Posts Global Market electricity prices 12953 09 July 2024

European steelmakers call for paying attention to electricity prices, Ukrainian steel sector proposes to reduce the share of electricity imports which is needed to ensure stable energy supply to 50%

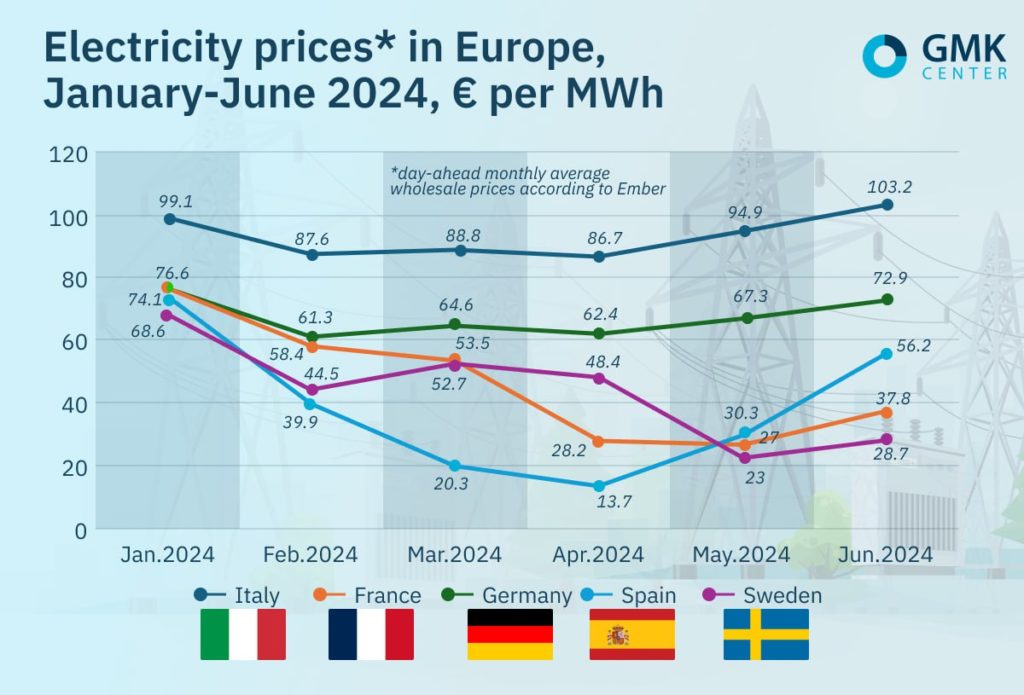

In the EU, average monthly wholesale day-ahead prices in June 2024 increased significantly compared to May.

According to Ember, they were:

- Italy – €103.2/MWh (+8.7% m/m);

- France – €37.8/MWh (+39.4%);

- Germany – €72.9/MWh (+8.3%);

- Spain – €56.2/MWh (+ 85.5%);

- Sweden – €28.7/MWh (+24.7%).

The reasons for the increase in prices were growth in demand in the second half of the month due to rising average temperatures, a drop in wind generation and instability of solar one during the month, fluctuations in gas prices and CO2 emissions.

At the same time, as noted in AleaSoft Energy Forecasting, in the first half of this year, the price of electricity fell compared to the second half of 2023 in most European markets. For almost all of them, the average price has been the lowest since the first or second half of 2021. The semi-annual production of solar energy was the highest in history in all markets, wind energy also reached this milestone in some cases.

«By the end of the year in Europe is expected seasonal rise in price of electricity, judging by the curve of forwards. For example, in Germany, price growth by the end of 2024 can be up to 15%. In general, the situation in the European energy market is very volatile due to the delicate balance of the gas market. But Europe is ready for this, unlike Ukraine,» said Andriy Tarasenko, chief analyst at GMK Center.

Situation in Ukraine

In Ukraine, the weighted average purchase and sale price of electricity on the day-ahead market (DAM), according to the «Market Operator,» in June this year increased by 27.9% m/m, amounting to 5403.38 UAH/MWh (€124.9/MWh at the rate of 43.26 UAH/euro), which is almost 16% more than the maximum average price in the EU in the same period.

According to Energy Map, in June Ukraine imported 858.4 thousand MWh of electricity, which is 6% more than was purchased for the entire 2023 (806.4 thousand MWh). In addition, this is the largest monthly volume of imports over the past 10 years. Compared to May, imports almost doubled, with June 2023 – almost twenty times. The largest amount of electricity last month was imported from Hungary.

In early July, representatives of large Ukrainian iron and steel companies called on the government to reconsider the decision to increase the share of electricity imports for stable energy supply of enterprises to 80%.

The business considers 50% as a compromise solution, otherwise the high price of imported electricity will lead to a reduction in production, since the electricity cost is a significant share of the production costs. The Ministry of Energy, in turn, declares the impossibility of such a step due to a significant shortage in the energy system, and offers businesses to build their own generation.

«The need to import electricity in Ukraine has led to the fact that local prices are higher than European ones. More than 90% of steel in the EU is produced in countries that have an advantage in energy prices compared to Ukraine. The energy-intensive domestic economy can suffer colossal losses. The past crisis allowed Europeans to create mechanisms for subsidizing electricity prices. In 2022, the EU spent €25 billion on compensation for price increases for industrial enterprises, in addition, €69 billion was cross-sectoral, meaning that part of these funds could also be directed to industry. And these launched mechanisms have a medium-term nature, that is, they will continue to operate in 2024-2025,» Andriy Tarasenko notes.

