Posts Global Market Italy 1136 29 December 2025

Steel consumption statistics reflect the depth of the problems facing the Italian economy

According to data from the Italian steel association Federacciai, demand for steel in Italy fell by 2.1% – to 26.1 million tons in 2024. This is one of the worst results on record. Since 2015, only COVID-19-stricken 2020 saw lower demand, at 23.9 million tonnes. The situation in the main steel-consuming industries suggests a further decline in steel sales in 2025 and 2026.

Macroeconomic overview

The local economic crisis has its own specific characteristics. In addition to pan-European problems, such as a sharp increase in electricity prices for industry and the associated high interest rate of the European Central Bank, Italy has another problem: huge external public debt.

In September 2025, it reached €3.08 trillion, more than 21% of the total public debt of the European Union member states. This is forcing the authorities to pursue a tight fiscal policy. The VAT (IVA) rate in Italy is 22%, and the income tax (IRPEF) rate is 23% (for annual incomes up to €28,000). This is despite some tax breaks introduced by Giorgia Meloni’s government in 2024.

In such conditions, there is no question of high purchasing power among Italian households, which are the main driver of demand for new cars and housing.

According to a report by the Rome-based Center for Social Investment Research (Censis), 70% of Italian citizens want tax cuts in 2025. At the same time:

- 45% of families have already cut back on spending;

46% can no longer save money;

44% expect the situation to worsen over the next three years;

41% of families with children receive regular assistance from retired parents.

The enormous costs of servicing the national debt reduce the possibility of investing budget funds in infrastructure development and stimulating sales of new cars and household appliances through trade-in schemes using tax incentives, as is done in China and India, the most powerful developing economies. Payments on public debt accounted for 6.8% of all Italian government budget expenditures in 2023 and will account for 7.5% in 2024.

The situation in Italy’s main steel-consuming industries should be viewed from this perspective.

Demand for flat products

Italian consumers prefer imported steel due to the significant price difference. At the end of November, quotes for locally produced thick plate were at €700/t EXW (with delivery in January 2026), while Asian offers were at €640–650 SFR. For wire rod, prices were €565–600/t EXW, compared to €505–570/t SFR from Indonesia and North Africa.

In 2024, out of 26.1 million tons of total steel sales, foreign deliveries accounted for 17 million tons, or 65%. Of these, 10 million tons, or 38.3%, came from countries outside the EU. Similar figures were recorded in previous years. In 2022, with a total market capacity of 29 million tons, imports accounted for 64.5%, in particular from outside the EU – 35.2%. This indicates the weak tariff protection of the European steel market, since foreign trade policy is the prerogative of official Brussels.

The same is true of the Italian car market. It contracted sharply in 2020 during the COVID crisis. This was followed by a slight recovery after the bottom was tested in 2022.

In 2024, passenger car production in Italy fell by 42.8% to 309,800 units, according to the Italian Automobile Manufacturers Association (ANFIA). This is one of the lowest levels in the last decade. This led to a 1.6% decline in flat steel consumption to 14.7 million tons. A new record low may be set at the end of this year.

In January-September 2025, new car sales fell slightly, by 2.9%, to 1.168 million units. At the same time, passenger car production fell by 29.9% to 179,700 units. The share of local car manufacturers in total sales was less than 15%. It is difficult for them to compete with foreign companies, primarily Chinese ones, which use cheaper steel and labor and receive tax and export subsidies from the state. Under these conditions, the basic 10% duty on car imports into the EU is not enough to support local car factories.

The machine-building industry is also in a difficult situation. In 2024, the production of machine tools and equipment fell by 11.4% to €6.75 billion, according to the industry association UCIMU. This was primarily due to a 33.5% collapse in the domestic market to €2.26 billion. A 6.3% increase in exports to €4.49 billion only slightly increased consumption of flat-rolled products, although this was a record figure.

“2024 was a completely lost year for the Italian machine tool industry, which tried unsuccessfully to save the end result through overseas activities,” said UCIMU President Riccardo Rosa.

