The market needs new incentives for growth

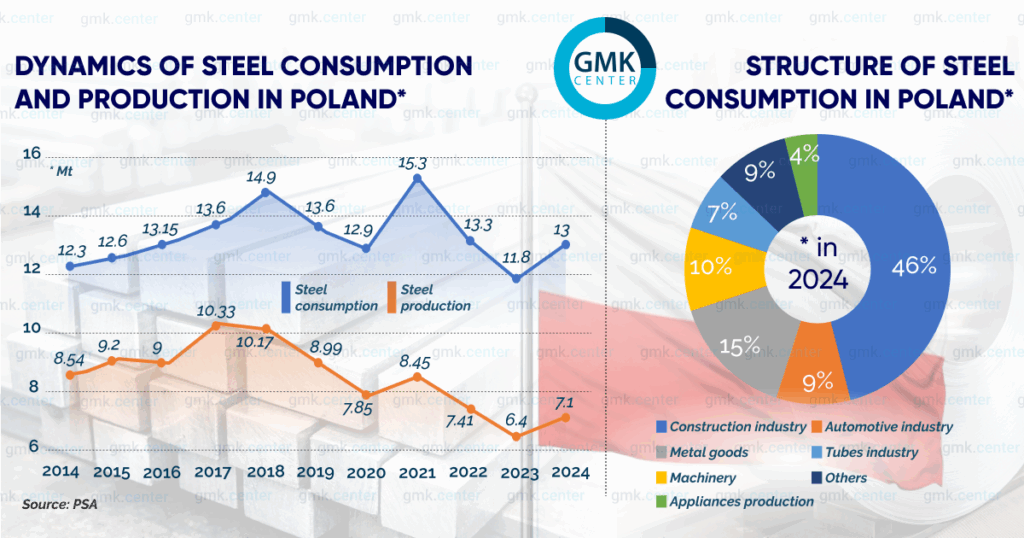

Demand for steel in Poland has remained within the range of 12–13 million tons over the past 10 years. The increase up to and including 2018 reflects the overall upturn in the Polish and European economies. This was followed by the consequences of the COVID-19 crisis and anti-crisis economic measures. Then came the adaptation to the energy crisis in Europe caused by the Russian-Ukrainian war. We can say that the main steel-consuming industries are resilient to external challenges. Do they have opportunities for further progress, or has the market reached saturation? GMK Center sought answers.

Market profile

Most steel sales in Poland are flat products (about two-thirds of the total). Sheet rolling and pipe production were the most affected by the crisis in the Polish steel industry. This refers to the closure and bankruptcy of the Huta Czestochowa steel plant, the Walcownia Rur Andrzej, Huta Pokój, Walcownia Blach Batory, Huta Krolewska, and Rurexpol steel mills.

According to the Polish Steel Association (PSA), in 2024, consumption of flat rolled products in Poland amounted to 7.4 million tons, and steel pipes – 1.2 million tons. The capacity of local producers in these segments is 2 million tons and 0.9 million tons, respectively. In the long products segment, consumption in 2024 amounted to 4.5 million tons, with domestic production capacity of 4.4 million tons.

The construction industry generates the main demand for steel in Poland. In 2024, it used 4.4 million tons of long products and 1.6 million tons of flat products. The second largest consumer is the hardware industry, with 2 million tonnes. The automotive industry rounds out the top three, with 1.2 million tonnes. An assessment of their current state will allow conclusions to be drawn about the immediate prospects for steel sales.

Construction industry

Polish housing construction is in a difficult situation. At the end of 2024, the housing stock across the country had expanded by 16.16 million m2. According to data from the Polish Statistical Office (GUS), between January and November 2025, the commissioning of new housing increased by 3% to 184,100 units. There are further indications of a significant decline. In the first 11 months of 2025, the number of building permits for new housing decreased by 11.4%, and the number of projects started decreased by 9.9%. In 2026, the sector is expected to experience a serious decline.

