Posts Industry steel consumption 1096 26 February 2026

Steel trading companies recorded an average increase in sales of 10–15% in real terms

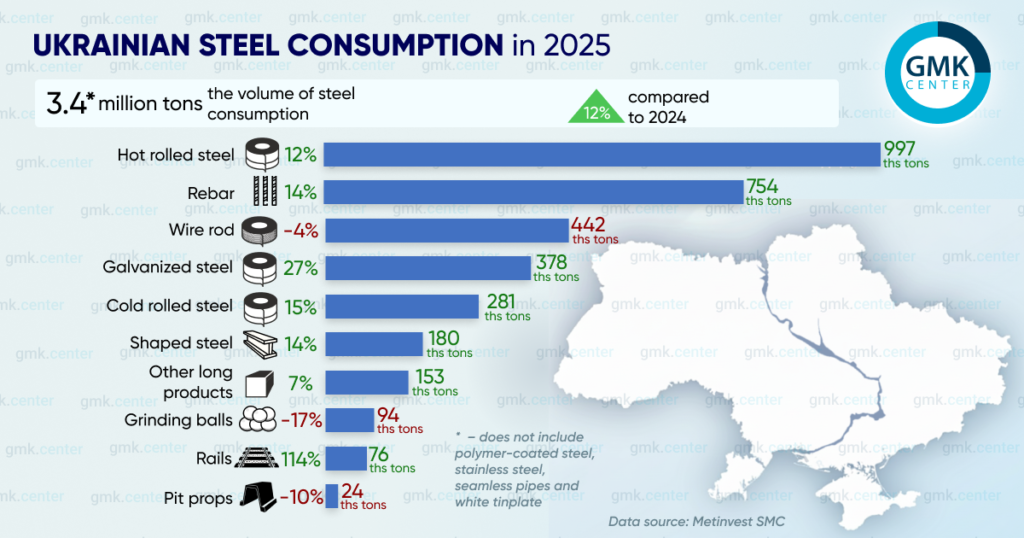

The Ukrainian steel market ended 2025 with growth: steel consumption increased by 12%, and market capacity reached 3.4 million tons. These figures reflect a combination of weakening sales amid slower demand in the infrastructure sector and lower output caused by power supply disruptions at many customer facilities. They also point to intense competition, compressed margins, labor shortages, and delays in payments under government contracts. GMK Center investigated what was happening on the Ukrainian rolled steel market.

Overall market dynamics

In 2025, steel consumption in Ukraine grew by 12% after increasing by 10% in 2024. According to Metinvest-SMC estimates, the capacity of the Ukrainian steel market last year was 3.4 million tons (excluding polymer-coated sheets, stainless rolled products, seamless pipes, and tinplate).

During the year, the dynamics of steel consumption in different segments were uneven. In the construction segment, the season got off to a slightly delayed start in May. After that, typical seasonal patterns prevailed, with demand peaking in mid-year and easing slightly in November and December.

The pattern was different in the machinery sector. Demand for steel products was strongest in the first half of the year and then declined in the second half. TAKT Metal attributes this downturn to insufficient funding for the defense industry.

Steel trading companies surveyed by GMK Center reported an average 10-15% increase in steel product sales volumes in 2025. However, overall sales of the leading market participants have yet to return to pre-war levels.

Market trends

Steel traders highlight the following key market trends:

- Slowdown in steel consumption in infrastructure construction. For most of 2025, state funding for infrastructure projects remained low. Only in the fall, after the resumption of systematic attacks on energy infrastructure, did the authorities begin to strengthen the protection of energy facilities again. Last year the volume of construction work completed in Ukraine increased by 15.5 y/y. The sector returned to growth only in the summer. In January-May 2025, construction activity was still down 7.5% compared to the same period a year earlier.

- Declining margins in many segments. According to estimates by Vitaliy Prytula, director of Euro Metal, net margins rarely exceed 5% today.

- Impact of power outages. Steel service centers are generally able to operate using generators. However, power shortages reduce effective demand: customers are forced to partially or completely halt production or construction. This impact was particularly noticeable at the end of 2025.

- High competition. The market continues to experience fierce price competition with instances of dumping, which significantly limits traders’ ability to raise prices.

