Posts Global Market Slovakia 1113 13 February 2026

Slovak demand for steel has peaked under current market conditions

Slovakia has held the top spot in the world for many years in terms of car production per capita – 190-200 units. As a result, it is also among the top five countries in the European Union in terms of specific steel consumption. There is potential for further growth, but for a number of reasons, this is unlikely to happen in the foreseeable future.

Market profile

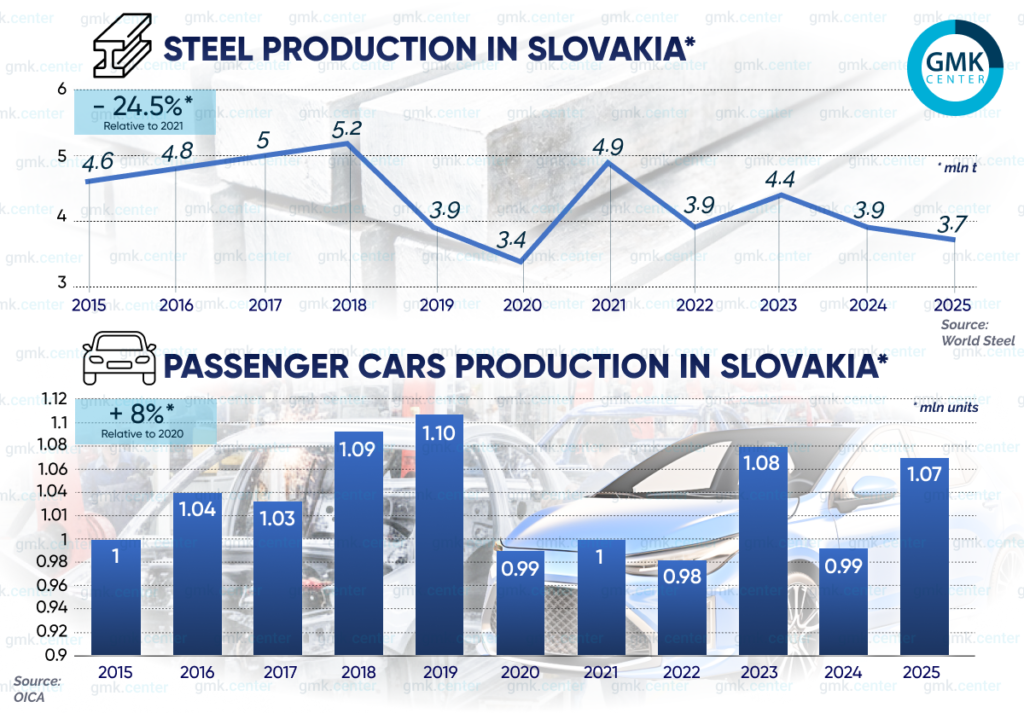

The main local player is the integrated Steel Kosice plant, a manufacturer of rolled sheet steel. In June 2025, the plant became the property of the Japanese corporation Nippon Steel, along with all other assets of the American US Steel. Things are not going well for Steel Kosice. In 2025, production fell by 5.1%, and by 25% over the last five years as a whole.

The situation is currently uncertain. The Japanese company is deciding which US Steel plants it will further strengthen and which it will weaken.

There is also the Max Aicher Slovakia Steel Mills electric steel plant in Strazske, owned by the small German group Max Aicher. This is a manufacturer of reinforcing and profile rolled products with an annual capacity of 620,000 tons, which has been idle since 2015. The local market’s demand for construction rolled products is fully met by imports.

The share of long rolled products in steel consumption is small for reasons discussed below. Most foreign supplies are sheet products. Demand for these products is driven by the automotive industry. From July 2024 to July 2025 inclusive, steel imports to Slovakia fell by 15.65% to 1.41 million tons, according to the Sinoimex platform. The main destinations were the Czech Republic, Germany, Poland, Italy, and Slovenia.

At the same time, demand remained stable, based on data on car production for this period. Therefore, we can assume an increase in the presence of local rolled products on the market. The overall decline in production at Steel Kosice is explained by a reduction in exports. From August 2024 to August 2025, it fell by 17.7% – to $2.407 billion.

There is no current information on the volume of the Slovak steel market. We can use data from the US International Trade Commission, according to which the figure was 2.7 million tons in 2016. That year, Slovak car production was at 1.04 million units, and in 2025, it was 1.07 million units. Thus, current steelconsumption is within the range of 2.7-2.8 million tons. Approximately 50% of this volume is accounted for by imports.

Demand for long-term rentals

Housing construction in Slovakia is at a minimum. In 2025, only 2,800 new apartments were sold, according to consulting firm Cushman & Wakefield. This is the highest result since 2021. At the same time, 3,874 new apartments were built in 99 residential complexes. In other words, supply significantly exceeds demand.

High mortgage rates, the main brake on the sector in European countries, do not play a major role in this case. According to the National Bank of Slovakia, in 2024, only 24% of real estate purchases were financed by mortgages. 34% were financed by personal funds. The rest were gifts and inheritances.

