Infographics ArcelorMittal Kryvyi Rih 281 22 June 2026

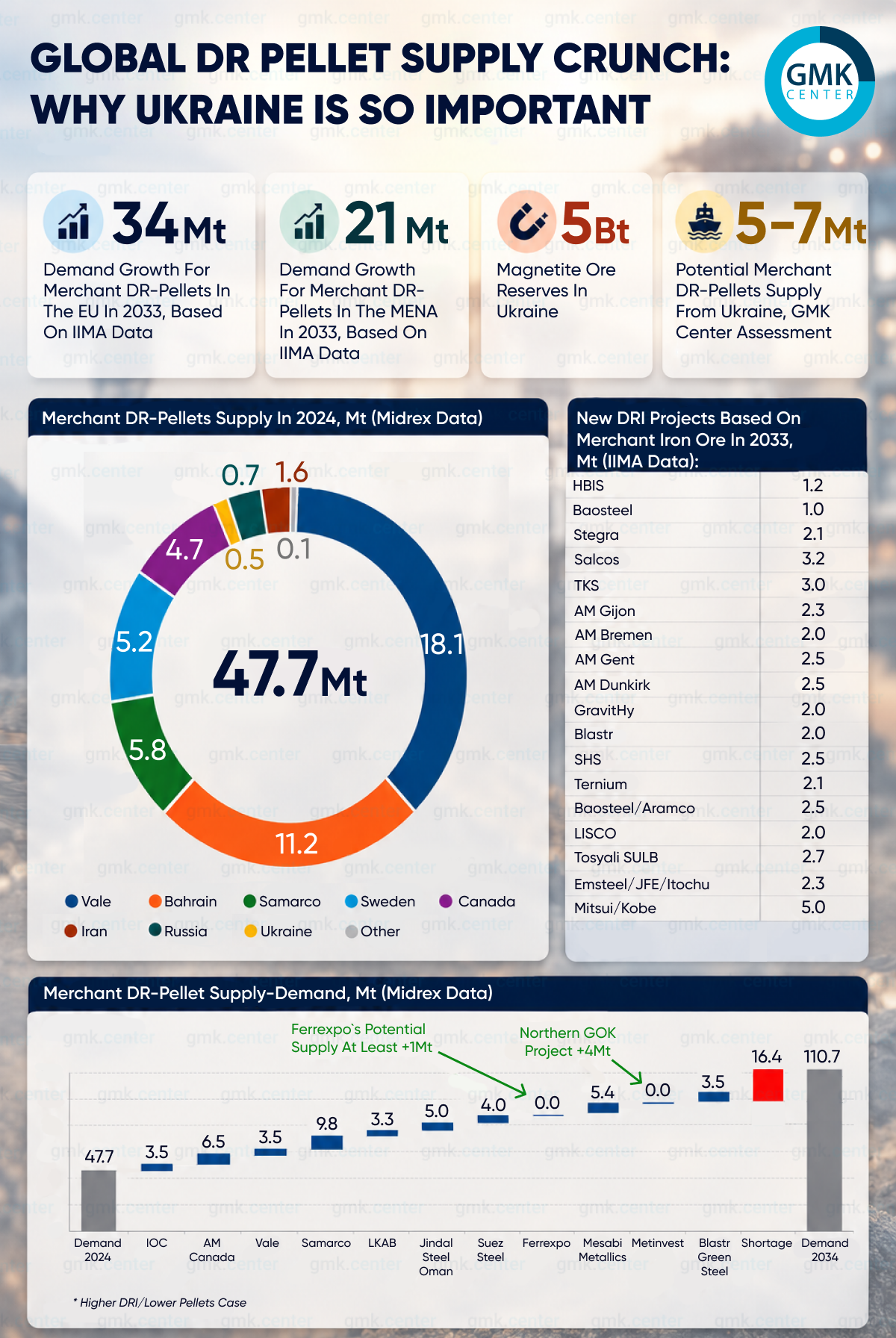

Potential merchant DR-pellets supply from Ukraine could reach 5-7 million tonnes

While Midrex’s analysis for 2024 shows Ukraine exporting just 0.5 million tonnes of DR-grade pellets, this reflects the realities of war and constrained logistics, not production potential. Both of Ukraine’s major iron ore producers have proven they can deliver far more.

Metinvest’s Central GOK facility, upgraded in 2021 with a new flotation circuit to produce DRI-grade feed, has a nameplate capacity for high-grade DR pellets of 2.3 million tonnes per year. The company has demonstrated output approaching 300,000 tonnes in a single quarter at this plant, equivalent to an annualized rate of around 1.2 million tonnes.

Ferrexpo, for its part, achieved quarterly production of DR pellets at 263,000 tonnes in Q3 2022, equivalent to an annualized run-rate of over 1 million tonnes. After a pause in 2023, the company resumed DR pellet production in 2024, ramping up to a total of nearly 0.5 million tonnes for the year.

Ukraine’s true potential lies is in brownfield expansions already underway, offering a faster and more capital-efficient path to market compared to greenfield projects elsewhere.

- Metinvest Northern GOK: The project involves two key contracts signed in late 2025: a basic engineering agreement with Austria’s Primetals Technologies to modernize the pelletizer, and a separate contract with Finland’s Metso for the basic engineering of a new flotation complex. The goal: to produce around 4 million tonnes of DR pellets per year.

- Ferrexpo Upside: While Ferrexpo currently produces a modest volume of DR pellets, the company has the potential to scale up to 3-5 million tonnes per year of DR-grade material should it invest in additional flotation capacity. Even assuming no new projects and maintaining the status quo, Ferrexpo’s supply could be no less than 1 million tonnes.

Midrex’s latest modelling suggests a potential merchant DR pellet supply deficit of 16.4 million tonnes by 2034 under its lower supply case, even as demand surges in the EU (34 mt) and MENA (21 mt). Ukraine’s contribution, from just Metinvest and Ferrexpo, could realistically exceed 7 million tonnes of DR pellets.

And the potential goes further. Even before the war, other projects were in development:

- Southern GOK: already producing 3 million tonnes of Fe68-69% concentrate and had planned a pelletizing plant.

- ArcelorMittal Kryvyi Rih: had announced a 5 million tonnes pelletizing project (primarily captive).

- BlackIron: a greenfield project aimed at producing 8 million tonnes of Fe68% concentrate.

With at least 20 million tonnes of potential DR-feed production in the long term, Ukraine is poised to play a decisive role in balancing the global DR pellet market. At a time when the industry is scrambling to secure supply for the green steel transition, the country’s existing operations and accelerated brownfield projects offer a competitive, proven, and significant source of the high-grade raw materials the sector urgently needs. Ignoring this potential means understating the supply-side equation.

-

02 July 2026

06 July 2026

01 July 2026

18 June 2026