Posts State Ukraine’s economy 2220 30 July 2025

In the first half of the year, industrial production and construction indicators have already entered negative territory, while GDP is still showing minimal growth

The growth rate of the Ukrainian economy began to gradually decline in the second quarter of last year. In the first half of 2025, certain macroeconomic indicators point not only to a halt in growth, but also to a transition to a stage of decline. Of course, this can be explained by the war and its numerous consequences.

However, virtually all previous sources of economic activity have been exhausted, and government economic support measures remain limited in scope and do not create new growth points. Moreover, tax and administrative pressure has increased significantly over the past year, and the tariffs of state monopolies are constantly rising, killing the last vestiges of Ukrainian business competitiveness.

Results for the first half of the year

The Ukrainian economy showed a clear decline in a number of key sectors in the first half of 2025. Thus, the real sector indicators in January-April were negative:

- Industrial production – -6.1% y/y (2024 – 3.6% y/y). The only areas of growth remain the defense industry and related sectors, as well as production focused on domestic consumer demand.

«Our industry is doing worse than we had previously assumed. The extractive industry is shrinking significantly because we lost the mines in Pokrovsk at the end of the year. Russia also dealt a very heavy blow to gas production,“ emphasized Oleksandra Betliy, a leading expert at the Institute for Economic Research and Policy Consulting (IER), at an online event entitled ”What awaits the economy in 2025 and beyond?», held by the Center for Economic Strategy.

- Construction – -13% y/y (2024 – 15.5% y/y). The largest decline was recorded in the construction of engineering infrastructure, which was a consequence of the termination of USAID funding for energy projects.

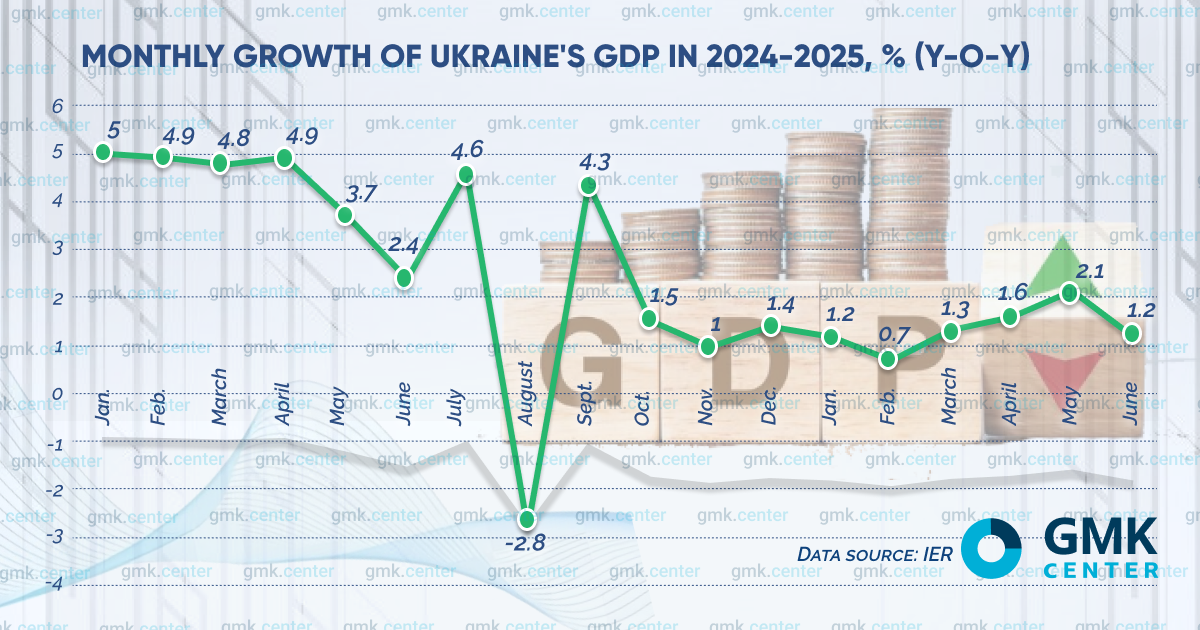

At the same time, the dynamics of Ukraine’s GDP so far show only a slowdown. According to preliminary estimates by the IER, in the first half of 2025, the economy grew by only 1.3% y/y. Despite the low dynamics, this figure even exceeds the growth rate in the first quarter (0.9% y/y), which was previously announced by the State Statistics Service. For comparison, throughout 2024, GDP grew by 2.9% y/y.

«As we can see from the first quarter, almost all sectors of the real economy are in the red. Only retail trade is driving growth, but even that is slowing down. The public administration sector is also driving growth, including sectors that depend on the budget. These are education and healthcare. It is unclear what factors, other than agriculture, could accelerate GDP growth,“ said Olexander Manuilov, an analyst at Forbes Ukraine’s analytics and research department, during the online event ”What awaits the economy in 2025 and beyond?»

