Posts Industry Metinvest-SMC 4194 12 February 2025

Demand for sheet and shaped rolled products, steelware and grinding balls increased most of all

By the end of 2024, the capacity of the Ukrainian steel consumption market grew by only 10%. The growth dynamics could have been higher, but it was hindered by the reduction in infrastructure construction, power shortages after missile attacks on the Ukrainian energy sector and increased mobilization. The latter two factors reduced economic activity in the second half of the year, which affected demand for steel products.

Despite the difficult situation on the frontline and in the economy, steel trading market operators forecast a slight increase in sales of steel products and the capacity of the domestic market as a whole for the current year. This may be facilitated by the realization of pent-up demand, comparative cheapness of steel products and the desire to save funds from depreciation due to inflation.

Slowdown in growth

At the end of last year, the dynamics of steel consumption in Ukraine slowed down to 10%, which was expected after a record recovery growth of 2.2 times by the end of 2023. According to Metinvest-SMC estimates, the capacity of the Ukrainian market for steel products amounted to 3 million tons (excluding polymer-coated rolled products, stainless steel and white tinplate).

“Domestic market provided us with good dynamics only in the first half of the year. There were some infrastructure projects. But then, when they were finished, the market was not going at the speed that we expected,” explains Mauro Longobardo, CEO of ArcelorMittal Kryvyi Rih.

Let us describe in more detail the reasons for the slowdown in steel consumption in the second half of last year:

- Electricity shortages.

Last year, Russia launched 13 massive missile attacks on the Ukrainian energy sector. This resulted in reduced energy supplies to enterprises, lower production activity and lower demand for steel products.

- Slowdown in the sphere of construction and restoration of infrastructure.

If in the first half of last year the driver of construction growth in Ukraine was engineering structures (+46.1% y/y), then at the end of January-September 2024 the dynamics in this category decreased to 25.4% y/y, giving the first place in growth to the construction of non-residential buildings (27.2% y/y).

“While in the first half of 2024, infrastructure projects showed growth relative to the same period of the previous year, in the second half of the year the demand in this segment significantly decreased. And as a whole, by the end of 2024, it fell almost 3 times relative to 2023 due to a large comparison base, which was observed in the second half of 2023”, said in the commentary of GMK Center Olexander Vedernikov, Head of Analytics and Pricing Department of Metinvest-SMC.

- Strengthening of mobilization and shortage of personnel.

Intensified recruitment of persons liable for military duty in the AFU has led to a shortage of labor, as well as a partial decline in economic activity in a number of steel-consuming industries.

“Demand in the second quarter of 2024 decreased by 6% y/y. At the same time, Q4 2024 turned out to be more optimistic and the market grew by 11% y/y and 9% y/y,” says Vedernikov.

Market trends

All steel trading companies surveyed by GMK Center in 2024 showed growth in sales of steel products in physical terms by an average of 15%, in some cases for narrow segments of rolled steel products – up to 25%.

Among the key market trends, steel trading companies name the following:

- Slowdown in consumption of steel products in the sphere of infrastructure construction. The volume of financing of state infrastructure projects in 2024 was at a low level, so the volume of construction work in this area decreased, and many projects were not completed by the end of the year due to lack of financing.

- Reduced margins in many segments. This is due to work in the conditions of a prolonged price drop in the market.

- Consolidation of major players in the steel trading market. As well as displacement of weak market operators that do not have sufficient margin of safety.

- Increase of steel import inflow to Ukraine. According to OP Ukrmetprom, last year imports of rolled steel rose 10.2% y/y – to 1.24 million tons. The specific weight of imports in the structure of steel consumption in Ukraine by the end of 2024 increased by 5.6 p.p. to 37.6% – to 37.6%, although it is lower than 39% in 2022.

- There is an increasing shift of construction grade sales to western regions.

“Western Ukraine has now become a big construction site. We see that there is active hotel and recreational construction in the Carpathians and industrial construction (including in industrial parks) for agro- and food enterprises – grain elevators, various processing facilities, etc.,” Vitaliy Pritula, director of Evrometal, told GMK Center in a commentary.

