Posts Global Market India 1756 01 December 2025

Delays in budget financing boosted rolled steel exports

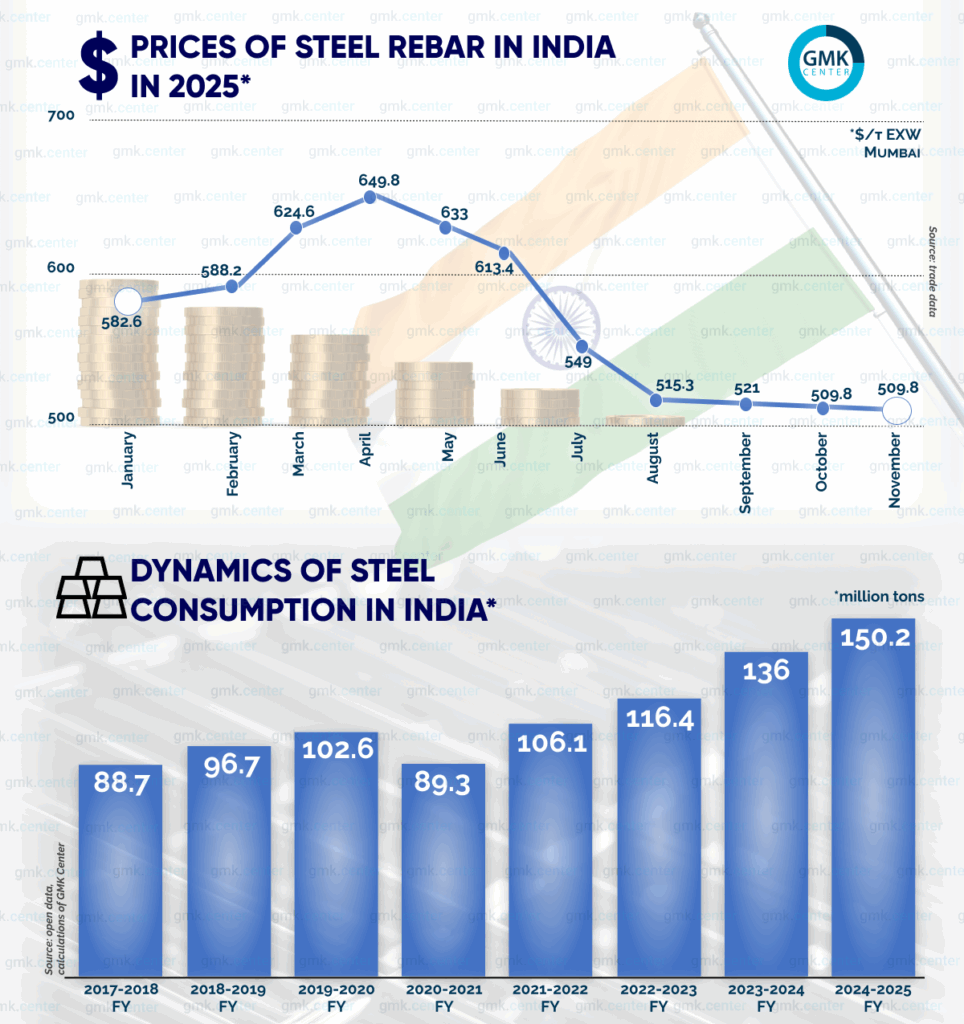

In October 2025, India regained its status as a net steel exporter for the first time in a long time. Foreign supplies increased by 44.8% year-on-year – to 640,000 tons, while imports fell by 55.6% – to 459,000 tons. The last time a positive steel trade balance was recorded was in 2023. At the same time, domestic steel consumption grew by 4.7% – to 13.6 million tons. So what is happening on the Indian steel market now?

Macroeconomic situation

In early October, the World Bank improved its forecast for India’s GDP growth in the 2025–2026 fiscal year from 6.3% to 6.5%. The adjustment was made after the release of the results for the second quarter of the fiscal year, according to which the Indian economy grew by 7.8%. This is the highest figure in the last 15 months.

At the same time, government spending increased by 7.5% and private consumption by 7%. Retail sales grew by 6.8% compared to the previous quarter. In particular, sales of everyday goods jumped by 13.9%.

The main driver was the tax reform carried out in September. As part of this reform, the tax rate on goods and services (GST, similar to VAT) was reduced for a wide range of items. In particular, the tax on cement was reduced from 28% to 18%, which significantly reduces the cost of housing and infrastructure construction and, therefore, affects their final cost.