Europe

An illustrative case demonstrating the vulnerability of the energy market happened in Germany last month. A computer glitch on June 25 led to a 3000% jump in electricity prices on European energy exchange Epex Spot. As a result, in the morning of this day in one hour in Germany, they jumped to €2325/MWh compared to a long-term average of about €50 for this time of day. The exchange in its message referred to «technical problems.»

As Bloomberg columnist Javier Blas noted, Epex Spot eventually applied its rules by launching a partial separation procedure – national auctions. As a result, countries that usually rely on imports, in particular Germany, suffered from sky-high prices, and exporters, including France, faced oversaturation and low prices.

Because of this situation, German companies using day-ahead prices paid an average of almost €500/MWh. However, there were other examples. So, the German reinforcement plant Feralpi Stahl temporarily suspended work. The damage from daily downtime at the enterprise was estimated at a six-figure amount, but continuing to work would mean losses in a seven-figure amount.

A day later, when the European electricity market “connected” again, prices fell to about €60/MWh.

Industry calls

In June-July, several European steel associations again commented electricity prices for industry and the impact of this factor on the competitiveness of the sector.

Associations of Italian steel producers Federacciai and casters Assofond pointed to a significant difference in energy prices between Italy and the rest of Europe. The heads of these industry organizations called on the authorities to accelerate the implementation of measures aimed at reducing gas and electricity prices in Italy and bringing the cost of energy in line with other European countries. In particular, the head of Federacciai, Antonio Gozzi, noted that a national «energy release» scheme was postponed that could support energy-intensive industries.

The cost of electricity also became one of the topics at the meeting of the Spanish Union of Steel Companies (Unesid). The Association has long drawn the attention of the authorities to the high energy costs in the production of steel in Spain, which are almost twice as high as in other EU countries, such as France or Germany. Unesid made a proposal to the government to compensate for additional electricity costs arising from emissions trading, due to 25% of the proceeds from auctions for the sale of quotas, as provided for by European legislation.

In early July, the British UK Steel also called on the new government to solve the problem of high energy costs for industry. As noted in the Association, new data showed that the wholesale price of electricity in the UK in the last three months more than double the price in France and Spain. It is expected that with the transition to EAF, electricity consumption in the sector will approximately double, which will make its price a priority issue.

Renewable energy

Last month, a number of organisations representing energy-intensive industries stressed in a joint statement that the EU must accelerate wind energy deployment to ensure the survival of the bloc’s industrial base. The signatories of the statement are WindEurope, the European Steel Association (EUROFER), the European Metals Association (Eurometaux), the European Chemical Industry Council (Cefic) and Cembureau, representing the cement industry.

At the same time, in early July, the WindEurope industry association reported that currently more than 500 GW of potential wind power capacity in France, Germany, Italy, Spain, Poland, Romania, Ireland, Croatia and the UK are awaiting evaluation of their application for connection to the power grid.

The association noted that gaining access to the network is now the biggest obstacle to the expansion of renewable energy in Europe.

European power grids are being upgraded too slowly, and due to sluggish and imperfect permit procedures in many countries, some projects are waiting up to nine years for this.

In turn, the surge in solar energy production in Europe has hit prices, outlining storage needs.

According to the Eurelectric Industrial Association, in January-June this year, 74% of electricity in the EU was produced using sources without carbon emissions (50% by solar and wind power plants, 24% by nuclear power plants).

Fullness of gas storages

According to the AGSI platform, as of July 1 of this year, the filling of gas storage facilities in the EU averaged 77.6%.

According to a June report by Wood Mackenzie, European gas storage facilities will reach 100% by the end of September and will remain full until the end of October. In addition, an additional 4 million tons/year will be accumulated in floating storage facilities.

According to Lucy Cullen, Director of Gas and LNG Research in the EMEA Wood Mackenzie region, lower demand in Europe led to lower prices and LNG began to flow to Asia, where imports to China alone grew by 22%. High prices are likely to hamper demand growth in Asia in the near term. As a result, European storage will be fully filled by the end of September and will remain at this level until end of October.

The report notes that a return to normal weather patterns in the winter of 2024/2025 and an improved macroeconomic outlook will boost heating needs, industrial activity and electricity demand across Europe. In general, gas demand is projected to increase by 7 billion cubic meters in 2025 compared to 2024.

The biggest risks for supplies, according to the Wood Mackenzie report, are related to Russian gas – whether due to the early termination of its transportation through Ukraine or the result of ongoing arbitration proceedings between European energy companies and Gazprom. Unplanned or long-term maintenance in Norway will play a more significant role, as this country is now the largest gas supplier in Europe. In addition, an important question remains how quickly new North American LNG supplies will reach the market.

Christian Signoretto, president of the European Gas Association Eurogas, writes Montel, expressed the view that competition between Europe and Asia for LNG supplies and ongoing geopolitical uncertainty will maintain gas price volatility until at least 2026-2027. Around this period, new LNG reserves will enter the market, in particular from Qatar and the United States, so the industry organization expects a more balanced market with less price volatility. According to Signoretto’s forecast, in the second half of this year, gas prices will fluctuate at the level of about €30-35/MWh.

-

02 July 2026

16 June 2026

10 June 2026

27 May 2026