Posts Green steel green steel 1793 15 September 2025

Australia can play an important role in the decarbonization of Asia-Pacific metallurgy

Australian steel companies are taking different paths to achieve carbon neutrality. The first one is based on proven and available technologies that guarantee the result. The second involves the development of fundamentally new solutions capable of turning the steel market upside down. As a result, some companies already have clear benchmarks for reducing greenhouse gas emissions. Others are still quite uncertain.

In both cases, decarbonization will lead to a structural transformation not only of the steel industry itself, but also of the iron ore industry – the backbone of the Australian economy. Therefore, changes in the industry are receiving serious government support.

The main players in the industry are divisions of large international corporations BlueScope and Liberty Steel. Australian Steel Products Ltd. is part of BlueScope. It owns Port Kembla Steelworks (New South Wales) with a capacity of over 3 million tons of steel per year. It is a leading producer of flat-rolled products. Liberty Steel’s main asset is Whyalla Works (South Australia) with a capacity of 2.6 million tons of steel, the largest producer of long products.

The combined melt output of these facilities in 2024 amounted to 4.8 million tons. This is down 11% from a year earlier. The decline reflects the problems of the Australian steel industry: high cost of natural gas and weak domestic market protection in the face of aggressive imports from Southeast Asia.

Both mills operate on BF-BOF technology and now have average emissions of 2.07 tons per 1 ton of crude steel. The owners of the mills are actively pursuing decarbonization as the Australian government aims to achieve a carbon-free economy by 2050.

EAF transition with a question mark

Liberty Steel Australia can be considered the pioneer of the process. It has staked on the EAF transition. To this end, GFG Alliance, Liberty Steel’s parent company, contracted Italy’s Danieli in April 2023 to supply equipment and build a 1.6 million tpy EAF to replace the existing BF. The new furnace will be powered by electricity from renewable energy sources (RES). The project was expected to be completed by the end of this year at a cost of $485 million.

Plans also include the construction of a 1.8 million tons per year DRI plant, here in Waialae. This facility will produce products from raw materials mined at Liberty Steel Australia’s Tamura iron ore plant in New South Wales. The cost of this project is estimated at $593 mln. Thus the company will solve the problem of resource supply of EAF-production. Which, as it is known, cannot use ordinary iron ore for steelmaking.

The challenge for the project is the limited supply of NG in South Australia, which is necessary to produce DRI. The construction of a floating LNG terminal at the Port of Adelaide, previously announced by Venice Energy Group, could offset the risks in the first phase. Its representative specified that the facility is aimed at receiving imported LNG. Probably from the Middle East.

In the future, DRI’s production at Wyalla is planned to switch to green H2 instead of NG. The hydrogen plant should become a part of the future complex.

Layout of the H2 production plant in Wyalla

Source: South Australian State Government

Liberty Steel Australia therefore intends to switch to emission-free steelmaking as early as 2030. However, the realization of this plan is in question, based on the difficult situation of the European assets ofGFG Alliance.

Liberty Steel, a member of the GFG Alliance, is facing serious financial difficulties after the bankruptcy of its main creditor, Greensill Capital, in 2021. Therefore, the Czech mill Liberty Ostrava was sold to SPV NH Ostrava and SPV NH Koksovna.

Liberty Steel plants in Luxembourg (Dudelange) and Belgium (Liege) have not found any buyers for 2 years, and, apparently, they are close to final closure. The Romanian steel mill Liberty Galati is in bankruptcy and management has been transferred to a consortium of administrators. Hence doubts about Liberty Steel’s ability to decarbonize its Australian assets by 2030.

A new concept for EAF transition

This option has been chosen by another company, Green Steel of Western Australia (GSWA). This is a new player that has decided to enter the local market in anticipation of the prospects associated with the growing demand for green steel.

Right now, the company does not have its own production facility. But it is building an EAF plant in Kohli with an annual capacity of 450,000 tons. The plant will produce rebar and wire rod. Commissioning is scheduled for 2026-2027.

Layout of the electromet plant in Collie

Source: Australian Government

GSWA is also building a DRI plant in Geraldton. Its design capacity is not disclosed. But it is known that the volume of investments will amount to $1.74 billion. i.e. it is a large enterprise with capabilities far exceeding the company’s own needs. Therefore, it is obviously planned to export its products.