In addition, the GST rate on commercial and small cars (with an engine capacity of up to 1.5 liters) was reduced from 28% to 18%. This stimulated demand in the automotive and construction sectors, which are the main consumers of finished steel.

Other tax innovations also indirectly contributed to growth, such as the reduction of the GST rate from 12–18% to 5% for a wide range of food products, as well as for medical and insurance services, etc. All of this ultimately led to an increase in household income.

It is also worth noting the low consumer inflation rate of 0.3% year-on-year at the end of October. The last time it was recorded at this level was in November 1999 (!). Overall, the Reserve Bank of India (RBI) forecasts inflation of 4.2% for the 2025–2026 fiscal year. Price stability has further increased the purchasing power of Indians.

Finally, on February 9, the RBI lowered its key rate by 25 basis points (bp) to 6.25%. This decision was made for the first time in the last five years. It made lending more accessible, including for the purchase of new cars and housing.

Consumption situation

Positive trends in macroeconomics have had a favorable impact on steel consumption. In October, it grew by 4.7% y/y – to 13.6 million tons. Overall, in April-October, the indicator increased by 12.53% – to 96.44 million tons. It should be noted that steady growth has been observed in recent years, except during the pandemic period.

The Indian automotive industry increased production by 4.6% – to 12.8 million units (including passenger and commercial vehicles, quad bikes, and motorcycles) in April-September, according to the Society of Indian Automobile Manufacturers (SIAM). This ensured increased demand for rolled steel.

In October, India’s auto market experienced a new surge. Sales of new passenger cars grew by 11% y/y – to 557,000 units. This was a historic record, according to the Federation of Automobile Dealers Associations (FADA).

In addition to explosive domestic demand, increased utilization of sheet rolling capacities was ensured by external sales. Exports of passenger cars in April–September grew by 18.4% – to 445,900 units, and exports of trucks grew by 26% – to 211,400 units.

The situation with demand for long-length rolled products is not so clear-cut. Its main consumer is the construction industry, in which government investment in both infrastructure and new housing plays a very important role.

For example, the Pradhan Mantri Awaas Yojana-Gramin (PMAY-G) program, funded by the Ministry of Rural Development, envisages the construction of 49.5 million houses in the country by March 2029. However, due to problems with the allocation of funds, as of April 1 of this year (i.e., at the end of the 2024–2025 fiscal year), only 13% of the plan has been implemented. It is already clear that at this rate, it will not be possible to achieve the set goals within the specified time frame.

The progress of the Pradhan Mantri Gram Sadak Yojana program, the main driver of road construction, has slowed significantly. Its funding in the current fiscal year has been reduced by 37% compared to the previous one.

The deterioration of the situation is also evidenced by a 30% year-on-year drop in October sales of construction equipment. At the end of fiscal year 2024–2025, growth slowed to 4% compared to 26% in fiscal year 2023–2024.

Indian sources, citing construction market participants, report delays in payments from the government. This applies to both state authorities and state-owned companies that are construction customers.

«Manufacturers have accumulated large stocks (of long-length rolled products – ed.), but there is simply no demand. Even infrastructure projects are not absorbing the required volumes. Unfinished approvals, delays in the allocation of funds, and cash flow problems for contractors caused by previous delays are holding back the implementation of projects,» said a Mumbai-based steel trader in a comment to Kallanish in the first half of October.

These stocks are forcing Indian steel companies, first, to lower prices.

Second, to send more and more products for export. Overall, exports grew by 25.3% in April–October, to 3.45 million tons, including a 44.8% year-on-year increase in October, to 640,000 tons. Two-thirds of these exports were long products.

All this creates additional tension in the markets of the European Union, the Persian Gulf countries, and some countries in Southeast Asia, particularly Vietnam. These are the main destinations for Indian steelmakers’ foreign sales.

Further forecasts for steel demand in India

The sharp decline in GST revenues as a result of tax reform poses risks to the implementation of federal and regional budgets. Therefore, it can be assumed that it will be difficult to quickly restore payment discipline. This means that Indian construction companies will continue to have problems financing work under government programs, and demand for long products will therefore remain volatile.

At the same time, the high share of the construction industry in national GDP should be taken into account – 9.2% at the end of the 2024–2025 fiscal year. Therefore, it seems logical that the Asian Development Bank downgraded its forecast for Indian economic growth in fiscal year 2025–2026 from 7% to 6.5% in September. Consulting firm Deloitte expects a slowdown to 6.5–6.9% in the next fiscal year compared to 6.7–6.9% in the current one (base forecast).

