Posts Global Market steel industry 791 26 March 2026

Weak domestic demand in Russia led to an increase in steel exports in 2025

The Russian steel industry experienced a significant decline in output in 2025. This situation was caused by the combined impact of Western sanctions, low global prices for steel products, and a decline in domestic demand. No reversal of this negative trend is expected in 2026.

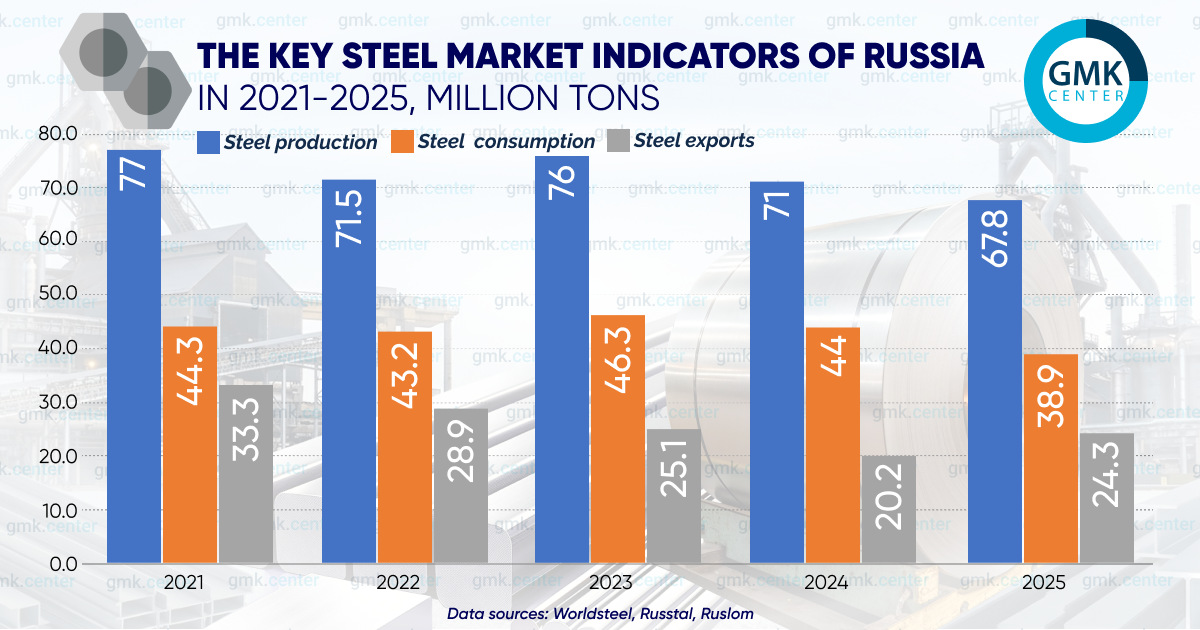

Russian steel market figures

The decline in the Russian steel industry has become entrenched. According to Worldsteel, steel production in Russia fell by 4.5% year-on-year last year, to 67.8 million tons. In 2024, the decline was 7% year-on-year.

According to Chermet Corporation, nearly all key production indicators last year showed negative trends:

- rolled steel – down 4.4% year-on-year, to 59.1 million tons;

- pig iron – by 1.4% year-on-year, to 50.3 million tons;

- tube products – by 19.5% year-on-year, to 10 million tons.

Iron ore production increased by 1.5% year-on-year, to 106.8 million tons.

According to estimates by the Russian Steel Association and Severstal, demand for rolled steel fell by nearly 14% year-on-year in 2025, to 38.9 million tons, following a 4% decline in 2024.

The export situation

Last year, exports became a lifeline for the Russian steel industry, and the dynamics of foreign shipments changed completely. According to estimates by the Ruslom Association, Russian steel exports grew by nearly 20% y/y – to 24.3 million tons. According to data from the Federal Customs Service of the Russian Federation, exports of metals and steel products in monetary terms in 2025 rose by 17.4% year-on-year, to $74.7 billion.

