Posts Global Market emission quotas 2359 23 September 2025

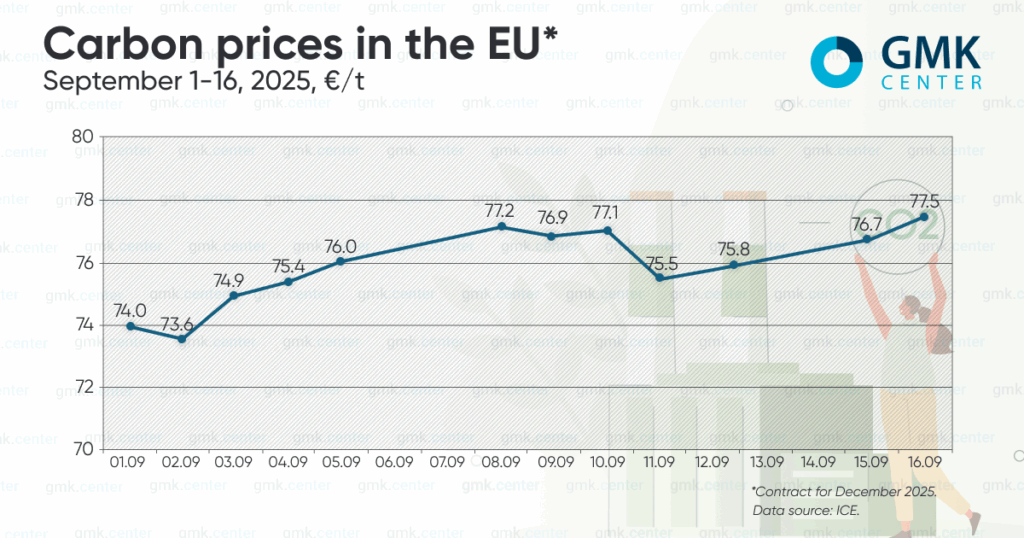

In two weeks of September, carbon prices rose above €77/t

In August, European carbon allowances were trading in a narrow range of €71-73/t (December contract), and mostly fluctuated depending on the gas price. However, in the first half of September (September 1-16), according to ICE, they rose by 5.3% to €77.5/t, as the market reacted to the behavior of traders who bought long-term contracts.

Growth points

The European carbon market is already preparing for next year. In addition to the final implementation of the Cross-Border Carbon Adjustment Mechanism (CBAM) in 2026, it will be affected by a number of other factors. These include a one-time adjustment to the annual emissions cap (a reduction of 27 million EUAs, equivalent to 27 million tons of CO2), a reduction in benchmarks for free allocation, and the end of the REPowerEU emissions trading program in August.

As for the CBAM, with its introduction, the volume of free allocation in the sectors covered by the mechanism will decrease, which will increase pressure on the market.

In 2026, the EC is planning to review the EU ETS and the Market Stability Reserve (MSR), and these issues are causing debate. In April this year, the EU executive body initiated a 12-week public consultation (until July 8).

As part of the consultation, German steelmaker Thyssenkrupp called for urgent changes in EU emissions trading to prevent the bloc’s industry from falling behind global competitors amid a slowdown in the green transition.

The German concern proposes a slower and more non-linear reduction of the allowance cap in the system until 2050, their more accurate correlation with the actual pace of industrial transformation and realistic levels of residual emissions. The company also proposes to extend free allocation beyond 2040.

The issue is being raised not only at the level of companies or unions, but also by governments. For example, Germany is seeking to ease EU emission reduction requirements for its industrial sectors due to higher energy costs. Minister of Economy Catherine Reiche warned of the risk of losing important sectors if the free distribution of CO2 emission quotas is terminated. According to her, it is necessary to quickly find a solution together with the European Commission.

At the same time, the Polish government is preparing a proposal to exclude the defense industry from the EU ETS, arguing that it will strengthen the security of the bloc’s member states. The Ministry of Climate and Environment has instructed the National Center for Emissions Balancing and Management (KOBiZE) to prepare an analysis of the potential impact of the initiative. The country intends to submit a legislative proposal to the EU. The government believes that it is necessary to take into account the specifics of arms production, which depends on energy-intensive raw materials, in particular steel.

CBAM transformation

On September 10, the European Parliament finally approved the CBAM simplification. The changes are part of the Omnibus I package presented by the European Commission in February this year.

In particular, a new minimum weight threshold of 50 tons of imports per year has been set, which will exempt 90% of importers (mainly small and medium-sized enterprises and individuals) from the CBAM carbon tax. At the same time, 99% of total carbon emissions from imports of iron, steel, aluminum, cement, and fertilizers will continue to be covered by the mechanism.

The rules for imports that remain under the CBAM have also been simplified. The start of the purchase of the relevant certificates has been postponed from January 2026 to February 2027 (covering emissions of goods imported in 2026). The reporting deadline has been extended from May 31 to October 31 of the following year.

In addition, importers will now be eligible to deduct carbon costs paid in any third country, not just the country of origin.

However, businesses still face uncertainty over key details that will allow importers to estimate the costs of CBAM. Appropriate technical legislation is needed to fully implement the mechanism.

In late August this year, the EU launched consultations on three key initiatives under the mechanism. These include the preparation of implementing acts that will define the rules for the final application of CBAM starting in 2026.

The consultations cover three areas: the methodology for calculating carbon emissions associated with the production of goods, the rules for taking into account free allowances in the EU ETS system, and the procedure for reducing the volume of CBAM certificates if the carbon price has already been paid for the products in third countries.

The deadline for submitting proposals is September 25 this year. Detailed implementing regulations based on these consultations are expected to be adopted by the end of this year.

Price forecast

Most experts predict an increase in the price of EUAs (greenhouse gas emission permits) in 2026 due to a decrease in supply and an increase in demand from new sectors such as shipping and air transport. Fluctuations in the cost of carbon will also depend on gas prices and industrial production. In addition, the gradual shift in the European energy balance away from fossil fuels, energy market reform, and emission reductions in this sector will result in industrial costs becoming the driver of carbon market pricing.

Thus, according to a quarterly Reuters poll of ten analysts, in July it was predicted that the average price of EU allowances in 2025 would be €75.15/t, in 2026 – €91.08/t, and in 2027 – €108.70/t. However, these expectations were lower than in April. All the experts surveyed expected carbon prices to rise in the coming years as the ETS reduces the limit on the amount of emissions that a sector or group of sectors can generate.

Brokerage firm Vertis recently raised its EUA price forecast for the current year by 10% to almost €78/t, and for 2026 to €110/t from €93/t previously, citing the completion of the REPowerEU allowance sale and the gradual withdrawal of free allocation, as well as increased emissions from maritime and air transport.

At the end of June, the Australian Macquarie Bank predicted the EUA price at €95/t in 2026. This is 5% higher than previous expectations. Analysts explain this by a reduction in supply. They estimate the volume of auctions next year at 475 million EUA (115 million less than in 2025), and free distribution at 447 million tons (-104 million by 2025). At the same time, the bank predicts a drop in demand in 2026 by only 32 million tons. At the same time, demand from the maritime and aviation sectors will increase by 27 million tons.

Next year will bring fundamental changes to the European carbon market. Its final configuration has not yet been determined – this is likely to happen in the second half of 2026. Nevertheless, experts advise market players to start long-term planning now amid the upcoming shortage of allowances and the need to implement emission reduction technologies.

-

11 June 2026

10 June 2026

27 May 2026

20 May 2026