News Green steel CBAM 3656 20 September 2023

EAF steelmakers will gain cost advantages behind BF-BOF

Introduction of CBAM will lead to increase of carbon costs by €146 for imported BF-BOF products. In longs segment it gives ability to domestic EAF producers to substitute BF-BOF imports, according to the GMK Center report «CBAM impact on iron and steel exports from Ukraine».

In the EU 85% of longs capacities are EAF-based and were only about 59% utilized in 2022. So, domestic EAF steelmakers will gain significant cost advantages and have enough free capacities to increase supply. So, producers of imported long BF-BOF products will not be able to transfer CBAM-related costs onto steel price.

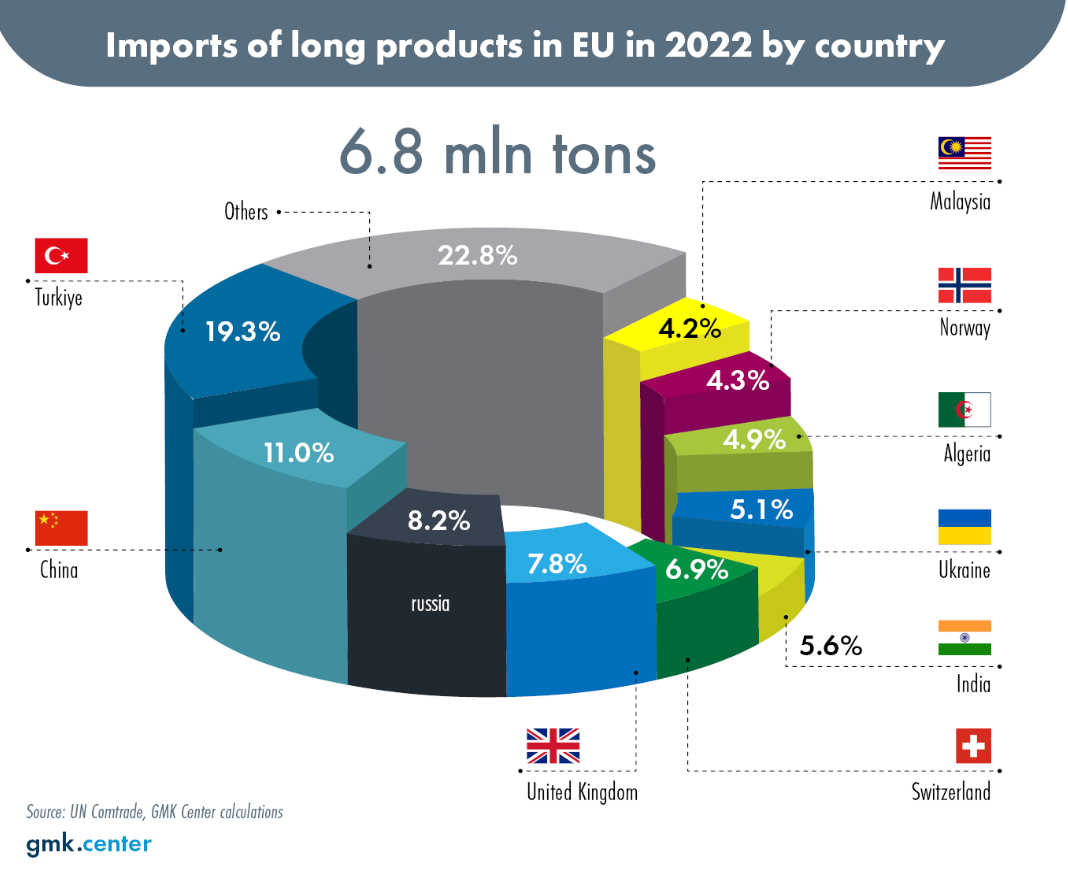

The EU imported about 4 mln tons of long products produced via BF-BOF route in 2022, according to the 58% share of BF-BOF route in the longs capacities structure in countries of imports origin. So, EAF producers in the EU could easily increase long products output by 3-4 mln tons and substitute BF-BOF imports.

European longs producers could be main benefiters of CBAM introduction. EAF producers of imported longs will be limited in their ability to increase supply to the EU, if the safeguard quotas system will be in force in 2030, that`s the GMK Center`s basic assumption.

CBAM also brings changes to square billet segment. But the challenge here is that BF-BOF square billet imports mainly represented by intragroup supplies. Re-rollers should find new sources of billet supply if they buy BF-BOF produced billet.

As GMK Center reported earlier, The impact of CBAM on the iron and steel market of the EU will differ by segment. For example, in the segment of flats, steelmakers will be able to transfer carbon costs to the end price.

-

Opinions Industry steel consumption

13 July 2026

14 July 2026

06 July 2026

17 May 2026