Russian steelmakers were partially aided by the abolition of export duties that were in effect in 2024 (ranging from 4% to 7% depending on the ruble exchange rate). In effect, Russian steelmakers began to offset the decline in domestic demand through foreign markets and maintained their capacity utilization rates.

In 2025, steel export logistics also showed positive dynamics. Rail exports increased by 11.1% year-on-year, to 24.8 million tons. The main cargo flow traditionally passed through ports—17.4 million tons. Southern ports shipped 11.5 million tons (+13.1% year-on-year), while ports in the country’s northwest shipped 4 million tons (+15.9% year-on-year); however, exports via the Far East fell by 14.8% year-on-year to 1.9 million tons. An additional 7.4 million tons of products were shipped for export via border crossings.

The decline in shipments via Far Eastern ports indicates a further drop in exports to countries in the Asia-Pacific region, primarily to China and South Korea. This reflects intensifying competition from local and Chinese manufacturers and weak demand for Russian semi-finished products in the region.

Domestic markets – CIS Countries

The CIS market is small and unable to compensate for the loss of Western markets in terms of either volume or margin. Among CIS countries, the main consumers of Russian steel products are Belarus and Kazakhstan.

There is no current data on Russian steel shipments to Belarus, but the approximate scale can be estimated based on 2021 data (after which Belarus stopped publishing statistics) — $1.3 billion (code 72). It is likely that this figure is currently no lower than the indicated level.

According to UN Comtrade data, exports of ferrous steel products (code 72) from Russia to Kazakhstan in 2024 grew by 9% year-on-year, reaching $1.5 billion. By year-end, Russian steel products held a dominant share in this market—83% of total imports. The main items of Russian steel exports to Kazakhstan in 2024 were steel semi-finished products (745,000 tons worth $411 million), rebar (535,000 tons worth $301 million), and hot-rolled steel (288,000 tons worth $185 million).

According to UN Comtrade data, steel shipments from Russia to other Asian countries belonging to the CIS are also quite significant:

- Uzbekistan – $920 million (-9% y/y) in 2024;

- Kyrgyzstan – $429 million (+43% y/y) in 2025;

- Azerbaijan – $209 million (-22% y/y) in 2025.

Georgia (which is not a member of the CIS) can be considered a partial domestic market for Russian steel; in 2024, it increased its imports from Russia under HS code 72 by 39% year-on-year, to $142 million.

It should be noted that some of the shipments to CIS countries and Georgia are transshipments and are actually re-exported to third countries, in particular to circumvent Western sanctions.

Turkey: a lifeline amid sanctions

Turkey remains the largest importer of steel products from Russia, a trend driven by short logistics routes, restrictions on shipments to the EU, and price dumping. According to Trademap, in 2025, Russian exports of ferrous steel products (code 72) to Turkey grew by 42% year-on-year and amounted to $3.3 billion. In particular, shipments of slabs to Turkey rose by 22% year-on-year – to 2.1 million tons, and square billets by 50% year-on-year – to 1 million tons. Russian exports of pig iron to Turkey last year increased by 83% year-on-year – to 1.8 million tons.

The significance of Russian steel raw material supplies to the Turkish market is evident from the share of imports from Russia in Turkey’s total imports in 2025:

- pig iron – 78% (in 2024, it was only 66%);

- slabs – 52% (42% in 2024);

- billets – 44% (only 12% in 2024).

Supplies made possible by price dumping make Turkish steel products more price-competitive. As a result, inexpensive steel from Turkey easily captures the Ukrainian market at the expense of local producers, accounting for over 60% of total steel imports into Ukraine. It was not until 2026 that Ukrainian producers began initiating anti-dumping investigations against rolled steel from Turkey.