Industrial construction, including logistics facilities, is also under pressure. As of the end of March, projects with a total area of 1.4 million square meters were under construction (41% less than a year earlier). According to estimates by consulting firm Cushman & Wakefield, this is the lowest figure since 2018. The segment is highly concentrated, with 92% of all projects under construction located in the Mazovia and Łódź provinces.

The overall vacancy rate for warehouse and industrial space in Poland increased by 0.3% year-on-year to 8.5% in Q1. At the end of Q3, the figure fell to 8.2%, 0.2% higher than a year earlier. In Q1 2025, deals were concluded for the lease of 1.1 million m² of industrial space. This is 16% more than a year earlier, but 11% less than the average for Q1 in 2020–2024, which implies a lack of demand for new construction of such facilities.

The volume of space under construction increased slightly by October 1 to 1.56 million square meters, which is 20% less than on the same date in 2024. Cushman & Wakefield attributes 45% of this to speculative investments. These are projects under construction that currently have no end buyers/tenants, industrial and logistics companies. A deferred supply is forming, which will negatively affect construction volumes in 2026.

Government investment under the National Recovery Plan (KRO) remains the real driver. It includes road and railway construction programs. In 2025, 400 km of new roads were planned to be put into operation. These are bypass roads around cities and towns, involving the construction of a large number of bridge junctions and crossings – extremely steel-intensive structures.

In March last year, the government announced that it would allocate $2.8 billion to modernize 800 km of railways by 2027. Forty projects were approved for implementation. Most of them are related to the modernization of line 104, which is part of the North-South trans-European transport corridor.

In addition to national funding, these projects are also receiving money from European funds managed by the European Commission. The EU is giving Poland $9.22 billion to develop its railway industry in 2021–2027. Large-scale construction projects that generate demand for steel receive support not only from the national budget, but also from the European budget.

Other major programs include the Eastern Shield, which involves the construction of 800 km of fortifications on the border with Belarus and Russia by 2028. The Interreg NEXT Poland-Ukraine 2021–2027 project is aimed at developing transport infrastructure on the border with Ukraine. As part of this program, railway line 101 is being modernized in Poland.

Warsaw has an ambitious «green transition» program that envisages the phasing out of coal-fired power plants and the development of nuclear and offshore wind energy.

The country’s first nuclear power plant with a capacity of 1.1 GW will be built by the American-Japanese corporation Westinghouse Electric Co. in 2026–2030 in the coastal town of Lyubyatovo. The cost of the first phase of the project is $15 billion. In the future, it is planned to increase the capacity to 3.75 GW. The cost of the second phase is also estimated at $15 billion.

There are plans to build a second nuclear power plant, the location of which has yet to be determined. The project will be operated by a consortium led by the South Korean state-owned corporation Korea Hydro & Nuclear Power Co.

Wind energy in Poland is developing rapidly, supporting demand for steel structures. In 2020, the total capacity of wind farms was 6.27 GW, and by the beginning of 2025, it will reach 10.15 GW. By 2040, the government aims to increase this figure to 18 GW, primarily through the construction of offshore wind farms.

One of the most notable projects is the Baltic Power wind farm, construction of which began in 2025. The planned capacity of the facility will reach 1.2 GW. The total height of the steel structures of one wind turbine is 250 m, and 76 of them are planned to be installed. These are very steel-intensive facilities.

An even larger project is the Baltic Power 2 wind farm with a capacity of 1.5 GW. It is planned to be completed by the end of 2027. The wind farm will consist of 107 floating wind turbines. The project will cost $3.7 billion, of which $1.5 billion will be allocated by the government from the budget as part of the CRO. The remaining funds will be invested by the state-owned company PGE.

