Posts Green steel green steel 3398 05 May 2025

Steelmakers face an «unexpected» problem of expensive energy and immature technologies

Leading steel players are revising their previously approved decarbonization strategies, while placing significant requirements on national governments. GMK Center has examined these developments and their potential implications.

Hydrogen on hold

There are currently three ways to reduce CO2 emissions in steel production:

1. Using energy from renewable sources for electric arc furnace melting (R-EAF scrap-based).

2. DRI production using hydrogen to reduce iron up to 99.99%, followed by smelting in EAF

3. Electrolysis of molten iron oxide (MOE).

The latter option is the most complex in terms of technology. The first one has certain limitations: EAF uses scrap metal as a raw material. And the uninterrupted supply of this resource is becoming increasingly problematic.

By establishing hydrogen-based direct reduction from iron ore, it becomes possible to fully phase out blast furnace ironmaking – the core component of the BF-BOF route, which is responsible for the majority of CO₂ emissions in the steel sector.

That is why leading European producers have chosen option 2 as the main one. In particular, in July 2021, ArcelorMittal SA announced the construction of an H2 DRI plant in Gijón, Spain, with an annual capacity of 2.3 million tons. The project cost at that time was €1 billion.

It was expected that the new plant would be operational in 2025 and start supplying products to ArcelorMittal’s Sestao electric arc furnace plant. But… at the end of November last year, the concern officially announced that the project was delayed indefinitely. The reasons given were the unfavorable market and energy situation, as well as the slow development of green hydrogen infrastructure.

Germany’s largest steelmaker, Thyssenkrupp AG, faced similar problems. At the end of March, it suspended (also indefinitely) a tender for the purchase of “green” hydrogen for the 2.5 million tons per year H2 DRI plant in Duisburg. The tender itself was announced in February 2024.

“It is becoming clear that the proposed prices will be significantly higher than expected, and other framework parameters of the hydrogen economy, which is developing more slowly than expected, will change significantly,” the concern said in a commentary.

At the end of March, S&P Global estimated the cost of producing “green” hydrogen by alkaline electrolysis in Germany at €9.35/kg. In December last year, it was €14.5/kg, which is much more expensive.

However, given that the Duisburg plant needs 151,000 tons of Н2 over 10 years, this is indeed an astronomical amount. Therefore, hydrogen-based steelmaking projects in Europe are currently on hold.

“We will continue to use hydrogen as soon as it becomes economically feasible and technically possible,” Thyssenkrupp promised.

In this regard, scrap-based R-EAF is becoming a priority for decarbonizing the steel industry everywhere. But it is not all that simple.

Consumer reaction

It’s not entirely accurate to claim that the high price of green steel is the primary barrier. Cost wouldn’t be an issue if buyers were truly willing to pay – but the reality is, they’re not, despite earlier commitments.

The automakers General Motors Co, Jaguar Land Rover Corp, Volvo Group AB, Mercedes-Benz Group AG, and Volkswagen AG have all previously stated that they will switch to 100% carbon-free steel in automotive production by 2050. But 2050 is a long way off. In the meantime…