This year, the situation for Turkish steelmakers could become significantly more difficult due to the European Union’s tightening of protective measures. This could lead to a reduction in Turkish steel exports to the European market by approximately 50–60%, given that up to 40% of all Turkish steel exports are destined for the EU.

Alternative market – Middle Eastern countries

Amid sanctions pressure, Middle Eastern countries have become a stable destination for steel exports from Russia. The countries in this macro-region have not joined the sanctions and are actively developing infrastructure, creating steady demand for steel products. On the other hand, there is fierce competition from products from China, Turkey, and other Asian manufacturers, and these countries also have their own steel production capacities.

The Middle East did not become an alternative export market after Russian steelmakers lost the European market. According to Trademap, in 2025, Russian exports of ferrous steel products (code 72) to Middle Eastern countries fell by 4.6% year-on-year to $3.3 billion, which is 44% less than in 2021 ($5.8 billion). The largest import categories to the macro-region last year were steel semi-finished products ($1.45 billion), cast iron ($638 million), and hot-rolled steel ($457 million).

The main importer of Russian steel in the export macro-region is Egypt: in 2024, shipments amounted to $967 million (+72% year-on-year). The largest import category was steel semi-finished products (486,000 tons worth $596 million). Other major consumers were Saudi Arabia ($62 million) and the UAE ($32 million).

This macro-region is characterized by instability — in recent years, hostilities of varying intensity have persisted in Israel, Yemen, Syria, Palestine, and Lebanon. This has led to Russian suppliers losing the Israeli market. Exports to this country effectively dropped to zero in 2024 after steel product exports totaled $741 million in 2023.

Following the escalation of the conflict surrounding Iran, instability in the Persian Gulf region has reached a new level. The prolonged continuation of hostilities in the Middle East poses a long-term threat to the economic development of most countries in the region and, consequently, to exports of steel products from Russia.

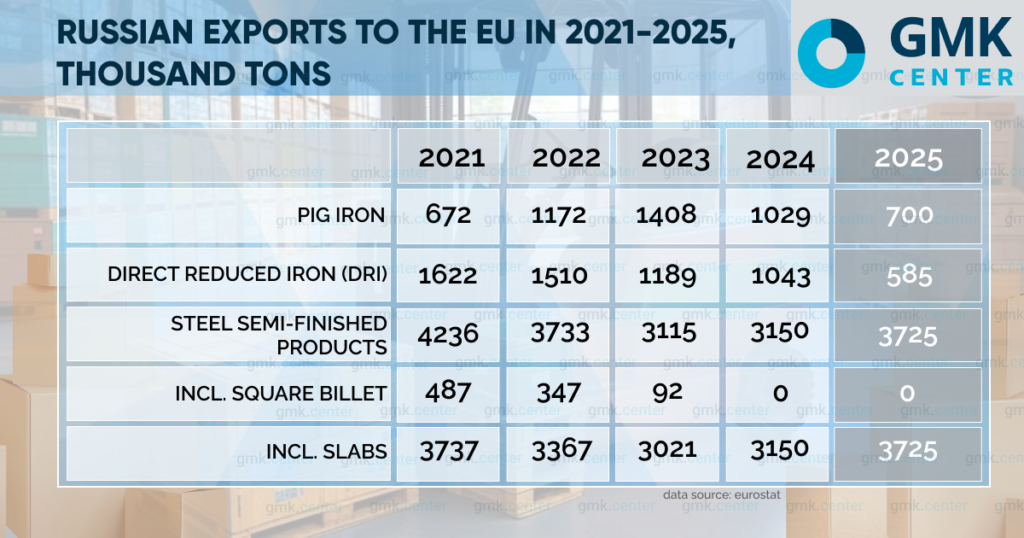

The EU is not turning away from Russian slabs

Currently, Russia supplies the European market primarily with steel semi-finished products. Last year, slab shipments increased by 18% to 3.73 million tons. The bulk of imports went to Belgium (1.3 million tons), Italy (837,000 tons), and the Czech Republic (826,000 tons).

