Posts Global Market economy 13878 08 May 2024

High lending rates and weak demand are dragging down the EU's largest economy

The German economy – the largest in the European Union with a GDP of about €4.5 trillion by 2023 – has turned from a locomotive into a brake on the European economy. Further dynamics largely depends on the inflation rate and the ECB’s monetary policy.

Stagnation or recession?

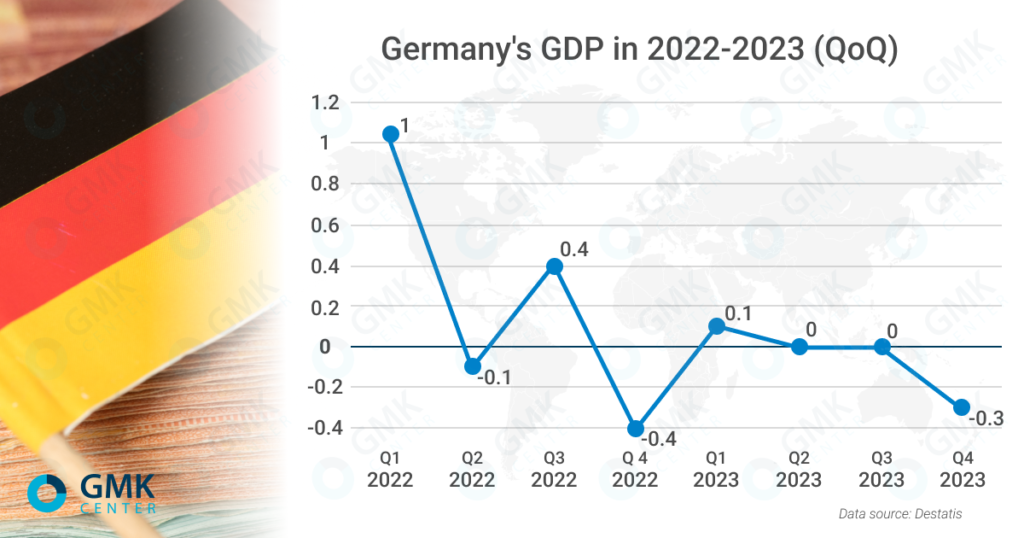

At the end of last year, Germany showed the worst result among developed countries – GDP fell by 0.3% y/y. The previous fall was in 2020 – by 3.8% y/y. And before that the decline was during the global financial crisis in 2009 (-4.7% y/y).

In the second half of 2023, Germany miraculously avoided recession (two quarters of decline). In Q4 GDP decline amounted to 0.3% q/q, and the preliminary result in Q2 (- 0.1% q/q) was revised upward to 0%.

The slowdown in global economic activity had a negative impact on foreign trade: German exports in 2023 fell by 1.4% – to €1.56 trillion and imports – by 9.7%, to €1.35 trillion.