The plant in Geraldton will start working on NG-DRI technology, in the future it is planned to switch to H2-DRI. Both enterprises of GSWA intend to use RES energy, i.e. it will be completely green production at once. The equipment for them will be supplied and installed by Danieli.

This is a good strategy with a modern concept. As you know, it is easier for small EAF plants to adapt to market realities and customer demands. They have more flexible marketing compared to large manufacturers. Well, in the conditions of decarbonization DRI is needed everywhere. And first of all, steel companies in Southeast Asia, which will soon start looking for a replacement for traditional pig iron.

Betting on green iron

BlueScope has chosen a different path. By 2030, the company will reduce CO2 emissions by 12% compared to the base year of 2018 for Scope 1 and 2 and 30% for Scope 3. This is expected to be achieved by increasing the share of scrap in raw materials to 30% from the current 25.4%. It also plans to partially replace coal in BF with biochar and ramp up the use of PCI coal dust instead of coke.

In the future, BlueScope will abandon blast furnace production in favor of green iron produced in ESF electric smelting furnaces using H2 and RES. The corresponding technology is currently being developed. The NeoSmelt project also involves local corporations Rio Tinto and GNR. In December 2024, the consortium selected the Kwinana industrial zone south of Perth to build a 40,000 tpa pilot ESF. It is scheduled to be commissioned in 2028.

The success of the research is difficult to predict. In addition, commercialization of H2-ESF-BOF technology will depend on the availability of green hydrogen at affordable prices. BlueScope therefore does not set targets beyond 2030 in its roadmap, limiting itself to striving to achieve carbon neutrality by 2050.

The participation of major iron ore exporters Rio Tinto and GNR in NeoSmelt is not accidental. As is well known, they are among the main suppliers to steelmakers in Southeast Asia (SEA). BF-BOF technology is now predominant almost everywhere there. But the challenges of decarbonization dictate the need to switch to either EAF or hydrogen pig iron production. This means there is a need for new types of green iron ore raw materials.

For example, DRI. But it is problematic to transport it over the distances separating Australia from China, Japan, South Korea – the properties of the material are lost. In addition, according to Geraldine Slattery, Chief Executive Officer of BHP Australia, Australian DRI will not withstand competition.

«Even with generous political support, the cost of production will be twice as high as in the Middle East or China – and customers are thousands of kilometers away,» she stressed, speaking at the Australia-China Economic Forum in Shanghai in July this year.

Green iron is another matter. That is why the third largest iron ore exporter Fortescue is also engaged in a similar project. The corporation has invested $50 million in the construction of an experimental ESF in Christmas Creek (Western Australia). Its launch should take place by the end of this year.

And now it remains to be seen who will be the first to commercialize the H2-ESF: NeoSmelt or Fortescue? Either way, green iron could indeed become the backbone of the nation’s steel exports, given Australia’s RES and H2 production capabilities. In fact, it will usher in a new era for the global steel industry.

Government support for the green transition

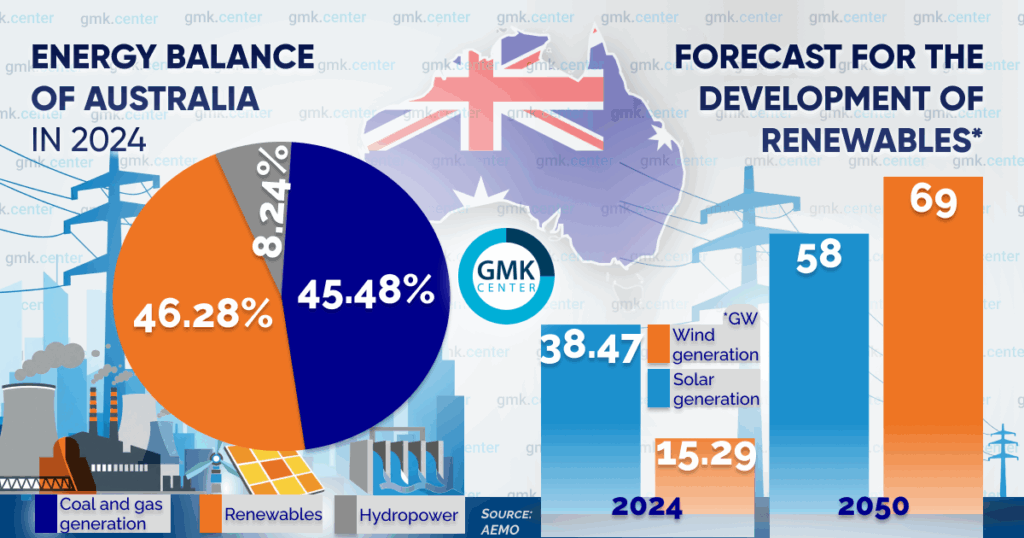

In Q4 2024, the share of coal and gas-fired generation fell below 50% of Australia’s total electricity generation for the first time. And by 2050, it should be completely replaced by renewable energy sources. It is planned to commission 32 GW of new green capacities by 2030. Their share will reach 82%.