Automotive industry

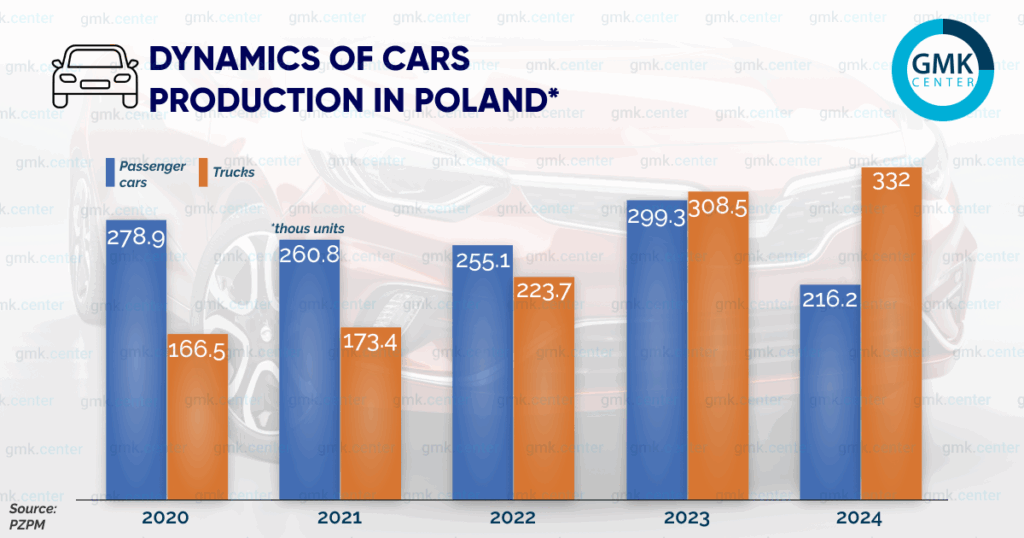

The Polish car market grew by 16.1% in 2024, with 551,568 new passenger cars registered. Car production fell by 28.7% – to 216,200 units. The increase in demand did not affect the capacity utilization of local car factories.

This problem is characteristic of the European automotive industry as a whole – weak tariff protection of the EU car market makes its products uncompetitive. Demand for sheet steel in these conditions was supported by an increase in the production of buses – by 38.8% to 7,113 units – and trucks and tractors – by 7.7% to 332,043 units.

The decline in passenger car production is partly due to a decrease in foreign sales. In 2024, Polish auto exports, including components, fell by 9.5% in monetary terms, to €45.5 billion.

The bulk of foreign sales by Polish car manufacturers is accounted for by components rather than finished cars. In 2023, finished cars accounted for only €7.19 billion of the total car exports of €50.3 billion. The volume of supplies here depends on the domestic situation in the automotive industry of other countries. The main destinations for Polish car exports are Italy and Germany.

In 2024, deliveries to Turkey, Egypt, and Morocco began for the first time. The new destinations will not be able to fully compensate for the decline in the main sales markets. Until the EU at the official Brussels level takes adequate measures to support the European automotive industry, Polish car exports will continue to decline, as will production volumes and demand for flat-rolled products.

Poland’s automotive industry continued to decline in 2025. From January to September, passenger car production totaled 75,500 units, with an average monthly output of 8,400 units. In 2024, Polish car factories produced an average of 18,000 units per month, in 2023 – 24,900 units, and in 2022 – 21,300 units.

The production of trucks and tractors decreased to approximately the 2023 level. In January-September 2025, the average monthly figure was 25,783 units, in 2024 it was 27,670 units, and in 2023 it was 25,705 units.

There has also been a decline in the average monthly production of buses, down to 510.5 units in January-September 2025, compared to 592.8 units in 2024, 427 units in 2023, and 421.7 units in 2022. This creates the conditions for a deterioration in the automotive industry’s final performance in 2025 and 2026.

The only sector of the engineering industry in which the Poles managed to achieve positive dynamics is the production of construction and road machinery. Here, in 2020-2024, the average annual increase in production was 8.59%.

Conclusions

- The increase in steel consumption to 15.3 million tonnes in 2021 demonstrates the potential of the Polish market, provided there is large-scale government support, primarily in the form of financing for infrastructure and energy development programmes. The dynamics in 2026 will depend on the implementation of the CRD.

- The most problematic area remains flat steel consumption, as there are no government incentives here, unlike in India and China. We are talking about tax breaks under the trade-in program for exchanging old cars for new ones.

- The application of the European CETA in 2026 will lead to an increase in the cost of foreign supplies for the Polish steel market, creating an additional financial burden on end consumers.