Posts Industry green steel 3168 08 October 2025

Steel producers are suspending projects and postponing deadlines, citing market conditions and regulatory uncertainty

Major steel companies are postponing their green transformation plans, seeking greater certainty, particularly regarding the bloc’s steps to protect the industry and the market.

Status: postponed

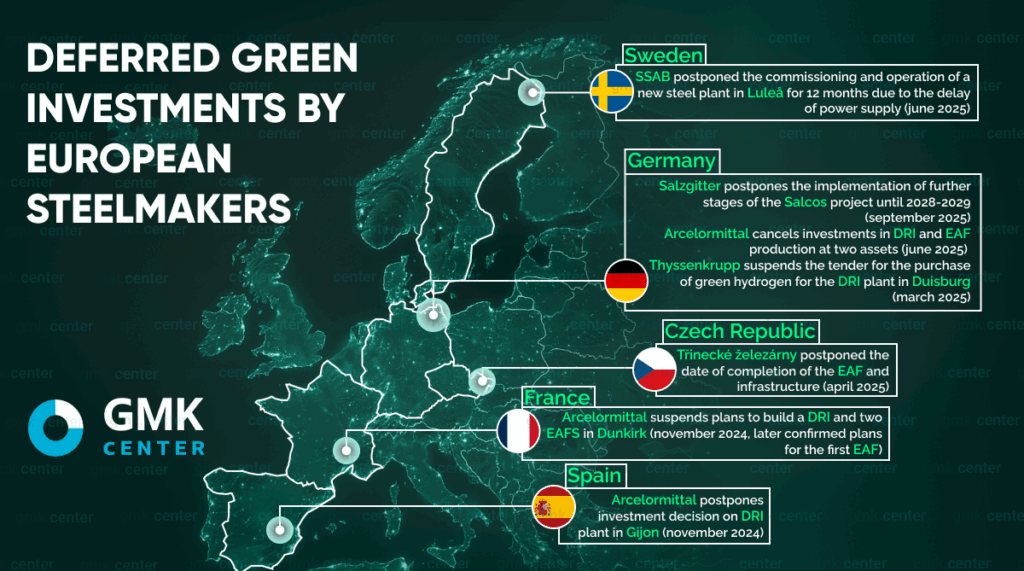

In September this year, German steel producer Salzgitter announced its decision to postpone the next stages of its large-scale green project Salcos, which aims to reduce CO2 emissions in steel production through the use of hydrogen, for three years. The company justified its decision by citing slower-than-expected development of the hydrogen market and the lack of regulatory changes promised by the government.

The total cost of the Salcos project is around €2.5 billion (€1 billion in state support). Its first phase is already underway. It involves the launch of a 100 MW electrolyzer, the construction of a direct reduction plant, and an electric arc furnace. However, Salzgitter has postponed the next stages until at least 2028-2029, whereas the investment decision was previously planned for 2026.

Salzgitter is not the first large company to put its plans for decarbonizing steel production on hold.

In June 2025, ArcelorMittal canceled the EAF-DRI project aimed at decarbonizing its plants in Bremen and Eisenhüttenstadt. The agreement with the German government included €1.3 billion in state aid and required construction to begin by June this year. When announcing its decision, ArcelorMittal pointed to market conditions and the lack of economic viability for green steel production.

Back in November 2024, the company decided to delay its green investment plans in Europe, citing high energy costs along with political and market uncertainty. The projects on hold included a €1 billion DRI plant for the Gijón cluster in Spain—€450 million of which was supposed to come from government funding—and the decarbonization efforts at its Dunkirk site in France.

In particular, a direct iron reduction plant with a capacity of 2.5 million tons per year and two EAFs were to be built in Dunkirk. However, later, in May 2025, ArcelorMittal confirmed plans to invest in the first electric arc furnace at this site (cost – €1.2 billion). The company expressed confidence that by the end of the year, all conditions would be in place to resume the decarbonization plan.

Unavailable hydrogen

At the end of March 2025, Germany’s largest steel producer, Thyssenkrupp AG, postponed indefinitely a tender for green hydrogen for its H2 DRI plant in Duisburg (2.5 million tons/year), which had been announced in February 2024. As the company noted, the proposed price was much higher than expected, and the hydrogen sector is developing slowly.