Demand by types of steel products

At the end of 2024, there was an increase in consumption of almost all types of steel products. According to Sergiy Kovalenko, Commercial Director of the Vartis network of steel centers, last year demand increased for such types of steel products as:

- rolled sheets (for the construction of shelters for power facilities);

- pipes;

- hardware products (for use in defense and fortification structures).

The ball segment showed the largest growth – by 71%, up to 113 thousand tons. Significant growth of the balls market was due to increased consumption at Ukrainian mining and processing plants, which increased production due to the opening of the sea corridor for iron ore exports.

According to Metinvest-SMC, the capacity of the rebar segment grew by 5% – to 664 thousand tons, wire rod – by 11%, to 460 thousand tons. Infrastructure and defense projects remained the main drivers of growth in these segments. Construction activity in the western regions also picked up, indicating a renewed interest in resort real estate and related infrastructure.

Another subgroup of construction steel products – the shaped rolled products segment – also showed growth. The consumption of beams, angles and channels increased by 20% to 159 thousand tons, and rails – by 15%, to 35 thousand tons.

The flat-rolled products segment showed multidirectional dynamics at the end of 2024:

- galvanized rolled products – growth by 32%, up to 297 thousand tons;

- hot-rolled products – growth by 9% to 892 thousand tons;

- cold-rolled products – decrease by 2%, to 245 thousand tons.

According to Metinvest-SMC estimates, the only market segment that showed a significant decline was mine racks, which decreased 2.5 times to 28 thousand tons. This was caused by the reduction in output and curtailment of activities at mines in the war zone.