Russian pig iron exports to the European Union fell by 32% year-on-year in 2025, to 700,000 tons. This figure represents the annual pig iron quota, which was effectively exhausted within two months of last year. The largest consumers of pig iron from Russia were Italy (525,000 tons), Latvia (87,200 tons), and Belgium (31,100 tons).

In 2025, direct reduced iron (DRI) shipments from Russia to the EU totaled 585,000 tons, a 44% decrease from the previous year. The largest importers of DRI were Italy (312,000 tons) and Belgium (135,000 tons).

A complete ban on imports of pig iron and DRI from Russia has been in effect since the beginning of 2026. This decision was established as early as in the 12th sanctions package (late 2023). At the same time, slab shipments from Russia will continue. The quota for Russian slabs until September 30, 2026, is 3 million tons, and for the following year (until September 30, 2027) – 2.62 million tons. Imports will cease only in October 2028.

The European Union’s continuation of Russian slab imports has drawn criticism from the German government, some Members of the European Parliament, European steel companies, and industry associations. Such imports undermine the competitiveness of a number of steel producers and harm the entire European steel industry, which is currently facing the most challenging period in its history. So far, there are no indications that Europe will abandon Russian semi-finished products ahead of schedule.

An additional long-term risk for Russian slab exports to the EU is the CBAM mechanism. In the long run, CBAM will gradually reduce the price competitiveness of Russian slabs even within the limits of current sanction quotas.

Conclusions on exports

In recent years, the domestic market has remained more profitable for Russian steelmakers than the export market; however, due to the deepening crisis in steel consumption, domestic market margins are shrinking. According to estimates by Euler, the domestic premium for rolled steel in Russia could decline by 27% in 2026—from $155 to $120 per ton. The highest risks of a premium decline are associated with rebar and long products, and to a lesser extent, pipe products.

Under the current circumstances, Russian steelmakers will be forced to increase exports. Russian exports will face the same challenges, including competition from cheap products from China and Southeast Asian countries.

A decline in demand from Middle Eastern countries could negatively impact steel exports from Russia in 2026. Given the stagnation of global steel consumption — with the exception of India — and the rise of protectionism, there is virtually nowhere left to redirect export flows.

In 2025, exports served as a buffer for Russian steel producers, preventing the industry from collapsing. The export structure remains vulnerable: Russia primarily supplies foreign markets with semi-finished products and raw materials with low added value (slabs, billets, pig iron) rather than finished rolled products. This limits the price premium and increases dependence on global steel market conditions.

Sanctions pressure from the European Union will intensify. Starting in October 2028, imports of Russian slabs will cease, depriving Russia of one of its main export channels, amounting to over 3 million tons per year. To compensate for the lost volumes, Russian exporters will become more active in the markets of Asia, Africa, and Latin America.

Forecasts and expectations

There is currently no basis for an optimistic forecast regarding an increase in domestic steel production in Russia, as indicated by production results for the first two months of 2026. According to data from Chermet Corporation, the decline in industry performance in January–February was as follows:

- steel production – down 9.9% year-on-year, to 10.3 million t;

- pig iron production – down 3.9% year-on-year, to 8.2 million t;

- rolled products output – down 8.3% year-on-year, to 8.9 million t;

- steel pipe production – down 35% year-on-year, to 1.2 million t;

- iron ore mining – down 8.9% year-on-year, to 16 million t.

Under these conditions, the decline in indicators by the end of 2026 could reach 3–5% y/y. According to Severstal’s forecast, consumption of steel products in the Russian market is expected to continue declining this year, with the rate of decline slowing to 3–4% y/y.

Given this situation in the domestic market, Russian steelmakers will continue their export expansion in 2026. Despite the challenges facing the global steel market, its participants should expect high activity from Russian exporters in global and regional markets.

-

OpinionsGlobal Marketmacroeconomics

28 May 2026

27 May 2026

20 May 2026

14 May 2026