News Global Market flat & long steel prices 58 12 July 2026

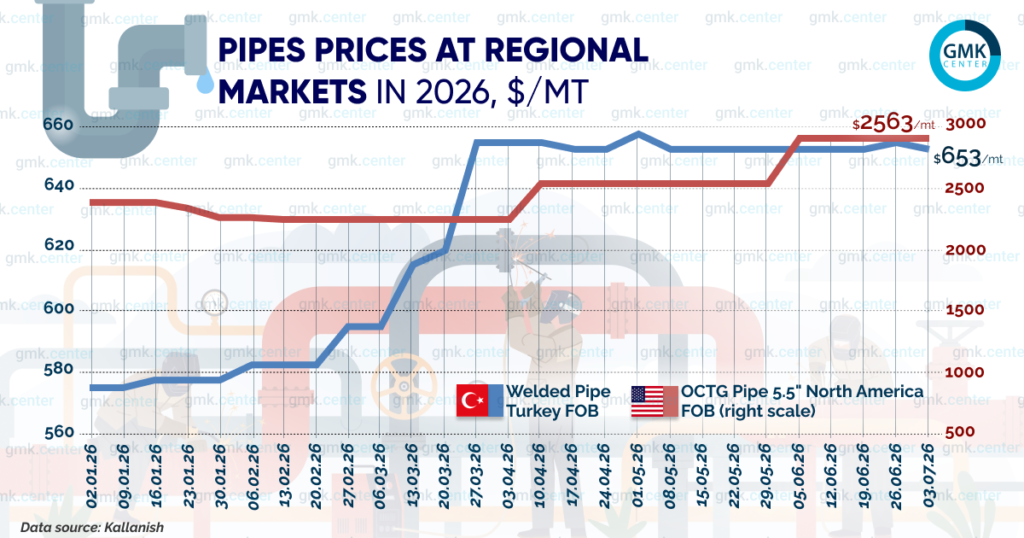

Prices for Turkish welded pipes rose by $3 per tonne over the same period

Regional pipe markets are seeing mixed trends, linked to the specific characteristics of pipe products. By the end of June, prices for welded pipes in Turkey, intended for construction purposes, had risen slightly, whilst quotations for oil and gas OCTG pipes in the US had stabilised at $2,563/t.

USA

Average prices for OCTG pipes on North America FOB terms jumped by a further $289 per tonne at the start of June, reaching $2,563/t. However, prices had remained stable at $2,274/t for almost the whole of May.

Meanwhile, trends in the number of active drilling rigs in the US continue to point to rising investment in drilling. According to Baker Hughes, the number of oil and gas drilling rigs in the US – an early indicator of future production – stood at 573 at the end of June, an increase of 11 units over the month. In the final week of June, the increase was 10 rigs, marking the largest weekly rise in the last four years.

Furthermore, investment in the pipe segment itself is also on the rise. US Steel is to allocate $475 million to expand steel processing capacity for the production of oilfield pipes at its Fairfield Tubular Operations plant in Alabama. Full capacity is scheduled to be reached in the second quarter of 2029.

The US oil industry is also showing no signs of slowing down. In April, the US set a historic record – oil production rose to 13.4 million barrels per day, an increase of 216,000 barrels per day compared with March.

As predicted, WTI prices showed a downward trend throughout June. Over the past month, average WTI prices fell by 16.3 per cent – to $85.5 per barrel from $102.1 per barrel in May. The main drivers of the decline were a reduction in geopolitical risks in the Middle East, the reopening of the Strait of Hormuz and an increase in oil production volumes. However, the situation remains unstable.

Turkey

According to Kallanish, prices for welded pipes rose slightly in June – by $3 to $654/t (Turkey FOB). Turkish pipe producers maintained high export prices, even despite falling prices for hot-rolled coil (HRC) and scrap. This is due to demand from Europe, as many European distributors sought to build up stocks ahead of the introduction of new protective measures in the steel market.

The introduction of the EU’s new quota system has added uncertainty for Turkish pipe exporters, for whom the EU remains the largest export market. In particular, the quarterly quota for hollow sections from Turkey has been reduced by 40 per cent to 60,000 tonnes.

At the same time, domestic market conditions remain weak. According to the Turkish Statistical Institute (TUIK), the business confidence index in Turkey’s construction sector recovered in June, rising by 1.1 points to 83. Although the construction activity index has risen over the last three months to 89.4 from 85.3 in May, the situation in the sector remains weak, as the index is below 100 – indicating pessimistic sentiment.

As noted above, average prices for HRC, which is the raw material for the production of welded pipes, fell by $20 in June to $605/t (on Turkey FOB terms). One of the factors behind the price decline towards the end of the period was the reduction in EU quotas for imports of Turkish HRC.

It should be recalled that, at the end of May, prices for welded pipes in Turkey intended for construction purposes fell slightly, whilst quotations for oil and gas OCTG pipes in the US once again jumped by almost $290 per tonne – to $2,563/t.

-

02 July 2026

12 July 2026

11 July 2026

10 July 2026