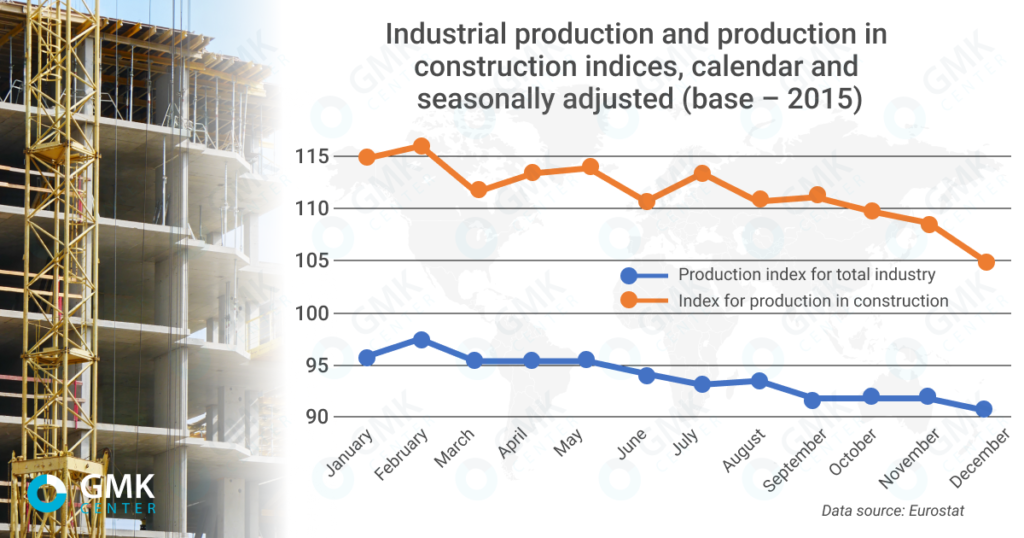

Industrial production in Germany contracted by 2% y/y last year due to declines in the energy, chemicals and steel sectors. In general, the manufacturing industry sagged by 0.4% y/y. In turn, the service sector showed growth of 1.8% y/y, but it was weaker than in 2021-2022 and could not compensate for the overall decline in GDP.

The construction sector recorded a 0.2% y/y growth due to infrastructure and completion of already started projects. Housing construction, on the contrary, is suffering from a drop in demand due to high mortgage rates and rising costs. A continued downturn in residential construction could have negative consequences for the entire economy. The German construction industry expects a 3.5% y/y decline in revenue in 2024, following a 5% y/y decline in 2023.

Due to unfavorable business conditions, German companies have started to think about relocating their production facilities to other countries. The survey of the German Chamber of Commerce and Industry (DIHK) showed that one third of respondents (sample – more than 27 thousand companies) plan to reduce investments in the country in the next 12 months, including preferring to invest in development abroad.

The main beneficiary of this situation is the US, which introduces preferences for technological industries. In 2022, the US passed the Inflation Reduction Act, providing tax breaks and subsidies worth $370 billion to finance, in particular, the production of batteries and electric cars. Thus, the US began competing with its allies for climate investments.

This immediately changed the dynamics of the investment flow. According to fDi Markets, last year German companies announced investments in the U.S. in the amount of $15.7 billion amid $8.2 billion in 2022. Such car giants as Volkswagen, BMW and Porsche, which explicitly refused in favor of the U.S. from the construction of battery production in Germany, want to locate their plants there.

At the same time, major German companies are also expanding their presence in China. Chemical giant BASF is investing €10 billion in production in China, while at the same time reducing its capacity in Germany due to high gas prices. German direct investments in China in 2023 reached a historic high of €12 billion. According to fDi Markets, the size of German projects announced last year in China amounted to $5.9 billion.

Factors affecting the state of the German economy

Shortly after the outbreak of the war in Ukraine, the German authorities announced the refusal to import Russian energy resources. At the same time, the country was highly dependent on their supplies. Before the war, the share of Russian gas in the German market amounted to 55% of all imports, coal – 50%, oil – 35%. Because of this dependence, it was Germany that suffered the most from the energy crisis of all European economies.

Through austerity measures and the shutdown of a number of industrial production facilities, by the beginning of 2023 Germany managed to stop using Russian gas, oil and coal, diversify its supply sources and reduce consumption. This significantly improved the overall situation in all segments of the country’s energy sector.

In 2023, the energy crisis passed and energy prices decreased. In particular, the level of gas prices has roughly tripled in 2023: the average day-ahead price level in 2023 was €41/MWh, compared to €127.1/MWh in 2022. Electricity prices last year in Germany fell to 2021 levels: according to BNA, the average wholesale price last year was €95.2/MWh, compared to €235.4/MWh in 2022. At the same time, electricity output in 2023 fell by 9.1% y/y. Last year, for the first time, Germany became a net importer of electricity: imports rose 63% to 54.1 TWh, while exports fell 24.7% – to 42.4 TWh.