- Increase in imports of steel products. According to Ukrmetallurgprom, in 2025, imports of rolled steel products increased by 31.2% y/y, and the share of imports in steel consumption increased by 2.5 p.p. to 40.1%. This is the highest figure since Ukraine gained independence. Turkey and China remain the main importing countries.

- Increasing staff shortages. Labor shortages are pushing wages higher, but in a highly competitive market this pressure is largely absorbed through lowering margins. In some companies, staff shortages reach 30% of total requirements.

- Increased importance of fast delivery. The demand for prompt shipment requires sufficient warehouse stocks, which leads to the freezing of working capital in commodity assets.

- Deferred payments on government contracts. According to Roman Anzin, CEO of Vartis, this puts a serious strain on the working capital of suppliers and manufacturers and forces them to borrow.

- Shift in sales of construction products to western regions. In 2025, the region saw active construction of logistics hubs, warehouses, grain elevators, and industrial facilities, alongside robust growth in residential and recreational development.

At the end of 2025, serious logistical disruptions reemerged for the first time since the western border crossings were unblocked in the spring of 2024. The main reason was a series of systematic Russian strikes targeting port infrastructure in Odesa and the Danube ports. This risk is likely to remain relevant in 2026.

«A lot of steel is imported from Turkey by barges. Currently, a large number of barges are waiting to be unloaded in Romanian territorial waters. Many Turkish shipowners who used to deliver steel products to Ukraine have refused to enter Ukrainian ports. This has already led to a shortage in the 30–50 mm plate segment,» said Vitaliy Prytula.

Internal logistical problems may prove to be just as serious.

«There has been a reduction in the supply of logistics services due to a shortage of drivers and vehicles, which is putting pressure on pricing and causing significant fluctuations in the cost of services. There are difficulties with delivering goods to eastern regions and transporting products from production facilities in high-risk areas. Logistics companies often refuse to work in these areas, which complicates the continuity of supplies,» Roman Anzin emphasized.

An additional challenge for road transport in the first half of 2026 may be damaged roads after a harsh winter.

Demand by type of steel products

According to Metinvest-SMC, the capacity of the rebar segment grew by 14% to 754,000 tonnes. Infrastructure and defense projects were the main drivers. Additional support came from growth in commercial, residential, and recreational construction in the western regions.

The second subgroup of the construction product range, structural shapes, also showed growth. Consumption of beams, angles, and channels increased by 14% to 180,000 tonnes, while rails increased by 114% to 76,000 tonnes. The largest growth in the rail segment was ensured by the delivery of previously contracted volumes to Ukrzaliznytsia for the construction and repair of railway tracks. Other structural shapes (strip, round and square bar) grew by 7% to 153,000 tons.

The flat rolled products segment showed positive dynamics at the end of 2025:

- galvanized sheets – by 27%, to 378 thousand tons;

- cold sheets– by 15%, to 281 thousand tons;

- hot sheets– by 12%, to 997 thousand tons.

According to Olexander Vedernikov, Head of Analytics and Pricing at Metinvest-SMC, growth in the hot-rolled sheet segment was driven primarily by stronger domestic demand from pipe manufacturers amid rising consumption of pipe products. Meanwhile, expansion in the galvanized sheet segment was linked to higher output of polymer-coated sheets and increased demand for galvanized coils.

Last year, consumption declined across several categories of rolled steel products

- grinding balls – −17%, to 94 thousand tons, due to a decrease in iron ore production and a reduction in the utilization rate of iron ore mining and processing enterprises;

- pit props (mine supports) – −10%, to 25 thousand tons, amid the scaling back of operations at mines located in the combat zone, most notably the suspension of coking coal extraction at the Pokrovske mine;

- wire rod – −4%, to 442 thousand tons, due to increased competition from Chinese and Turkish manufacturers in both the domestic and European markets.

For comparison: in 2024, pit props were the only market segment that showed a significant decline – by 2.5 times, to 28 thousand tons (for the same reasons as in 2025). The grinding ball segment showed the highest growth in 2024 – by 71% to 113 thousand tons, thanks to increased consumption at Ukrainian iron ore mines, which increased production after the opening of the sea corridor for the export of raw materials. This clearly illustrates how the structure of demand for certain types of rolled steel products is changing in the context of the war.