The main reason why almost no new housing is being built in Slovakia is the lack of demand for it. As of the end of 2023, 93.6% of all households lived in their own homes. For comparison, in Germany this figure is 47.6%.

The bulk of construction is focused on infrastructure. However, the government’s investment opportunities are limited, with European budget funds being the main source of financing.

One example is the 7.5 km long Višnévo car tunnel, the longest in the country. This is an extremely steel-intensive project, which was commissioned in December 2025. Its construction continued… since 2008. This is a fairly vivid illustration of Slovakia’s own capabilities in infrastructure development.

That is why the share of long products in total steel consumption is insignificant. For the same reasons, Max Aicher has not yet resumed production at its plant in Strazske.

Demand for flat-rolled steel

The automotive industry accounts for 52% of Slovakia’s total industrial production. It is the main consumer of flat-rolled steel. The industry is represented by Jaguar Land Rover in Nitra, PSA in Trnava, Kia Motors in Žilina, and Volkswagen in Bratislava. The COVID crisis forced them to slow down somewhat, but not too significantly. Thus, demand for flat-rolled products is characterized by stability.

In 2025, car production grew by 7.8%. At the same time, the Kia plant reported a 15% decline to 296,600 units. This is although production of the Kia EV4 started there in August. Usually, the launch of a new model allows for a significant increase in sales. This is an alarming signal for the industry. Since most of the cars produced are exported, it is linked to the downturn in foreign markets. First and foremost in Germany, the Czech Republic, Poland, and Austria – the main destinations for foreign sales.

Domestic demand cannot sustain production volumes. In 2025, Slovakia recorded only 93,060 new car registrations, 5.75% more than in 2024. The share of domestic sales was less than 10%. In neighboring Eastern European countries, where the automotive industry is also export-oriented, this figure is between 15-20%.

Market prospects

Demand for flat rolled products may increase, given that three car plants produced 1.04 million units in 2016. In 2018, Jaguar Land Rover joined them. However, its capacity is modest, at 150,000 units per year. In other words, the potential for growth is modest. And its implementation is highly questionable, according to Alexander Matushek, president of the Slovak Automobile Manufacturers Association (ZAP SR).

“We have results (for 2025 – ed.), but we are losing the conditions for further development. If this trend does not stop, the automotive industry in Slovakia will not disappear suddenly, but will gradually fade away,” he emphasizes.

According to the head of ZAP SR, the main reason is the authorities’ overly strict fiscal policy.

“The tax burden has already exceeded its maximum. The future of the industry is increasingly under threat due to the deterioration of conditions for business and investment,” he said.

This thesis is confirmed by the same Kia plant, which paid €226 million to the state in 2024. This is 4(!) times more than a year earlier. It is clear that the growth in tax payments does not correlate at all with production dynamics. Hence its deterioration as early as 2025.

It should also be noted that at the end of 2025, Slovakia ranked last in the list of the 36 most successful economies compiled by the British magazine The Economist. In the annual economic competitiveness ranking compiled by the World Bank, Slovakia ranks 63rd out of 69 countries.

In 2025, a record number of companies in Slovakia’s modern history closed down – 66,600, according to the local publication Finstat. Only 42,000 new companies were registered.

“This is apparently a reaction to legislative changes related to fiscal consolidation measures and an increase in the number of inspections by employment authorities,” the publication believes.

Based on this, Slovakia does not have the opportunity, like neighboring Hungary, to actively attract foreign investment to the country, including the construction of new industrial enterprises. This includes car factories. This means that demand for sheet steel will, at best, only be able to maintain last year’s volumes.

The development of wind energy will not be able to become a new driver, as there are no suitable natural and climatic conditions. The authorities have plans to build a third nuclear power plant, but they are still far from the practical stage.

In January 2026, Slovakia and the US signed an intergovernmental agreement on cooperation in nuclear energy. Local experts conclude from this that the construction will be entrusted to the Japanese-American corporation Westinghouse Electric Inc. However, no contract has been signed with it yet. Therefore, practical implementation is still a long way off.

The Slovak authorities have a large-scale infrastructure project in their portfolio – the construction of the Bratislava-Prague high-speed railway, jointly with the Czech Republic. However, it is only just getting started this year. As part of this project, a new railway station will be built in Stupava. And, remembering how many years it took to build the Vyshneve road tunnel, we can assume that this project will not have a significant impact on steel demand.

There are prerequisites for an increase in long product sales thanks to the revival of commercial construction. In the first half of 2025 alone, investment in this segment exceeded €500 million. This is more than for the whole of 2024, according to Europa Property. Logistics facilities are mainly being built. By the beginning of 2026, 311,000 m2 were under construction. The total area of existing warehouses is 4.6 million square meters.

Without an improvement in the business climate and government support for business, the economic situation in Slovakia will continue to deteriorate. This is already having a negative impact on the ability to attract investment. As a result, the local market is threatened with a serious decline.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

16 June 2026

10 June 2026

27 May 2026