Despite the fight against inflation, it still remains at high levels and is hampering economic activity. According to Destatis, the inflation rate (CPI) in 2023 was 5.9% y/y, while the harmonized inflation rate (HICP) was 6% y/y. In 2023, goods rose in price by 7.3% y/y, services – by 4.4% y/y, energy prices rose by 5.3% after a sharp increase of 29.7% in 2022.

To combat high inflation, the European Central Bank (ECB) raised its benchmark lending rate from 0% per annum to the current 4.5% from June 2022 in 14 cycles. This has helped to slow consumer price growth but has had a negative impact on the econ. Inflation in the eurozone in March 2024 was 2.4% annualized (the target is 2%), meaning high interest rates will continue for some time to come.

The German economy is export-oriented and in particular depends on trade with China, which is its largest trading partner. However, economic growth in China is slowing down. Moreover, the Chinese authorities are focusing on the development of their own machine building industry, so the prospects for exports to China are worsening.

The situation in steel industry

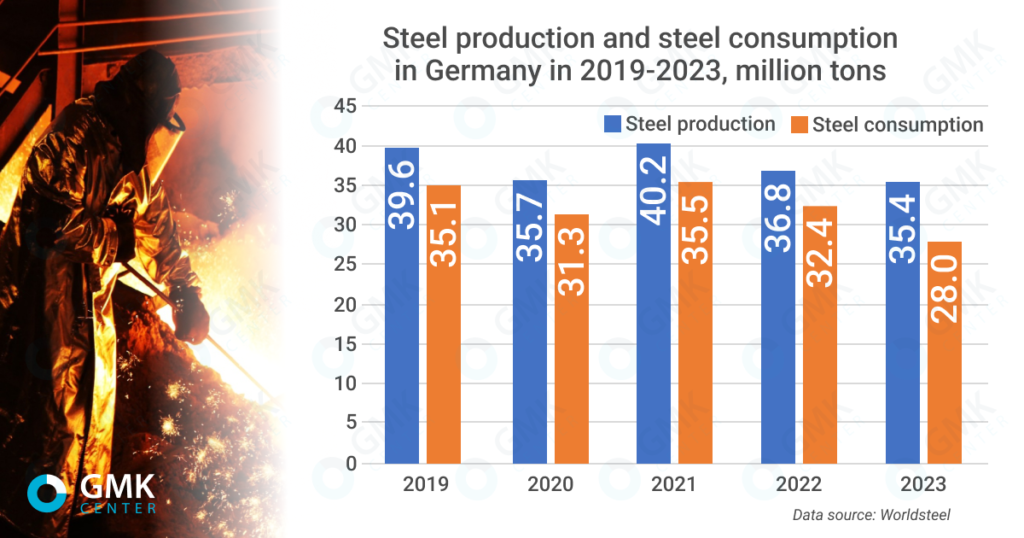

The situation in the German steel industry is a reflection of the general economic situation in the country – for the second year in a row, the industry is in decline. According to the Worldsteel Association, in 2023 German steelmakers will reduce steel production by 3.9% y/y – to 35.4 mln tons, in 2022 – by 8.4% y/y, to 35.4 mln tons. In 2022 – by 8.4% y/y, to 36.8 million tons. In 2023, steelmaking turned out to be the lowest since the financial crisis of 2009. However, this did not prevent Germany from retaining the 7th place in the world ranking of steel producers for two years in a row.

The decline in steel production in Germany in 2022-2023 is due to both negative macroeconomic factors and high energy prices, weak demand and growth in steel imports from Asia. The industry has responded to the deteriorating situation by closing capacity.

For example, French producer Vallourec closed seamless pipe production at two plants in Germany.

Other indicators of the German steel market also declined last year:

- exports – by 7.8% year-on-year, to 3.36 million tons;

- imports – by 31.9% year-on-year, to 760 thousand tons.

