Posts Infrastructure electricity prices 8118 12 August 2024

In Ukraine, the weighted average price for solar power in July was €134.4 MWh, which is higher than in other European countries

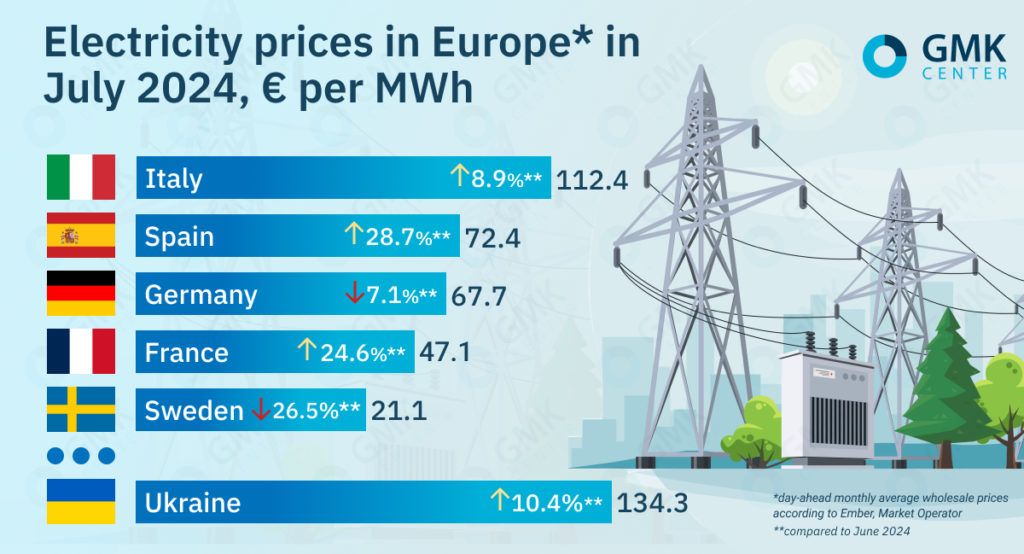

In the EU, the average monthly wholesale prices for the day ahead in July 2024 showed a mixed trend.

According to Ember, they were:

- Italy – €112.37/MWh (+8.9% m/m);

- France – €47.09/MWh (+24.6%);

- Germany – €67.7/MWh (-7.1%);

- Spain – €72.4/MWh (+28.7%);

- Sweden – €21.1/MWh (-26.5%).

In July, according to AleaSoft Energy Forecasting, prices on the electricity markets of Spain, France and Italy increased compared to June. This was due to higher temperatures, which caused an increase in demand. In addition, the situation was affected by decreasing wind generation in most markets. In north countries of the continent, the increase in temperature and demand was less pronounced, and prices there fell in line with lower gas costs and carbon emissions.

The situation in Ukraine

In Ukraine, in July 2024, the average weighted price of purchase and sale of electricity on the DAM (day-ahead market), according to the “Market Operator“, increased by 10.4% m/m – up to 5,967.11 UAH/MWh (about €134.4/MWh – at the rate of 44.41 UAH/euro on July 31), and was higher than in other European countries.

Demand on the day-ahead market in the specified period compared to June decreased by 9%, and supply fell by 5.26%.

In July 2024, Ukraine reduced electricity imports by 2% compared to June, to 837.8 thousand MWh. Its largest share fell on Hungary (45%), followed by Poland (19%) and Romania (18%).

According to the analysis of D.Trading, a slight decrease in imports in July compared to the previous month occurred due to the increase in electricity prices on the markets of neighboring countries and an increase in electricity consumption in Europe, which was caused by the heat. Due to weather conditions, prices in Europe began to rise rapidly in the second week of July.

In addition, the volume of available crossing last month decreased compared to June. Thus, from July 10 to July 21, due to abnormal heat, electricity imports from Moldova were temporarily suspended, and from July 22 to July 24, repair work was carried out on the interstate power transmission infrastructure on the border with Slovakia.

Last month, Ukrainian business and experts opposed the unification of the tariff for the electricity distribution. The regulator – the National Commission for State Regulation of Energy and Utilities (NEURC) – intended to consider the possibility of abolishing the division into classes of consumers (currently there are two of them in Ukraine).

In particular, the association of enterprises Ukrmetalurgprom indicated that such a decision could have serious negative consequences for the iron and steel enterprises and the economy as a whole. Major players in the industry noted that this is not economically justified and contrary to European practice.

In the end, the National Energy and Utilities Regulatory Commission refused to unify tariffs for the distribution of electricity. The decision was considered at a meeting of the regulator on July 17 and was not approved. In addition, it was proposed to start preparing regulatory documents for the transition to three voltage classes in accordance with European practice.