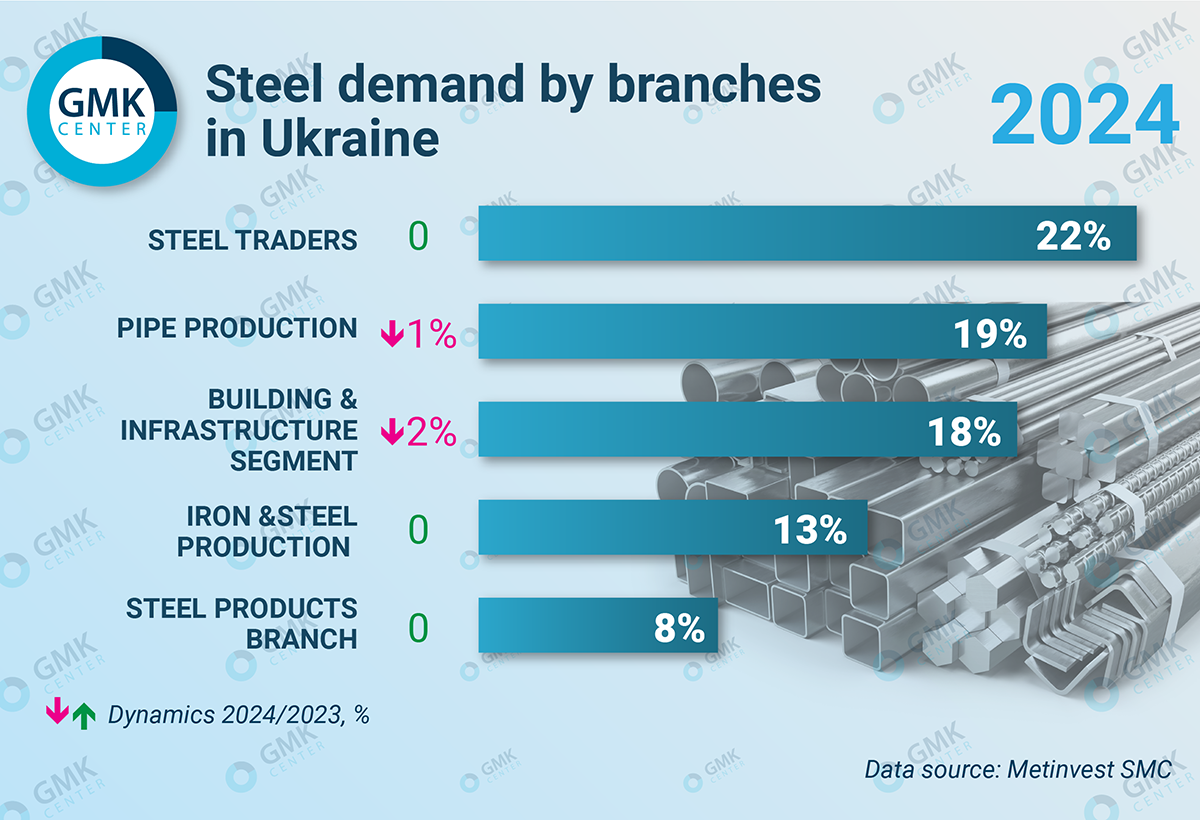

Industry structure of steel consumption

The structure of rolled steel consumption by industry fully reflects the current economic situation in the country and the dynamics of individual industries. The largest consumers in the sales structure of Metinvest-SMC by the end of 2024 are steel traders and pipe industry.

According to Metinvest-SMC estimates, the construction segment in 2023 showed a decrease in the specific weight in the structure of demand for steel to 18% against 20% in 2023. This is due to the fact that in 2024 the dynamics of reconstruction of destroyed housing and infrastructure, as well as the construction of protective structures over power facilities decreased. The slowdown in the dynamics of construction work is also evident in the capacity of the rebar segment, which grew by 5% in 2024 compared to 104% in 2023.

At the same time, a serious surge in construction activity can be seen in the western regions of the country. According to Metinvest-SMC, last year sales of steel products in Lviv increased by 45%, mainly due to rebar and galvanized rolled products.

Also, market operators note the growth of demand for steel on the part of certain segments of machine building – production of agricultural machinery and railroad cars. In particular, Metinvest-SMC observed a 76% increase in sales of steel products in Poltava region due to the activation of railcar building enterprises and mining and processing plants.

The driver of increased demand for steel products in 2023-2024 was the defense industry, which is focused on domestic defense orders. However, steel consumption in the DIC is limited to a narrow range of products and cannot replace low demand from many other sectors of the DIC economy.

“We note an increase in consumption by the defense industry, in particular, special steel grades, electro-slag and vacuum-arc remelted steels, tool steels required for processing of these alloys,” notes Igor Udovichenko, Marketing and Sales Director of TACT Metal.

A significant share in the structure of demand in the market in 2024 was occupied by mining and steel enterprises – 13%, remaining at the level of 2023. Despite a 2-fold decrease in the consumption of UHM profile, it was compensated by an increase in the consumption of grinding balls.

Steel trading market forecast

The state of the steel trading market depends entirely on the state of the economy and the level of business activity, which give little reason for optimism. In such conditions it is difficult to give forecasts, but steel traders expect sales growth of 15% on average and a slight increase in the steel consumption market.

“Demand and market dynamics may change significantly depending on how events on the front will develop, whether a ceasefire will be agreed, what will happen to energy, logistics and labor in the industry. Basically, we expect the market to grow by 6% to 3.2 million tons (excluding polymer-coated steel, stainless steel and white tinplate),” Vedernikov adds.

The first sales results for the current year show that there are good prerequisites for expecting sales growth, which gives optimism to steel trading market operators.

“The market is very much alive now. People are realizing pent-up demand: they are resuming construction projects frozen in 2022-2023. In addition, now steel is relatively cheap, the hryvnia is depreciating, which means it is a good opportunity to invest in steel, so as not to lose them due to inflation,” emphasizes Pritula.

At the same time, Ukraine has a large long-term need for the restoration and construction of new infrastructure, the consumption of steel within the framework of which will require, according to various estimates, from 3 to 5 million tons – both domestic production and imports.

-

OpinionsIndustrysteel consumption

13 July 2026

24 June 2026

18 June 2026

15 June 2026