Particular attention should be paid to rising consumption in the machinery sector, which is heavily oriented toward defense orders.

«The largest growth was observed in the segment of special and alloy steels, calibrated rolled products, and products with increased quality requirements. Demand for standard items remained subdued, while demand for niche and technically complex products increased. In 2025, sales of calibrated rolled products increased by 16%, which correlates with the overall dynamics of demand in this segment,» said Igor Udovychenko, Director of Marketing and Sales at TAKT Metal.

Sectoral and regional consumption structure

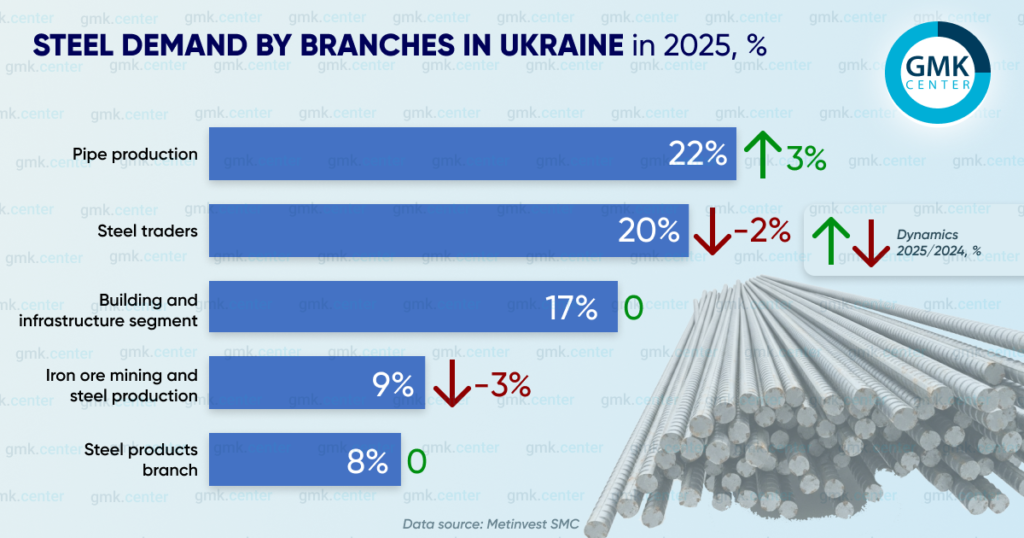

An analysis of demand by end-use sector in 2025, based on data from Metinvest-SMC, indicates the following shifts compared with 2024

- The pipe industry became the largest consumer: its share in the total portfolio increased from 19% to 22%.

- Steel traders ranked second in terms of volume, but their share in the sales structure decreased to 20% from 22% a year earlier.

- The share of construction companies remained at 17%.

- The share of iron and steel companies decreased by 3 percentage points to 9% due to lower production at mines and reduced output at mining and processing plants.

- The share of steel processing companies remained stable at 8%.

The main sources of demand in 2025 were the defense industry and the construction industry. Within the defense-oriented segment of the machinery steel market, related engineering and repair industries account for roughly 50% of the order book.

«The main growth was driven by defense orders and a partial renewal of industry. Civil engineering has not yet achieved stable growth: there was a significant decline in railcar manufacturing and mining machinery manufacturing. Agricultural engineering showed positive dynamics,» said Igor Udovychenko.

The regional structure of steel product sales remained largely unchanged. According to Alexander Vedernikov, the majority of shipments to end users remain concentrated in industrialized regions that include cities with populations exceeding one million, namely Dnipropetrovsk, Kyiv, Kharkiv, Odesa, and Lviv regions. Together, they accounted for 74% of total sales. The smallest volumes of supplies were recorded in the frontline regions of Chernihiv, Sumy, and Kherson, as well as in Rivne region.

Market development forecast

The state of the steel trading market is determined primarily by the nature of hostilities and the general state of the economy. In both areas, there are few grounds for optimism in 2026. Metinvest-SMC expects that, under a conservative scenario, market capacity could grow by 3.5% y/y to 3.5 million tons. Vartis forecasts growth in steel product sales of no more than 10% if hostilities continue.

-

OpinionsIndustrysteel consumption

13 July 2026

24 June 2026

18 June 2026

15 June 2026