The problems of the German steel industry can be seen in the example of the industrial group ThyssenKrupp, which since the beginning of last year with renewed vigor began looking for opportunities to sell its steel division. Since the summer 2023, negotiations have been underway about the possible sale of up to 50% of this business to the Czech holding company EPCG. At the moment the parties have reached an agreement on the sale of 20% of shares in Thyssenkrupp Steel Europe with the prospect of increasing the stake to 50%. In any case, ThyssenKrupp already plans to reduce steelmaking capacity by 1.5-2 million tons – to 9-9.5 million tons per year. Earlier, the company closed the Galmed plant in Spain, which specialized in the production of galvanized rolled products for the automotive industry.

A slight improvement in the situation with production and demand can be expected this year. According to the results of January-February, Germany has already increased steelmaking by 4.6% y/y – up to 6.2 million tons. In turn, Worldsteel forecasts growth of steel consumption in Germany in 2024 by 3.2% y/y – to 28.9 mln tons after the decline in steel production after falling in 2023 by 13.7% y/y. (to 28 million tons). However, this is significantly worse than forecast back in fall-2023, when growth expectations were for 10.6% y/y – to 32.3 million tons. Worldsteel expects higher steel demand growth in Germany in 2025, up 10% – to 31.8 million tons. German steel association WV Stahl also forecasts an improvement in demand only in 2025.

«We view the crisis in the German economy as cyclical. The ECB’s loosening of monetary policy will support economic recovery and steel demand growth. More than half of German business representatives expect the economic situation to improve over the next 6 months. Positive expectations are observed in almost all sectors related to steel consumption. We believe that this year there is a possible growth in visible consumption in Germany by 2-3%,» said GMK Center analyst Andriy Glushchenko.

German perspectives

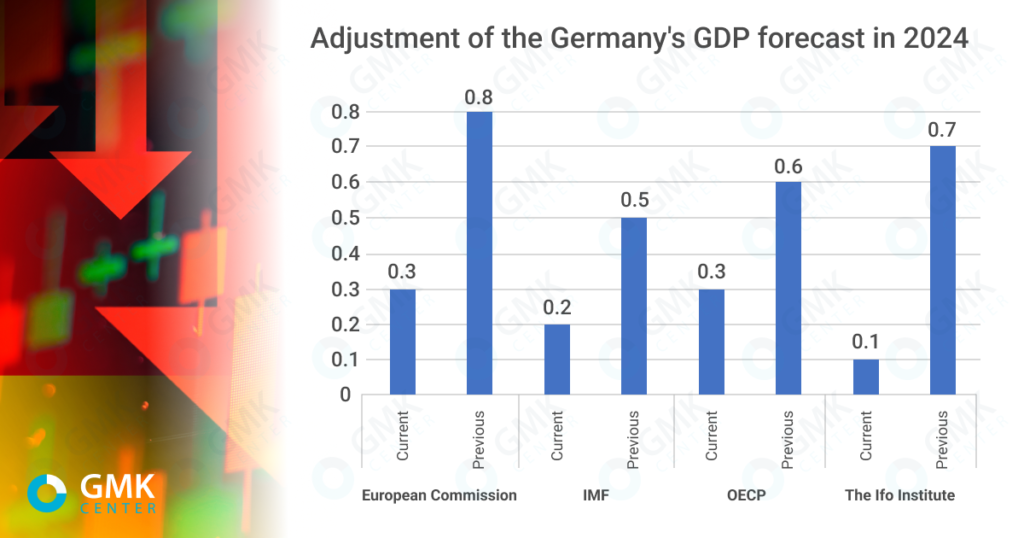

German politicians and analysts expected the dynamics of the German economy to be more positive this year than in 2023, but everything points to a worsening situation. Recently, different institutions have adjusted their forecasts for German GDP growth in a worsening direction. From September 2023 to February 2024, the European Commission twice worsened its forecast for 2024: from 1.1% to 0.8%, and then to 0.3%. The IMF lowered the forecast to 0.2% in April from 0.5% in January. In turn, the German authorities worsened the country’s GDP growth forecast for the current year to 0.2% from 1.3% earlier.