After ArcelorMittal’s decision to cancel its German project, Thyssenkrupp reaffirmed in June that it would move forward with building a green steel plant in Duisburg (the project is expected to cost €3.5 billion). However, the company noted that the success of the green transformation is possible under economically viable conditions, accessible hydrogen infrastructure, and competitive (affordable) energy prices.

The need for state support

Třinecké železárny Group, the largest steel producer in the Czech Republic, announced at the end of April 2025 that it was postponing the completion date of the largest investment in the plant’s history related to the decarbonization process. The company will complete the construction of the EAF and necessary infrastructure no earlier than 2030 instead of the announced 2028. Until then, active negotiations will be held with the Czech government and the EU to ensure adequate support for the project. According to public sources, it is unlikely that the project will receive state support.

Italy, meanwhile, is discussing fantastic projects for Acciaierie d’Italia (ADI) in Taranto. There are plans to build three EAFs (total capacity – 6 million tons/year). However, the search for a new owner of the assets is not yet over and is likely to end in disaster. Therefore, these decarbonization plans are also unrealistic and are being postponed.

The beginning of the journey

However, there is some good news. At the end of September 2025, Tata Steel finally signed a non-binding letter of intent with the Dutch government to reduce emissions. At its IJmuiden site, the company aims, among other things, to decommission blast furnace No. 7, build a direct iron reduction plant that will initially run on natural gas, and build electric arc furnaces with increased scrap consumption.

The Dutch government has agreed to allocate €2 billion to support Tata Steel Netherlands’ (TSN) decarbonization project. In addition, TSN has applied to the EU Innovation Fund for €0.3 billion.

However, the parties will continue to work on a binding agreement in the coming months, particularly after the elections and the formation of a new government. During the process of concluding the agreement, Tata Steel’s board of directors will consider the final investment decision. The decarbonization plan for the Dutch plant, presented in 2023, is scheduled to run until 2029.

In September 2025, Sweden’s SAAB announced the official start of construction of its new “green” steel plant in Luleå (cost: €4.5 billion). It will replace the current BF-BOF-based production and will have an annual capacity of 2.5 million tons. The plant will be equipped with two EAFs, an advanced secondary metallurgy system, an integrated hot rolling mill, and a cold rolling complex.

The start of operation was announced for the end of 2029, but in June 2025, the company postponed it by 12 months. The reason was that the power grid reinforcement for the new plant will not be completed as planned.

At the same time, Swedish startup Stegra is looking for alternative financing options after being denied a previously approved grant through the Climate Leap fund. According to the company, the reason for the refusal is that its activities will generate certain emissions when using gas, which is necessary until there are sufficient substitutes. Therefore, the company is reviewing its financing plans.

Stegra is building a large-scale plant for the production of environmentally friendly steel in Boden. It will consist of an electrolyzer, a direct reduction plant, two electric arc furnaces, as well as cold rolling and finishing shops. Production is expected to start here in the second half of 2026, with the plant reaching full capacity in 2028.

In September this year, Voestalpine launched Austria’s largest climate project. Construction has begun in Linz on Hy4Smelt, the world’s first industrial-scale demonstration steel plant that will combine hydrogen direct reduction technology with an electric arc furnace. The project is being implemented at voestalpine’s facilities in cooperation with Primetals Technologies and Rio Tinto. Production is scheduled to start at the end of 2027, with the program due to be completed in 2030. The project is partly funded by Austrian and European institutions.

Plans and realities

When reviewing their decarbonization plans, companies cite the weak steel market, high energy prices, and slower-than-expected development of hydrogen infrastructure.

Important issues for steelmakers remain the format of new EU protective measures (the current ones expire in July 2026) and the carbon border adjustment mechanism (CBAM), which will be fully implemented from the beginning of next year. In addition, uncertainty remains regarding the green steel market itself.

Even with government support for green projects, steelmakers emphasize that they are unable to cover the costs of transitioning to low-carbon technologies on their own.

«Let’s be honest and frank. The days of green steel ‘hysteria’ are coming to an end. The time has come for technological, investment, and government decisions. The industry needs affordable smart technologies (not hydrogen myths), the industry needs investment, and the industry needs a long-term, clear government policy. It is impossible to rebuild a large sector in 3-5 years based on unavailable hydrogen and “green” premiums. Different companies will produce green steel in different ways in different countries — some based on scrap, some based on hydrogen, relying on the competitive advantages of individual states and regions,» concludes Stanislav Zinchenko, CEO of GMK Center.