Opinions Global Market MENA 10859 20 December 2022

Impact of Russian-Ukrainian war on global iron & steel trade flows

Disruptions in supply chain are not the main problem now. War worsens current economic situation globally

The first wave

The first wave of negative war effects includes supply disruptions due to idling steel plants in Ukraine. Majority of steel plants were stopped in the beginning of the war. In December only 2 steel plants work. Their capacities utilization does not exceed 30%. Such low utilization is explained by logistics and energy problems. Russian missile attacks significantly damaged energy infrastructure. It caused significant power outages. Electricity supplies are often interrupted. 5 out of 12 iron ore mining plants continue working now, because production of iron ore concentrate is energy intensive.

Logistics problems limit export geography. In the beginning of the war Russian fleet blocked Ukrainian seaports. It destroyed Ukrainian seaborne exports and MENA is the main suffered region. Local steel plants were significant consumers of Ukrainian iron ore, pig iron, semi-finished steel products. We assess that monthly exports losses for Ukraine reach $420 mln because of blocked seaports (1.3 mln tons of iron ore, 151 ths tons of pig iron, 192 ths tons of semi-finished products and 218 ths tons of finished steel products).

The first wave of war effects includes initial disruption in supply chains. Ukrainian steel plants stopped production and EU and USA faced with shortages. Pig iron supplies to USA were stopped for 3 months. Supplies to EU continue by railway, but volumes decreased. Average monthly supplies of Ukrainian pig iron went down by 87%. It became shock for European and American steel plants because they were traditional importers of Ukrainian pig iron.

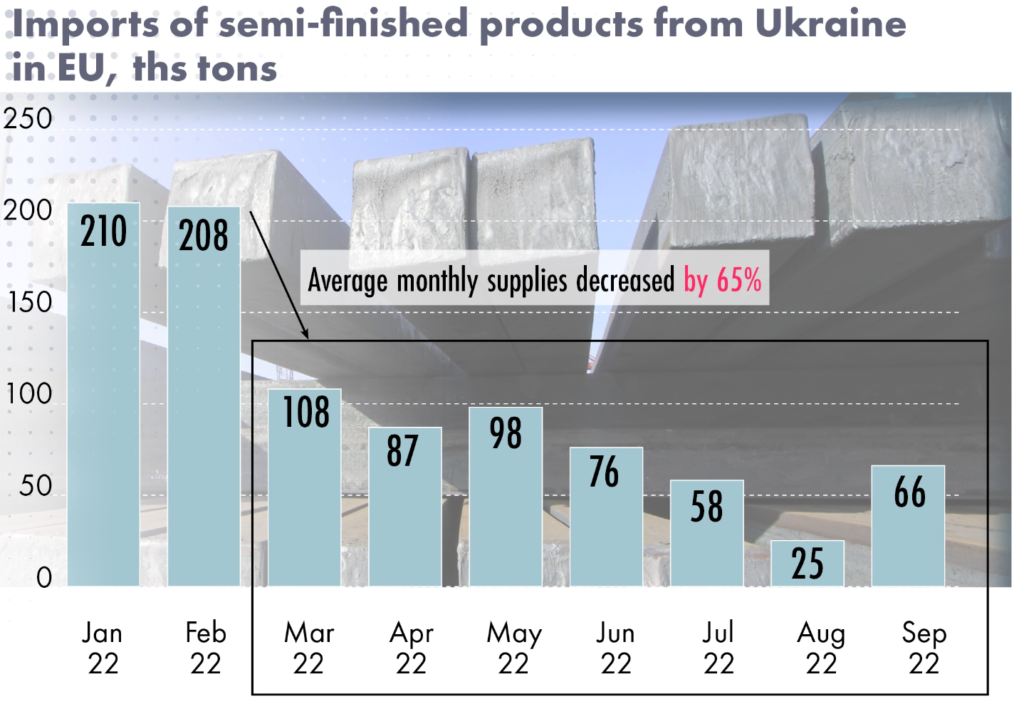

EU re-rolling plants also traditionally depend on import of semi-finished products from Ukraine. In 2021 imports from Ukraine satisfied 50% of square billet demand in EU. Ukrainian steelmakers met 35% of demand for slabs in EU. Average monthly supplies of steel semis to EU decreased by 65%. They cannot be recovered because two major Ukrainian steel plants were destroyed during the war.

Redirecting flow of Russian steel

The first wave of war effects also includes impact of sanctions against Russia and Russian companies, that changed directions of international trade flows.

The European Union banned the import of Russian finished steel products in the fourth package of sanctions. EU almost completely stopped imports of Russian finished steel products. Steel quotas for Russia were redistributed to other third countries. It influenced on global trade flows.

But instead, Russia increased pig iron exports to EU. Especially supplies from Russia raised in April-May when majority of Ukrainian steel plants did not work. In fact, Russia substituted pig iron imports from Ukraine. Iron ore and pig iron are not subjects of EU sanctions. So, Russia can use exports of these products as compensation for stopped supplies of finished steel.