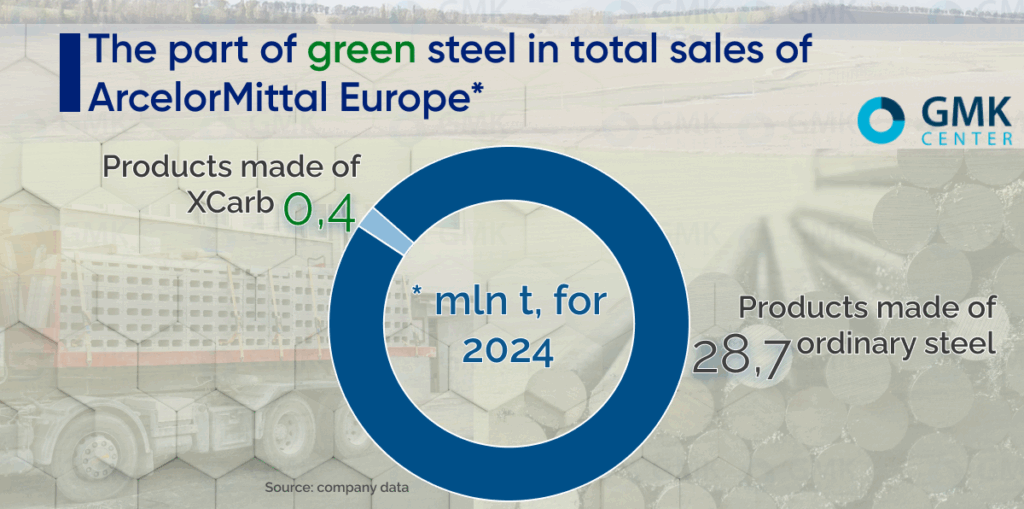

ArcelorMittal Europe sold 400 thousand tons of its carbon-free XCarb steel in 2024, doubling the figure for the previous year. This seems to be a very good result. But if you compare it with the total volume of steel sales, it becomes clear why the concern announced in February this year that it would partially suspend its European plan to decarbonize production.

“Although customers are interested in low-carbon steel, their willingness to pay a premium is limited. So, in fact, they cannot buy such steel. Because we sell it only at a premium,” explained Genuino Cristino, CFO of ArcelorMittal.

An analysis of the market situation fully confirms this thesis. According to Fastmarkets, in mid-April, price premiums for green steel in the EU were at €200-300 per tonne, depending on the carbon footprint. At the same time, buyers were willing to pay €100-150, which is half as much. Representatives of the plants responded by saying that the maximum discount they could accept was €20-30 per ton. Thus, supply and demand are currently far apart.

“According to our estimates, the green premium may exist on the market for a very short time and will not be a decisive factor for investments in the green steel transition,” comments Stanislav Zinchenko, CEO of the GMK Center.

Key terms and conditions

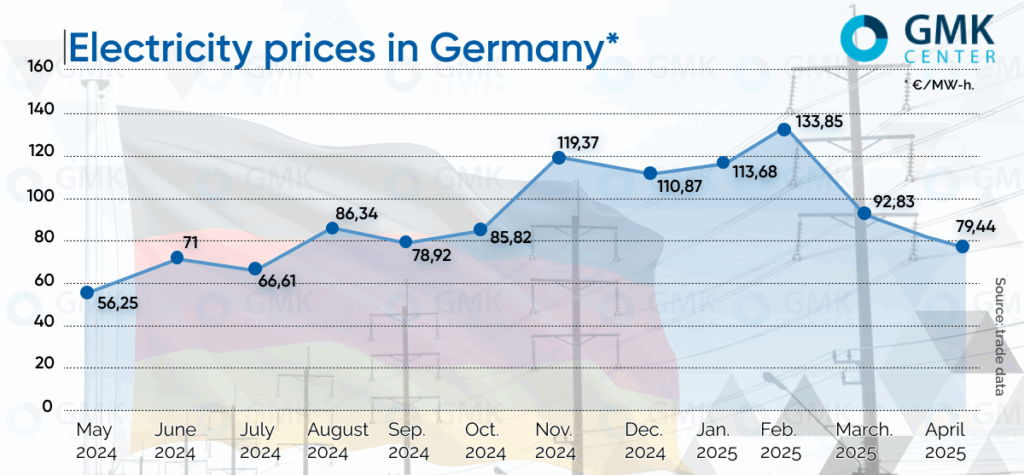

Thomas Bünger, CEO of ArcelorMittal Germany, says that the main reason for the suspension of decarbonization is the high cost of electricity. According to him, a price of €50-55/MWh would be acceptable for R-EAF scrap-based electric steelmaking, as it was before the energy crisis. The last time electricity in Germany was around this level was a long time ago.