In 2025, there was some improvement. In the first quarter, the machine tool order index increased by 8.5% compared to the previous quarter and reached 94.5 points. The domestic order index rose by 71.5% year-on-year. Given the disastrous results of the previous year, we can say that there has been some recovery in the market, but not growth.

The dependence of Italian machine tool manufacturing on exports poses risks for steel consumption. In 2025, machine-building products imported into the US will be subject to an additional 50% duty. In 2024, the US accounted for 10% of machine tool exports from Italy.

Italian manufacturers have high hopes for the government’s “Transition 5.0” program. It provides tax breaks for replacing outdated machine-building equipment with new equipment. Due to insufficient regulation of bureaucratic procedures, this tool is not working properly. In 2024, only €600 million, or 10%, of the €6.3 billion allocated to the program was used.

The situation with the production of construction equipment is similar. In 2024, sales in Italy fell by 11% to 22,000 units, according to the industry association Unacea. Exports decreased by 8% year-on-year to €2.6 billion. In the first half of 2025, domestic sales increased by 3% to 9,500 units, while exports continued to decline by 8.8% to €1.29 billion.

The weak recovery of the domestic market does not compensate for the previous decline and is combined with a deterioration in foreign trade caused by new tariff barriers. All this is reflected in a further decline in demand for flat-rolled products.

Demand for long-length rolled products

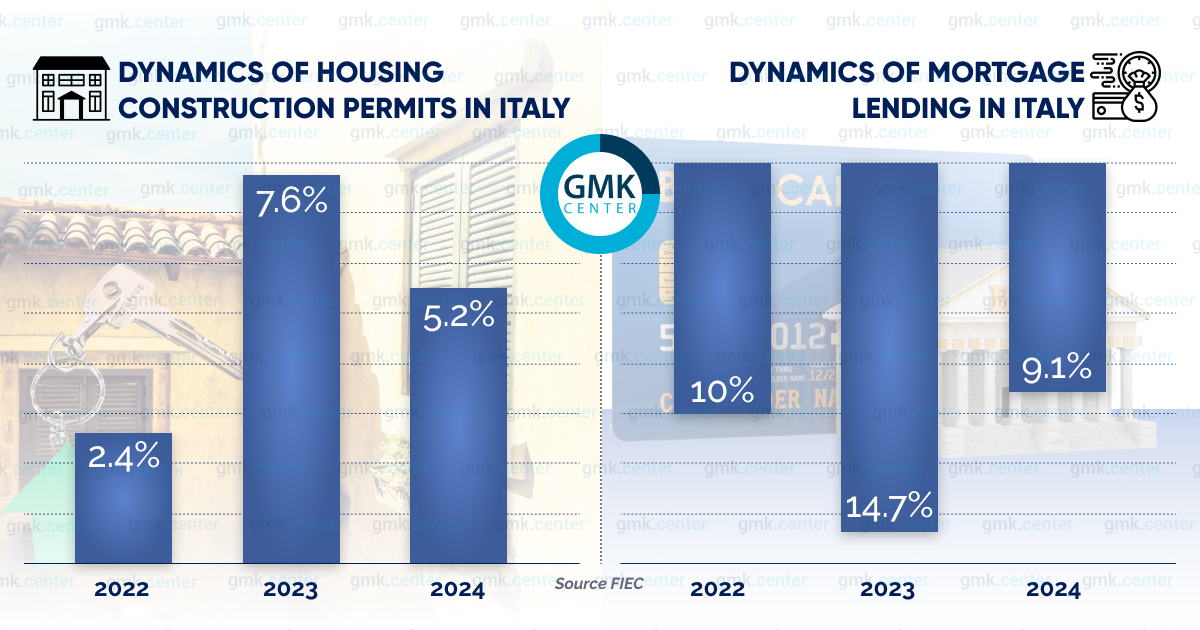

Consumption of long-length rolled products is under pressure from the crisis in the construction industry. Housing construction volumes are declining, which is reflected in a reduction in the number of permits issued for new homes. The reason for this is the deterioration in access to long-term mortgage loans.