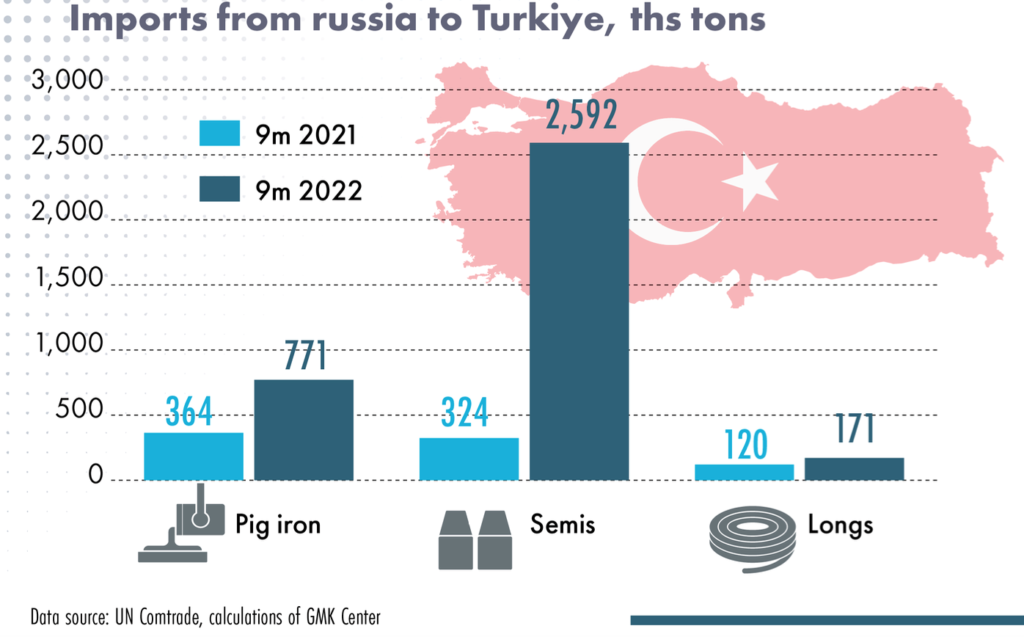

Without full access to EU market Russian steelmakers had to search for other export destinations. In fact, Russian suppliers broke steel market. Russian suppliers offered discounts (from 15% to 30%). Buyers were interested to get more steel products at lower prices. As a result, Russia increased exports to Turkiye and some CIS countries. In particularly, Turkiye increased imports of Russian steel semis 8 times. In its turn buyers of Russian products offer lower prices for their consumers. Russian supplies decreased steel prices to current low level. As a result, minimal losses for MENA rebar producers reach $70 mln per month.

The third wave

The war was the catalyst for the economic crisis in developed economies, that had realized “soft” monetary policy for a long period of time. The war increased energy prices and accelerated inflation. To curb inflation central banks had to raise interest rates. It hurts global economic growth. Everyone has already lost in this situation.

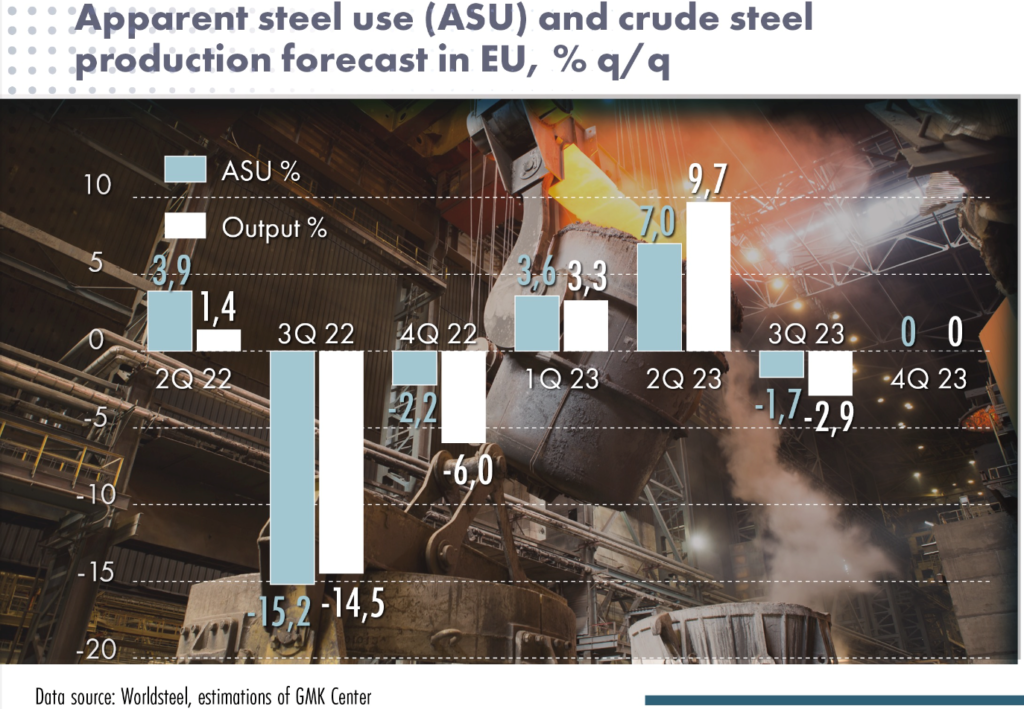

Economic crisis causes decreasing steel demand and redirection of trade flows. For example, Turkiye was traditional steel supplier for EU. Now Turkiye is becoming more active in MENA region. In 9 months 2022 India decreased steel exports to EU by 45% and increased steel exports to MENA by 16%. Low-cost steel suppliers like Russia, China, India decrease steel prices to expand exports. Raising exports mean negative margins for steelmakers.

We see that disruptions of supply chains are not the main problem now. Supply chains are adapted after initial disruptions. Producers found alternative suppliers. Decreasing steel demand also helped market to find balance. The economic situation in the EU has stabilized a bit. But it’s not the end.

Now the main risks are associated with a further escalation of the war in Ukraine. Nobody understands consequences of such situation. The war worsens current economic situation globally. The war can reveal additional disbalances, for example, in the real estate market in China and the EU, in the sovereign debt market. It is necessary to prevent further war escalation. This will mitigate the consequences of the second wave.

For mitigating the first wave Ukrainian sea ports should be unblocked. It will support Ukrainian economy and restore supply chains.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

02 July 2026

15 June 2026

07 April 2026