necessary to restore competitiveness and reinforce the sector’s resilience against external shocks. Without such measures Polish steel industry will continue losing market positions.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

16 June 2026

10 June 2026

27 May 2026