Amid it, analysts are revising their forecasts for 2025. The National Bank has lowered its GDP growth expectations to 2.1% y/y from the previous 3.1% y/y. For its part, the consensus forecast (based on estimates from eight analytical centers) shows expectations of a slowdown in GDP growth this year, with a forecast range of 2-2.6% y/y and a median value of 2.3% y/y. It should be recalled that at the end of 2024, independent analysts expected the economy to grow by 3.7% y/y this year.

The NBU’s forecast already takes into account the triggers for the worsening economic problems in the country: a decline in harvests, the abolition of preferential access for Ukrainian agricultural products to the EU market (estimated losses of $700 million in 2024), and the intensification of hostilities and shelling of infrastructure. All this is expected to add to the existing negative factors: high electricity and gas prices, complications in foreign markets due to trade barriers, labor shortages and the high cost of credit resources, as well as uncertainty regarding the introduction of CBAM.

Economic outlook

The war remains the main factor influencing the prospects for the Ukrainian economy. Unlike at the beginning of this year, expectations regarding the duration of the active phase of hostilities have deteriorated significantly. Analysts who participated in the consensus forecast survey expect the war to continue until at least the end of 2025. Most are also pessimistic about 2026.

It is important to note that it is incorrect to attribute the deterioration of the economic situation solely to the war, as many variables depend on the actions or inaction of the authorities. In particular, the government’s work does not create new points of economic growth against the backdrop of the fact that the drivers of 2023-2024 have already been practically exhausted.

“Industrial policy in Ukraine remains fragmented and limited in terms of resources and instruments. This is not enough for significant structural changes in the economy,” Volodymyr Vlasyuk, director of the state-owned enterprise Ukrpromzovnishchexpertiza, said earlier in a comment to GMK Center.

Expectations for the new cabinet should also be very modest. First, all the new faces there are “old.” Second, experts believe that no significant breakthrough can be expected from the new government, even though it will receive more powers and a certain carte blanche.

Yulia Svyrydenko’s government introduced a one-year moratorium on inspections and restrictions on tax and customs inspections, planned an audit of criminal cases against businesses, deregulation, and a reduction in unnecessary permits. This is only part of what businesses expect from the new Cabinet of Ministers. At the same time, the government’s plans do not include other measures that businesses consider important and necessary:

Support for businesses in frontline regions, in particular through tax breaks, grants, and access to financing.

Further currency liberalization.

Development of tools for accessing business financing and insurance against military and political risks.

The NBU’s tight monetary policy continues to have a negative impact on the economy. Significant currency restrictions create problems for businesses in attracting capital, and the discount rate, which remains at 15.5%, makes affordable lending impossible.

“Although the regulator estimates that the decision will have a neutral impact on lending, maintaining a high real positive rate (with expected inflation of 9.7% at the end of this year) is unlikely to provide an additional boost to credit and economic activity,” said Danylo Getmantsev, chairman of the Verkhovna Rada Committee on Finance, Tax and Customs Policy.

In the near future, no improvements in the availability of lending are expected. According to Serhiy Nikolaychuk, deputy head of the NBU, the discount rate will remain at its current level until the fourth quarter of 2025, after which it is expected to gradually decline.

The tariffs of state monopolies continue to rise steadily, which is already causing production to slow down. It is unclear what factors, other than agriculture, could accelerate GDP growth,“ said Alexander Manuilov, an analyst at Forbes Ukraine’s analytics and research department, during the online event ”What awaits the economy in 2025 and beyond?»

Against this backdrop, analysts are revising their forecasts for 2025. The National Bank has lowered its GDP growth expectations to 2.1% y/y from the previous 3.1% y/y. For its part, the consensus forecast (based on estimates from eight analytical centers) shows expectations of a slowdown in GDP growth this year, with a forecast range of 2-2.6% y/y and a median value of 2.3% y/y. It should be recalled that at the end of 2024, independent analysts expected the economy to grow by 3.7% y/y this year.

The NBU’s forecast already takes into account the triggers for the worsening economic problems in the country: a decline in harvests, the abolition of preferential access for Ukrainian agricultural products to the EU market (estimated losses of $700 million in 2024), and the intensification of hostilities and shelling of infrastructure. All this is expected to add to the existing negative factors: high electricity and gas prices, complications in foreign markets due to trade barriers, labor shortages and the high cost of credit resources, as well as uncertainty regarding the introduction of CBAM.

Economic outlook

The war remains the main factor influencing the prospects for the Ukrainian economy. Unlike at the beginning of this year, expectations regarding the duration of the active phase of hostilities have deteriorated significantly. Analysts who participated in the consensus forecast survey expect the war to continue until at least the end of 2025. Most are also pessimistic about 2026.

It is important to note that it is incorrect to attribute the deterioration of the economic situation solely to the war, as many variables depend on the actions or inaction of the authorities. In particular, the government’s work does not create new points of economic growth against the backdrop of the fact that the drivers of 2023-2024 have already been practically exhausted.