European companies

In July, the French energy company EDF announced that, together with Italian steelmakers, it was considering joint investments in nuclear energy. EDF has signed an agreement with Italian subsidiary Edison, equipment manufacturers Ansaldo Energia and Ansaldo Nucleare, and Italian steel industry association Federacciai to explore joint investment opportunities in the sector.

The memorandum of understanding provides for the promotion of cooperation in the use of nuclear energy to increase the competitiveness and decarbonization of Italian steel industry. The signatories of the agreement, in particular, pledged to consider joint investment in the construction of small modular reactors (SMR) in Italy over the next decade.

Voestalpine, an Austrian technology group, summing up the first quarter of fiscal 2024/2025, noted the lack of support from the country’s government in covering rising electricity costs.

The company drew attention to the fact that the Austrian government stopped paying compensation for high electricity costs for energy-intensive industries. In 2022, this assistance amounted to €50 million, Kallanish reported, citing Voestalpine CEO Herbert Eibensteiner.

Eibensteiner notes that energy costs undermine the competitiveness of Austrian producers in the international market. He explained that the governments of all European countries, with the exception of Sweden and Austria, provide such benefits to their industries. High energy costs for the company will increase more during the energy transition, as it intends to replace two blast furnaces at its facilities with DRI/EAF units by 2027.

In addition, a specific factor for Austria is the obligation to use biogas in industrial production.

In February of this year, the Council of Ministers of the country presented the «law on renewable gas,» which was submitted for consideration and approval to the next chamber. It will regulate the use of local biogas in the energy balance, and envisages that 7.5 TWh per year by 2030 will be produced from domestic sources (more than a 50-fold increase compared to current levels). Gas suppliers will have to offer customers almost 10% of their volumes from renewable sources. Eibensteiner believes that this law is likely to be adopted, and this will mean that the company will have to consider biogas in its mix.

Fullness of gas storages

According to the AGSI platform, European gas storage facilities as of August 1, 2024, were more than 85.2% full. This exceeds the 5-year average of 78%.

In July, European gas prices failed to reach June highs. However, geopolitical factors continue to influence the situation in the EU gas market.

So, on August 1, TTF estimated futures for the month ahead rose to €36.9/MWh (which is high for the summer) amid fears of a possible escalation of the war in the Middle East. The sharp increase in gas prices since August 6 is associated with hostilities in the Kursk region of the Russian Federation and concern about possible interruptions in the supply of Russian fuel through Ukraine. On August 8, they rose to €40.10/MWh.

The Sudzha border gas station is part of the last route of the Russian pipeline to Europe via Ukraine. Bloomberg notes, although Europe has reduced its dependence on Russian pipeline gas since the 2022 crisis, some countries, such as Slovakia and Austria, still depend on these supplies, making them vulnerable to sudden disruptions.

«The price of the TTF contract rose to around €40 at the beginning of August, which is the highest since the end of last year. The market is reacting to a possible escalation in the Middle East and the course of hostilities between the Russian Federation and Ukraine. The same reaction was in the 4th quarter of 2023, but the highs of €55 in October 2023 are still a long way off,» notes GMK Center chief analyst Andriy Tarasenko.

He adds that the balance of gas supplies to the EU remains very delicate and there is a lot of uncertainty.

«Despite more than average gas storage filling, in the event of a major war in the Middle East, energy prices will rise significantly, which will cause a spike in electricity prices in the EU and in Ukraine as well,» explained Andriy Tarasenko.

As Bloomberg notes, the summer of the current year for the gas market in Europe is generally unstable. Heat waves in parts of Asia and Europe have boosted demand and intensified competition for LNG cargoes. In addition, some of the world’s major manufacturers have also experienced capacity disruptions due to technical reasons or extreme weather conditions.

Norway, the leading European supplier, is about to enter an intensive maintenance period in August and September. According to ICIS, planned and unplanned outages of gas infrastructure in this country will significantly affect the supply of gas to Europe.

It is predicted that the daily capacity reduction in Norway will exceed 130 cubic meters by the end of August compared to less than 20 million cubic meters per day during the last week of July. A significant reduction in supply can lead to price volatility and market uncertainty.

At the same time, Dutch financial group ING revised its forecast for gas prices in Europe for TTF in the third quarter, noting that it will average €30/MWh (previously €25/MWh). The updated expectations are due to slower-than-expected growth in EU gas stocks in July-early August, lower LNG inflows, lingering supply risks and healthy speculative interest in gas.

-

OpinionsInfrastructuresteel consumption

13 July 2026

18 March 2026

29 January 2026

20 January 2026