The government has more optimistic expectations. At the end of September, Steel Secretary Sandeep Pundarik said that steel consumption in fiscal year 2025–2026 would increase by 9–10%. According to estimates by the Indian rating agency ICRA, it will increase by 7–8%.

The automotive industry will remain the main driver of demand for flat steel. Moody’s forecasts a 5% increase in new car sales in India in 2025 and another 5% in 2026. The previous forecast for next year predicted a slowdown in growth to 2.5%. Moody’s explains the improvement in the forecast by the impact of tax reform.

ICRA provides similar estimates. It forecasts a 3-5% increase in sales of passenger and commercial vehicles in the 2026-2027 financial year. Passenger car sales will amount to 6-6.5 million units.

Demand for thick-gauge steel will grow thanks to an ambitious shipbuilding development program. It envisages increasing India’s share in the global shipbuilding industry to 5-7% by 2030, compared to the current figure of 1%. In this regard, there are plans to build new shipyards and modernize and expand existing ones.

According to the government’s plans, eight shipbuilding clusters will be created. Five of them will be new sites in the states of Andhra Pradesh, Odisha, Tamil Nadu, Gujarat, and Maharashtra. Another three will be based on existing facilities in Vadinar, Kandla (Gujarat), and Kochi (Kerala).

Despite volatility, demand for long-length rolled products remains strong, with good prospects. Despite the slowdown in the implementation of local projects, Irish research company Research&Markets expects the Indian construction industry to grow by 7.1% in real terms in 2025. In 2026–2029, it is expected to grow by an average of 6.1%.

As noted, this forecast carries significant risks. However, there are also reasons for optimism: numerous government programs that support demand for steel.

- In August, the federal government allocated $3.1 billion for the development of 128 km of railways in Delhi, including the 65 km Delhi–Dehradun line and the 17 km Delhi–Tronik City line. In total, the federal budget for the 2025–2026 fiscal year allocates $603 billion to the transport sector. Of this, $34.5 billion goes to the Ministry of Road Transport and Highways and $30.9 billion to the Ministry of Railways.

- In July, the Maharashtra state government approved the $8.43 billion My Home My Right program, which provides for the construction of 3.5 million affordable housing units by 2030. In addition, in August, the authorities signed an agreement with Singapore’s CapitaLand. The company has committed to investing $2.3 billion in the construction of industrial parks, data centers, and logistics complexes in Maharashtra by 2030.

- In June, the state-owned National Thermal Power Corporation (NTPC) announced plans to build new hydropower plants with a total capacity of 20 GW. Of these, 3–5 GW are to be completed by 2032.

- In July, the federal government signed agreements with private companies to build four pumped storage power plants with a total capacity of 6.5 GW. The cost of the projects is $3.8 billion.

- In April, the Ministry of Energy announced plans to expand nuclear power capacity from 8.9 GW in 2024 to 100 GW by 2047. Eight reactors with a total capacity of 6.6 GW are currently under construction.

The implementation of these large-scale investment plans will drive the construction industry and, as a result, demand for long-length rolled products. This will be the case in 2026 and in the years to come.

Impact on foreign markets

India’s steel production capacity has already reached 205 million tons in the current fiscal year, according to estimates by BigMint. The government has very ambitious plans for the further development of the industry. By 2030, it should reach 300 million tons, and by 2047, 500 million tons.

Such plans seem logical given the large-scale long-term programs in the field of transport infrastructure, commercial, industrial, and residential construction, and the expansion of production and energy capacity, which should create and maintain sustainable demand for steel in the domestic market.

However, government funding cannot be a reliable and stable factor in steel demand. Even minor changes related to reforms can negatively affect domestic steel demand. As events in recent months have shown, this leads to a sharp increase in Indian steel exports.

Already, with local steelmakers having 205 million tons of capacity, the impact of additional volumes is beginning to be felt in foreign markets, particularly in the European Union and the Persian Gulf countries. But what will happen when productivity reaches 300 million tons and domestic demand is unstable due to a lack of government funding or macroeconomic problems?

Currently, the oversupply in global steel trade is primarily driven by China amid declining domestic consumption. India may become the next factor in the volatility of global steel prices.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

23 July 2026

22 July 2026

17 July 2026