“Industrial policy in Ukraine remains fragmented and limited in terms of resources and instruments. This is not enough for significant structural changes in the economy,” Volodymyr Vlasyuk, director of the state-owned enterprise Ukrpromzovnishchexpertiza, said earlier in a comment to GMK Center.

Expectations for the new cabinet should also be very modest. First, all the new faces there are “old.” Second, experts believe that no significant breakthrough can be expected from the new government, even though it will receive more powers and a certain carte blanche.

Yulia Svyrydenko’s government introduced a one-year moratorium on inspections and restrictions on tax and customs inspections, planned an audit of criminal cases against businesses, deregulation, and a reduction in unnecessary permits. This is only part of what businesses expect from the new Cabinet of Ministers. At the same time, the government’s plans do not include other measures that businesses consider important and necessary:

- Support for businesses in frontline regions, in particular through tax breaks, grants, and access to financing.

- Further currency liberalization.

- Development of tools for accessing business financing and insurance against military and political risks.

The NBU’s tight monetary policy continues to have a negative impact on the economy. Significant currency restrictions create problems for businesses in attracting capital, and the discount rate, which remains at 15.5%, makes affordable lending impossible.

“Although the regulator estimates that the decision will have a neutral impact on lending, maintaining a high real positive rate (with expected inflation of 9.7% at the end of this year) is unlikely to provide an additional boost to credit and economic activity,” said Danylo Getmantsev, chairman of the Verkhovna Rada Committee on Finance, Tax and Customs Policy.

In the near future, no improvements in the availability of lending are expected. According to Serhiy Nikolaychuk, deputy head of the NBU, the discount rate will remain at its current level until the fourth quarter of 2025, after which it is expected to gradually decline.

The tariffs of state monopolies continue to rise steadily, which is already causing production to slow down. On July 31, the National Energy and Utilities Regulatory Commission (NEURC) increased the maximum permitted level of electricity prices (price caps) for industrial consumers during evening peak hours by 1.67 times. Higher business costs for electricity will further increase pressure on production costs, which may lead to higher prices for goods and services.

A separate issue is the non-reimbursement of VAT – business debts have long exceeded UAH 30 billion. Exporting companies are heavily dependent on VAT refunds, as this is part of their working capital, which is always in short supply in wartime. At the same time, businesses cannot count on loan financing – bank loans are expensive, and the possibilities for raising funds on Western capital markets are extremely limited. This problem has recently affected iron and steel companies in particular, especially the largest mining companies.

By the end of the year, the trade deficit situation may become significantly more complicated. In the first half of the year, we saw a significant increase in imports (15.4% y/y), which significantly outpaced export growth (2.6% y/y). The negative balance of foreign trade in goods for January-June amounted to $18.3 billion, which is 47.5% more than in the same period last year.

If the current dynamics continue, Ukraine risks significantly exceeding the negative record of 2024 – $29 billion. For comparison: in 2022, the negative balance amounted to only $11.1 billion. This means the “washing out” of currency from the country, increased pressure on the hryvnia, and a deterioration in the financial and economic situation for domestic producers.

The issue of deferral from the CBAM, which will be introduced at the beginning of 2026, is very important for basic industries. This quasi-tax means additional payments from the metallurgy, cement, energy, and other industries. According to GMK Center estimates, the potential additional export losses from the introduction of CBAM will amount to $372 million in 2026 and a total of $1.75 billion by the end of 2030. But in fact, the introduction of CBAM will begin to negatively affect Ukrainian export volumes as early as this fall. Potential losses in tax revenues to the state budget next year will amount to $266 million, and by the end of 2030, a total of $1.35 billion.

Instead of a conclusion

No one knows when and under what conditions the war will end. Its consequences for our country are not predetermined. The country’s ability to defend itself largely depends on the functioning of the economy – the rear. In turn, the functioning of the rear largely depends on the speed and nature of the government’s management decisions.

It is quite likely that as a result of the war, the country will be left with an industry that has been depleted and destroyed by the war. But it may also end up with an industry that has been hardened by the war and adapted to rapid change. The outcome depends not only on the external environment, but also on the decisions made by the authorities.

That is why now is the best time to change the approach to economic management. Ukrainian business needs greater and more systematic support, above all, access to “long-term” and cheap money. This will allow one of the goals of the new Cabinet of Ministers to be achieved – to increase the share of the processing industry in GDP from 8% to 20% in 10-15 years.

That is why Yulia Svyrydenko’s new government must ensure the necessary decisions aimed at developing the Ukrainian economy:

- economic support must become more systematic and large-scale in order to create new drivers of growth;

- a significant reduction in tax and administrative pressure;

- implementation of an adequate monetary policy for wartime conditions;

- freezing of state monopoly tariffs;

- ensuring the availability of credit and easing currency restrictions;

- launching effective insurance of military risks to attract investment.

All this will make it possible to flexibly and effectively stimulate economic development, improve conditions for business, and increase domestic production of defense products, thereby maintaining a sufficient level of defense capability. However, if the necessary management decisions are not made, the decline of the Ukrainian economy will deepen and defense capabilities will diminish.