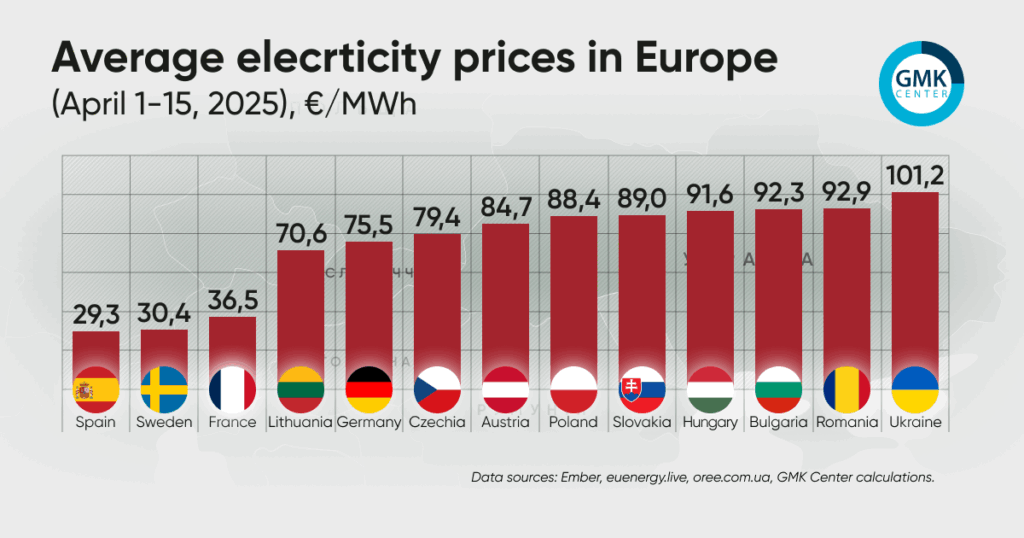

That is why the issue of cheap electricity has become the main one for the decarbonization of the European steel industry. At the end of April, ArcelorMittal Poland CEO Wojciech Koszuta announced the company’s readiness to make a large-scale conversion of the plant in Dąbrowa Górnicza from BF-BOF to R-EAF scrap-based. According to him, this requires guarantees of competitive electricity prices.

It is clear that the market cannot provide such guarantees. Only the government can do this. In this case, the government of Poland. It needs to make appropriate regulatory decisions. So far, however, the authorities in Warsaw and other European capitals are in no hurry to meet the demands of the steel industry.

In this regard, the largest Czech manufacturer, Trinecke zelezarne Group AS, postponed previously approved key projects to decarbonize production at the end of April. For now, for at least 2 years. This refers to the construction of electric arc furnaces and related infrastructure at the plant in Tršinka.

Just a month earlier, in March, the Czech government had pledged its support to the company, even signing a memorandum. But it seems that commitment never moved beyond words. As a result, the green transition has stalled – not only for Trinecke Zelezarny, but for the European steel sector as a whole.

Obviously, the process will move forward if three conditions are met simultaneously: affordable electricity, economically viable hydrogen production technologies, and public investment. Because companies will not be able to afford such projects on their own.

ArcelorMittal estimates it will need $40 billion to decarbonize its entire European operations — an enormous sum, even for the world’s second-largest steelmaker. Public funding is essential, and while support does exist, it falls well short of what’s needed

As of February 2025, the concern has received €1.3 billion in green subsidies from the German government, €850 million – from France, €460 million – from Spain, €280 million – from Belgium, and $651 million – from Canada. So far the state participation does not reach even 10% of the total price of the issue.

The Ukrainian aspect

Decarbonization is one of the priorities of the Ukrainian steel industry. Its necessity stems from Ukraine’s commitments made in 2021 under the Paris Climate Agreement – to reduce CO2 emissions to 65% of 1990 level by 2030.

In addition, all Ukrainian steel mills had plans to decarbonize as they prepared for the requirements of the European market.

At the same time, the problem of competitive electricity prices is even more acute for Ukrainian steel mills than for European ones. Not only in the context of the green transition. In general, for steel production.

Obviously, for a number of reasons, it makes no sense for Ukraine to blindly copy the European decarbonization model. Each country has its own optimal option, depending on the available resources. The European Union has energy from renewable sources and scrap metal. Plus, it has more opportunities to finance hydrogen technologies. Ukraine does not have this – all efforts and money after the war will be directed to rebuilding infrastructure.

Unlike the EU, however, Ukraine has large reserves of high-quality iron ore suitable for beneficiation. This opens the door to launching DRI production based on natural gas, with the potential to shift toward low-carbon steelmaking through the DRI-EAF route powered by nuclear energy. The country already operates three nuclear power plants, and there are viable plans to expand their capacity further.

But for this, the industry needs subsidies at the European level. And affordable prices for electricity and natural gas.

“Without affordable and cheap electricity, the steel industry in Europe and Ukraine has no future,” summarizes Stanislav Zinchenko.

-

Opinions Industry steel market

17 June 2025

29 May 2025

21 January 2025

28 November 2024