Posts Global Market industrial policy 1680 27 November 2025

Ukraine and the European Union must become technological and raw material partners to overcome declining competitiveness

The industrial decline has affected both the European Union and Ukraine, but for different reasons. For the EU, it is the result of global competition, high energy costs, and regulatory pressure. For Ukraine, it is the consequence of decades of systemic problems and a devastating war. However, common challenges create the basis for a strategic partnership: Ukraine can become Europe’s industrial platform, and the EU can become an investor and technological partner for Ukrainian reindustrialization.

The European Union is losing its global competitiveness

The European Union is experiencing a serious systemic industrial decline. According to Eurostat data, industrial production in the EU fell by 2.3% year-on-year in 2024. The capital goods sector was particularly hard hit, falling by 7.5% year-on-year. Since 2022, the overall decline has been around 6%.

The current situation is extremely difficult: businesses are closing, production facilities are being relocated outside the EU, the steel and automotive industries are in deep crisis, high energy costs are driving up expenses, and green transformation projects are being postponed.

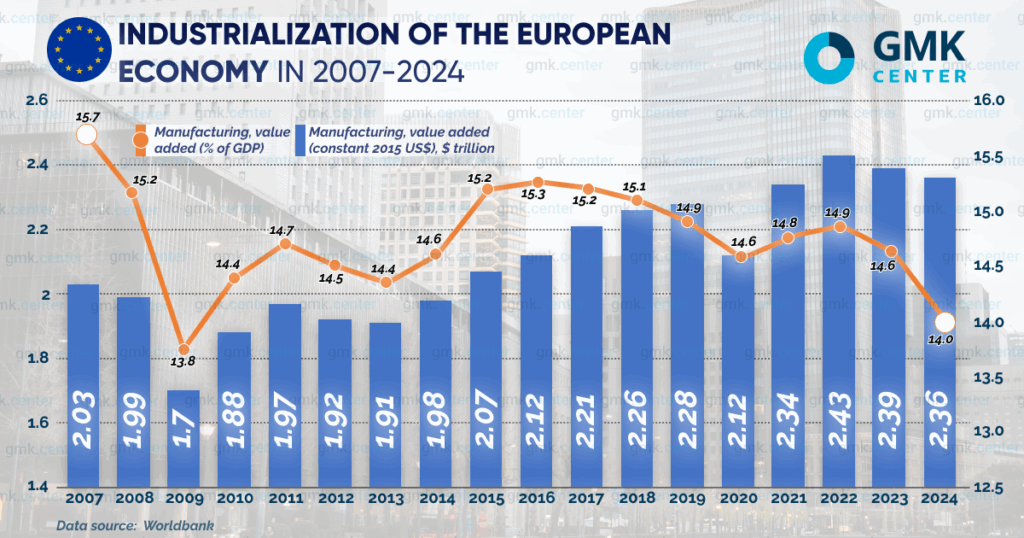

In the long term, the added value of the EU’s manufacturing industry is growing almost steadily: from $2 trillion in 2007 to a peak of $2.43 trillion in 2022 and a slight decline to $2.36 trillion in 2024.

At the same time, the share of manufacturing in GDP has followed the opposite trend. It dropped sharply during the 2007–2010 global financial crisis, then continued a steady decline from 15.2% in 2018 to 14.0% in 2024. This points to a gradual deindustrialization of the European economy and a growing dominance of the service sector.

Among the key reasons for the decline in industrialization in the EU are the following:

1. Globalization and the relocation of production to other countries. Countries with cheaper labor and less stringent regulatory standards appear more attractive for opening new production facilities than the European Union.

2. High cost of electricity and gas. The sharp rise in energy prices followed the start of the war in Ukraine and Europe’s move to phase out Russian fossil fuels. According to the IEA, by the end of 2024, average electricity prices for energy-intensive industrial consumers in the EU were approximately twice as high as in the US and 50% higher than in China. This undermines the competitiveness of European businesses and limits investment.