The expected growth dynamics of the German economy in the current year will be lower than the dynamics of GDP growth in the EU as a whole. The European Commission expects GDP growth in the eurozone in 2024 by 0.8%, in the EU – by 0.9%. Recently, the economic downturn in the country has been defined by some experts as structural rather than temporary.

The following factors may support the German economy in 2024:

- Growth of economic activity after the likely reduction of key ECB rates. Analysts expect 3-4 prime rate cuts of 0.25 pp – to 3.5-3.75% this year, the first of which is predicted as early as June.

- The U.S. can help reduce Germany’s dependence on China by becoming the country’s largest trading partner. In 2023, foreign trade with the US (€252.3 billion) was only €0.7 billion lower than with China.

- Rising defense spending in many countries has revitalized the German defense industry. In 2023, Germany exported more than €11.7bn worth of military equipment and ammunition (+40% y/y). It is planned that total German defense spending this year will amount to 2% of GDP, or €72 billion.

- At the end of 2023, German authorities adopted Baupaket, a program to stimulate investment in housing construction, including tax breaks, subsidies and simplified approvals. This should have a positive impact on the construction sector already this year.

At the same time, the expectations of German business are rather multidirectional. DIHK survey showed that 35% of respondents expect the business situation to worsen in the next 12 months, and only 14% expect improvement. In turn, the ZEW economic sentiment index (leading indicator) from the beginning of 2024 shows an improvement in institutional investors’ expectations for the next six months, although assessments of the current state of affairs are depressed. Positive sentiment comes from expectations of rate cuts in the foreseeable future.

The number of negative factors that hamper hopes for the recovery of the German economy is greater and they are weightier in importance:

- Geopolitical risks – rising tensions in the Middle East, the ongoing war in Ukraine, the blocking of shipping in the Red Sea by the Husis.

- Weak domestic demand. GfK estimates that Germans’ propensity to save in February 2024 rose to the highest level since June 2008, while consumer sentiment shows a decline and greater uncertainty.

- Possible prolongation of high interest rate policy. The ECB may start cutting rates as early as 2024 after the 2% inflation target and forecasts of a sustained decline. However, the ECB could also raise rates if inflation strengthens: this is also a possibility. For example, because of rising oil prices due to instability in the Middle East or the cost of maritime logistics after restrictions on shipping through the Red Sea.

- After inflation rises, Germany goes to the other extreme: industrial price deflation. According to Destatis, producer prices in Germany in February 2024 compared to January decreased by 0.4% and by 4.1% compared to February 2023. The year-on-year decline in producer prices has been observed since July last year.

- Weak export demand. Earlier this year, international institutions lowered their forecasts for the growth dynamics of the Chinese economy in 2024, estimating it in the range of 4.5-4.7%.

- Declining order books in industry and construction. According to Destatis, new orders in the manufacturing sector fell by 5.9% in 2023. In the construction sector, both residential and infrastructure new orders are mostly downward trending in 2022-2023.

All indications are that Germany will show at best minimal economic growth this year. The influence of negative factors from 2022 and imbalances accumulated even earlier will also shape the macroeconomic picture in 2024. The first macro indicators for 2024 are still in negative territory. According to Destatis, in February 2024, industrial production decreased by 4.9%, exports – by 4.4% and imports – by 8.7% compared to the same month in 2023. At the same time, industrial production in February showed a gain against January due to the construction sector, which grew by 7.9% m/m.

And if the next «black swans» appear in the world geopolitics and economy (escalation in the Middle East, rising oil prices, new global logistical problems), Germany’s macro indicators may go into “minus” in 2024. This will undoubtedly have a negative impact on the EU economy as a whole.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

23 July 2026

22 July 2026

17 July 2026