Infographics steel capacities 579 30 March 2026

Now Ukraine has no excess capacity, while room for steel production growth is limited

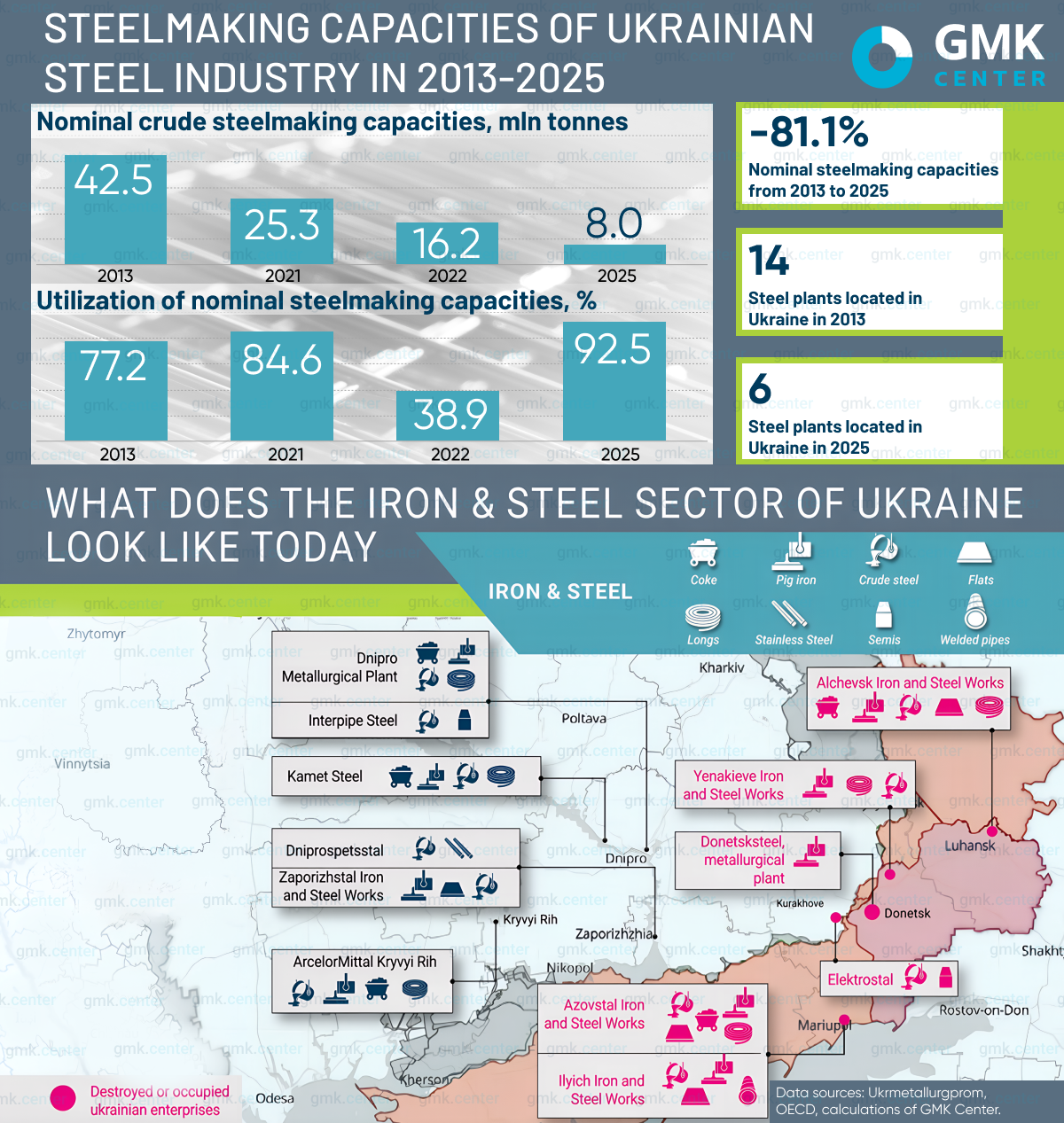

Between 2013 and 2025, nominal crude steelmaking capacities of Ukraine declined by 81.1%, from 42.5 mln tonnes to 8 mln tonnes, according to Ukrmetallurgprom (Ukrainian steel association). Over the same period, the number of operating steel plants decreased from 14 to just 6, reflecting the loss of key industrial assets as a result of Russia’s agresssion.

In 2013, Ukraine’s steel industry operated with large, export-oriented capacities inherited from the Soviet era. The first major structural break occurred after 2014, when the first military conflict in eastern Ukraine led to the loss of control over parts of the Donetsk and Luhansk regions. As a result, several large steelmaking facilities were effectively removed from Ukraine’s industrial system. Ukrainian steelmaking capacities decreased to 25.3 mln tonnes by 2021.

A second and more severe shock occurred in 2022 following the full-scale invasion by Russia. The destruction and occupation of additional industrial assets, including major integrated steel plants in Mariupol, led to a further sharp decline in nominal capacity to 16.2 mln tonnes. At the same time, steel production dropped more sharply due to disruptions in logistics, energy supply, labor availability, and export channels. As a result, capacity utilization temporarily collapsed to around 39% in 2022, reflecting the scale of the immediate economic shock.

In 2022, nominal annual capacity dropped to 16.2 mln tonnes, of which around 8.2 mln tonnes were decommissioned later. For example, Dnipro Metallurgical Plant has halted its BF-BOF route and is considering the construction of EAF to resume steelmaking in the future. Given constrained investment during wartime, approximately 8 mln tonnes represents the maximum capacity that can be maintained in operation by Ukrainian steel producers.

Despite the dramatic contraction in capacity, utilization rates have remained quite high outside of the exceptional disruption in 2022: 77.2% in 2013, 84.6% in 2021, 92.5% in 2025.Ukraine had competitive advantages in steel production which allowed Ukrainian steelmakers to supply their products globally.

The high level of capacity utilization observed in 2025 underscores the resilience and adaptability of the remaining steel producers. Despite operating under conditions of ongoing military risk, logistical constraints, and energy challenges, these enterprises have managed to continue production. However, the high utilization rates in 2025 suggest that there is limited room for further increases in domestic steel output without additional investment.

Now Ukraine doesn’t have any excess steelmaking capacities. Increase in steel demand associated with post-war reconstruction will need additional volumes of steel imports since capacities of Ukrainian producers will not be able to satisfy all consumers.

-

02 July 2026

06 July 2026

01 July 2026

22 June 2026