Opinions Global Market hot-rolled products 741 20 February 2026

Indonesia became a key player in the European hot-rolled coil market in Q4

Indonesian material, being the cheapest on the market, put pressure on prices in the EU

Indonesia emerged as a key player in the EU HRC market in Q4, grabbing a 26% share of imports.

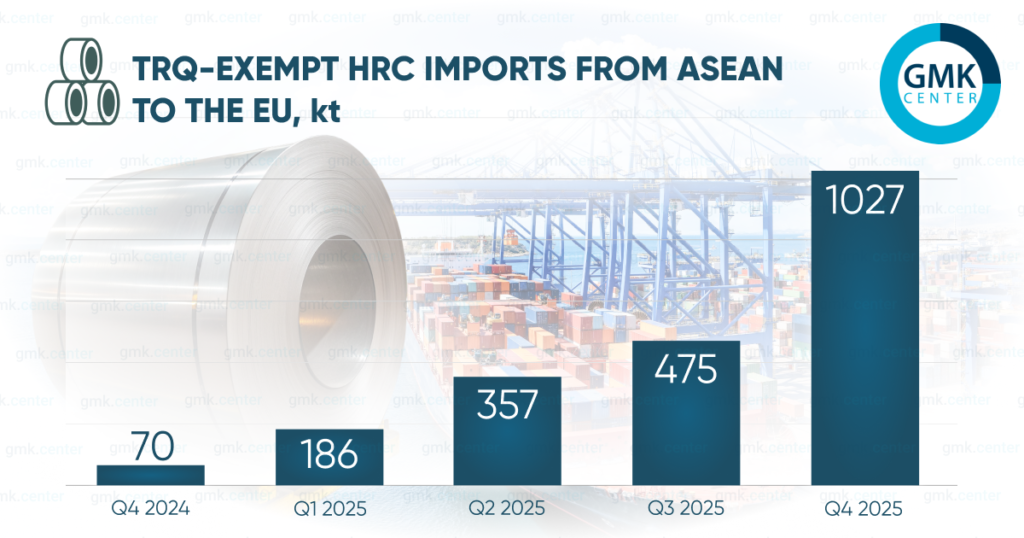

Combined, TRQ-exempt ASEAN suppliers (Indonesia and Malaysia) shipped 1.0 Mt to the bloc in the fourth quarter.

How did this happen? It is impossible to simply increase exports to Europe without consequences—this usually leads to trade restrictions. This has been observed many times over the past decade: as soon as one supplier gained momentum in the hot-rolled coil market, it was immediately restricted by anti-dumping measures. However, this opened the door for someone else, and the cycle repeated itself. This is now the fourth wave.

1st wave (2016–2017): Key HRC suppliers at the time, Brazil, Iran, Russia, and Ukraine, were hit with anti-dumping duties, giving Turkiye a competitive edge.

2nd wave (2020–2021): Turkiye itself became the target of anti-dumping measures. The outcome was more of a compromise, Turkiye remained a notable player.

3rd wave (2024–2025): Anti-dumping investigations targeted Asian suppliers Japan, Vietnam, and Egypt. India was also under review.

Parallel to the 3rd wave, the EU ramped up its TRQ system in 2025 to curb cheap imports amid China’s export push. Country-specific caps were introduced within the «other countries» quota category. That opened new opportunities for TRQ-exempt suppliers – first and foremost, Indonesia.

Indonesian-origin HRC accounted for one in every two tonnes imported into the EU in November 2025, and one in three tonnes in December 2025. Indonesia’s total HRC shipments in the Q4 were double those from Turkiye, which holds the largest individual country quota.

Being the cheapest option on the market, Indonesian material started putting pressure on other importers’ prices. That triggered renewed calls from EU steelmakers to tighten the screws.

Starting in July, import quotas will be cut by 42% compared to 2025 import levels. TRQ exemptions will be scrapped. That’s a serious blow for exporters heavily exposed to the EU. But will it stop Indonesian shipments? I don’t think so. Given current pricing dynamics in the ASEAN export market, Indonesian sellers can still absorb a 50% import duty, exceeding quota volumes.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

02 July 2026

15 June 2026

07 April 2026