3. High regulatory burden. European companies face multi-level regulation, which hinders innovation and increases costs. According to the IMF, internal barriers in the single market are equivalent to a 45% tariff on goods and a 110% tariff on services.

4. Lagging behind in technology and innovation. The EU lags significantly behind the US and China in the development of cutting-edge technologies, especially in the fields of AI, semiconductors, and digital technologies. There is not a single European tech giant on par with Google or Alibaba. China’s advances in technology sectors such as engineering and automotive have created serious challenges for the competitiveness of European products.

5. Environmental requirements. Strict climate and environmental standards increase production costs and reduce the competitiveness of European products for export.

6. Dependence on energy imports. Despite the diversification of energy sources after 2022, the EU is still vulnerable to external oil and gas price shocks. In addition, the European Union is critically dependent on imports of rare earth metals and semiconductors from China and other Asian countries. This has a critical impact on the competitiveness and capacity utilization of European industry.

As a result of the above problems, Europe’s global competitiveness is declining. According to the World Bank, the EU’s share of global manufacturing value added declined from 20.8% in 2000 to 16.3% in 2023.

Despite the growth in value added, deindustrialization in the EU is accompanied by a decline in employment. Between 2018 and 2024 alone, 700,000 jobs were lost in the EU’s manufacturing industry.

Chronicle of Ukrainian deindustrialization

The entire recent economic history of Ukraine is a history of deindustrialization, which began in 1991 after the country gained independence.

The disruption of economic ties after the collapse of the USSR, ineffective privatization, corruption, and the lack of improvement in the investment climate led to technological backwardness and a decline in the level of industrialization from 44.6% in 1992 to 17.4% in 2020. At that stage of the Ukrainian economy’s transformation, there was no chance of stopping this decline.

After 1997, the situation was exacerbated by global and domestic crises, and after 2013, by military action. At the start of the full-scale war in 2022, industrial production fell by 36.7% compared to 2021, and construction fell by 65%. The fighting was accompanied by huge financial losses, loss of assets and personnel, and a reorientation of sources of raw materials, logistics, and sales markets.

As the fighting continues, the statistics on losses are growing. According to KSE estimates, as of October 2024, direct documented damage to infrastructure amounted to $170 billion, including the destruction of industrial assets worth $14.4 billion.

Absolute value added in processing industry fell from $20 billion in 2007 to $6.7 billion in 2022, the lowest level for the period. After the full-scale invasion, the industry collapsed, but a partial recovery began in 2023–2024. Overall, the indicator for 2007–2024 fell by more than 2.5 times.

The share of manufacturing in GDP fell from 20% in 2007 to 7.6% in 2022. Full-scale aggression led to a decline in the indicator in 2021–2022 from 10.3% to 7.6%. Growth in subsequent years remains significantly below pre-war levels. Since the start of the war, the manufacturing sector has shown weak recovery amid deep structural deindustrialization.

The industrial crisis is exacerbated by structural problems: high electricity and gas prices, expensive logistics, a shortage of working capital, limited access to debt financing, and a shortage of personnel.