This problem is common to all eurozone countries. From July 2022 to September 2023, the average mortgage rate in Italy rose from 1.45% to 4.5% following the European Central Bank’s interest rate hike to combat inflation. From June 2024, it began to decline, with the cost of Italian home loans falling to 3.12%.

This is more than twice the pre-crisis level. According to data from the Italian National Institute of Statistics (Istat), in the first half of 2025, the total area of new houses and buildings commissioned decreased by 11.7% year-on-year.

Infrastructure projects, in which the state plays an important role, remain the main driver of the Italian construction industry. In 2024, public investment accounted for 71.8% of Italy’s transport infrastructure construction volume.

State funding is allocated under the National Recovery and Resilience Plan (PNRR). Most often, these are regional development plans for southern Italy based on the creation of new transport infrastructure. The total amount of the PNRR is €180.45 billion. In addition, there is the European Commission’s Connecting Europe Facility program, under which Italy receives €6.5 billion per year for the modernization of pan-European transport corridors.

In 2024, motorways accounted for 49.1% of the total volume of work in the transport infrastructure construction segment in Italy. The share of railways is gradually increasing, by an average of 5.12% per year. As a result, demand for long products remained stable at 9.4 million tons in 2024, but it is unlikely that this figure will be maintained at the end of 2025.

Further forecasts

According to calculations by the National Association of Italian Builders (ANCE), investment in housing construction will decline by 25.8% in 2025. This includes a 30% decline in the renovation of existing housing stock and a 2.6% decline in new housing. Private investment in industrial and commercial construction will decline by 1.4%. This implies a decrease in the volume of work performed in 2026.

According to estimates by the international company GlobalData, the construction industry will shrink by 0.8% in real terms in 2025 due to a decrease in the number of building permits issued, and by a further 4.1% in 2026. The detailed forecast by segment is as follows:

- Commercial construction will increase by 0.4% in 2025, followed by a 1.3% decline in 2026.

- Industrial construction will increase by 0.3% in 2025 and decline by 1% in 2026.

- Infrastructure construction will increase by 5.6% in 2025, slowing to 1.5% in 2026.

- Residential construction will decline by 3.5% in 2025, worsening to 7.5% in 2026.

- Energy construction – an increase of 5.4% in 2025, slowing to 1% in 2026.

In the energy sector, wind power is the main driver of steel consumption. According to Wind Europe, Italy ranked 7th in the European Union with an installed capacity of 12.9 GW at the end of 2024.

The pace of development is quite slow. Last year’s 6% growth was achieved by commissioning 685 new wind turbines with a total capacity of 0.685 GW. Wind Europe predicts that by 2030, Italy’s wind energy capacity could reach 20.09 GW.

Growing public debt will limit the government’s ability to invest in infrastructure construction. The decision by the Italian Court of Auditors to block the previously approved government project to build the world’s largest suspension bridge, 3.3 km long, between Sicily and mainland Italy at a cost of €13.5 billion, will also have a negative impact on long-rolled steel consumption.

The outlook for demand for flat steel in 2026 is moderately pessimistic. Italian manufacturers Alfa Romeo Automobiles S.p.A. and Lancia Automobiles S.p.A., part of the Fiat Group Automobiles S.p.A., are essentially fighting for survival. There is no talk of expanding production at the car plants in Turin, Arese, and Portello.

ANFIA expects that in 2026, new car production in Italy will, at best, return to 2022–2023 levels. This is 644–734 thousand units, including trucks. At the end of 2024, the figure was 519,000 units.

The UCIMU association forecasts a return to positive growth for Italian machine tool manufacturing in 2026, but with very moderate growth of 2.9% to €6.94 billion.

The European CBA, which will come into force on January 1, 2026, may even hinder these modest expectations. According to estimates by Italian steel traders, the imposition of an additional charge for the “carbon footprint” of imported steel will lead to an increase in its cost by €60-80/t for low-emission producers. For Indian steel mills with high CO2 emissions, the price increase could be €90-300/t.

Italian steel consumers are unable to pass on the additional costs to end buyers. The decline in demand for finished rolled products may accelerate even further.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

16 June 2026

10 June 2026

27 May 2026