Thus, in the near future the energy basis for decarbonization of the economy, including metallurgy, will be created. H2 production, DRI, iron and steel smelting in ESF and EAF – all these processes will be able to use 100% clean electricity.

But every issue has a price. In 2024, the wholesale cost of electricity in Australia will soar by 83%. The reasons: reduced availability of coal power in the context of high demand and grid constraints in electricity transmission.

Obviously, a further increase in the share of renewables in the energy mix will lead to even higher electricity prices. Both for household consumers and industrial consumers. Then, due to economies of scale, the cost of green electricity will start to decrease. But first everyone will have to survive the price shock. Therefore, the government has provided subsidies for the population in the amount of $300 per household. A total of $3.5 billion is allocated for this purpose in 2025-2027.

Business will not receive such direct support. However, the authorities will allocate $73 billion for the development of the energy sector. The funds are intended for laying new power grids and modernizing existing ones. This should remove the problem of grid limitations, increase the dispatch capacity of the energy system and the availability of electricity for industry.

In addition, the H2 industry will receive strong state support. According to the National Hydrogen Strategy, approved in July 2024, tax credits of $2000/t are provided to green H2 producers from 2027. This type of subsidy will remain in effect until 2040.

Given the current average cost of $5000/t for Australia, according to the Department of Energy, Environment and Climate Change, this is quite significant. Nevertheless, taking into account the consumption of 58 kg of H2 per 1 t of DRI, this product is 74% more expensive than conventional iron ore. The same economies of scale should reduce its cost.

By 2050. Australia plans to produce a minimum of 15 million tons of green H2 per year, and a maximum of 30 million tons. The first interim target is set for 2030. – 0.5 million tons, for 2035 – 1.5 million tons. The required electrolyzer capacity for 2030 is 3 GW and for 2050. – tentatively 150 GW.

By expanding production, the cost of H2 should fall to less than $1000/t by 2050. At these prices, exports to Japan and South Korea, which are planning significant hydrogen imports to decarbonize their economies, become feasible.

Also as part of the strategy, the federal government is providing $327 million through the Hydrogen Energy Development Fund to establish hydrogen hubs in New South Wales, Queensland, South Australia, Tasmania and Western Australia. Other existing initiatives that can be utilized by the meth companies include the following:

- The National Renewable Energy Fund (NRF) is allocating $1.96 billion to fund renewable energy and low-CO2 technologies. This category includes Liberty Steel and BlueScope decarbonization projects, as well as the GSWA project. An additional $650 million is being directed to value-added resources. This program is available to NeoSmelt and Fortescue;

- The Australian Renewable Energy Agency (ARENA) administers $197 million in programs to support the transition to renewable and low-emission technologies and energy efficiency;

- The Federal Government’s Green Iron Investment Fund, established in March 2025 as part of the Future Made in Australia plan, has received $1 billion in equity funding for decarbonization projects in the steel industry;

It is important to emphasize that these are not mere declarations of intent, but quite working initiatives. For example, Liberty Steel Australia was able to obtain $63.2 million from the federal government and $50 million from the state of South Australia to build the EAF in Wyalla. This is more than 20% of the project cost. The federal government announcement indicates that in total up to $500 million from the Green Iron Fund is being allocated to Liberty Steel. Apparently, the amount includes the H2-DRI plant project.

Thus, the Australian steel industry has all the prerequisites for successful decarbonization due to the huge resource potential in the field of RES and H2, as well as strong government support. However, additional measures will be required from the government in the form of tariff protection for the domestic market, similar to the European CBAM. Without them, the future of the industry is in doubt even after the completion of the green transition.

-

OpinionsGreen steelsteel consumption

13 July 2026

10 November 2025

16 October 2025

14 October 2025