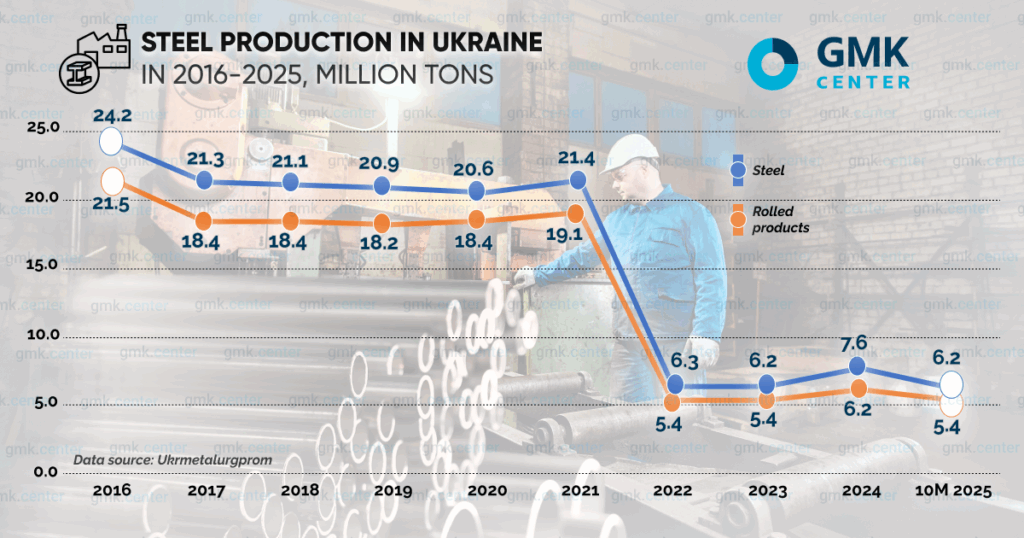

A classic example of deindustrialization is the Ukrainian steel industry, which has suffered critical losses due to military operations. Steel production has fallen from more than 50 million tons per year in Soviet times to 21 million tons in 2021. After the start of full-scale war, steel output fell to 6.3 million tons in 2022. By 2024, production had recovered to 7.6 million tons, approximately 15% of the original figures.

It is important to note that Ukraine has never had a comprehensive industrial and investment policy to create a favorable business climate. The use of incentives and subsidies has been fragmented and has not compensated for the lack of strategy. Isolated effective examples of using industrial policy tools has helped create several key segments of agricultural processing in which Ukraine now ranks among the leaders in Europe and globally.

Joint decisions

Without serious measures to protect European industry and strengthen its technological position, Europe risks losing key manufacturing competencies. To overcome deindustrialization, Ukraine and the EU can develop a set of joint measures.

Despite large-scale deindustrialization, war, and dependence on European funds, Ukraine has competitive advantages that are useful to the European Union, given its geographical proximity and prospects for European integration. Here are Ukraine’s key opportunities for the EU:

1. Creation of joint production chains in critical industries. Ukraine has significant reserves of critical minerals (lithium, titanium, graphite, and rare earth elements), which can be used to create production chains ranging from the mining and processing of critical materials to the manufacture of batteries, semiconductors, and green technologies. This will allow all parties to increase competitiveness and reduce dependence on external suppliers.

2. Source of cheap energy resources and green electricity. Ukraine has significant potential for developing renewable energy sources (bio, wind, solar energy) and can export electricity, helping to reduce the energy costs for European industries.

3. Participation in European value chains. Ukraine has the potential to fill gaps in areas where the EU faces shortages or is retreating due to high costs, such as intermediate goods, auto parts, and raw materials critical for the green transformation of the steel industry (DRI pellets, HBI), etc.

4. Relocation of production. As part of post-war reconstruction, Ukraine could become a hub for energy-intensive production by European companies, provided that energy infrastructure is developed and electricity tariffs remain stable.

Conclusions

Ukraine and the European Union are facing trends of deindustrialization that are different in origin but similar in their consequences: a decline in the role of manufacturing, rising energy prices, and a loss of competitiveness. At the same time, Ukraine is in a worse position, facing war and political crisis, with an economy dependent on external financing.

However, the main issue is not similar economic problems, but common geopolitical and defense interests. Ukraine and Europe are now doomed to act together.

In such conditions, there is room for cooperation. Ukraine can become Europe’s industrial platform – a source of inexpensive electricity, a base for energy-intensive industries, and part of new value chains. The EU can be an investor, a technological partner, and a sales market. Joint reindustrialization can strengthen both sides and reduce their dependence on crises and other geopolitical players.

Integrating industrial potential opens the door to shared competitiveness and the development of an economic model resilient to global competition.

The European Union has the financial and technological capacity to support Ukraine’s industrial development and the political motivation to include it in its production chains as an element of European strategic autonomy. The transition from exporting raw materials to processed products and access to European structural transformation funds are critically important for Ukraine.

To realize these advantages, the active phase of hostilities must end, and Ukraine must receive firm guarantees of peace and security.

-

02 July 2026

16 June 2026

10 June 2026

27 May 2026