News Green steel flat & long steel prices 4426 18 September 2023

Steelmakers could be able to transfer carbon costs onto end customer

The impact of CBAM on the iron and steel market of the EU will differ by segment. For example, in the segment of flats, steelmakers will be able to transfer carbon costs to the end price, according to the GMK Center report «CBAM impact on iron and steel exports from Ukraine».

The introduction of CBAM will lead to increased carbon costs for both importers and European steel producers. It is obvious that the introduction of CBAM will benefit EAF producers, that have up to 4 times lower carbon intensity. Therefore, the steelmaking capacity structure, namely the ability of EAF producers to increase supply to the market, will determine the impact of CBAM.

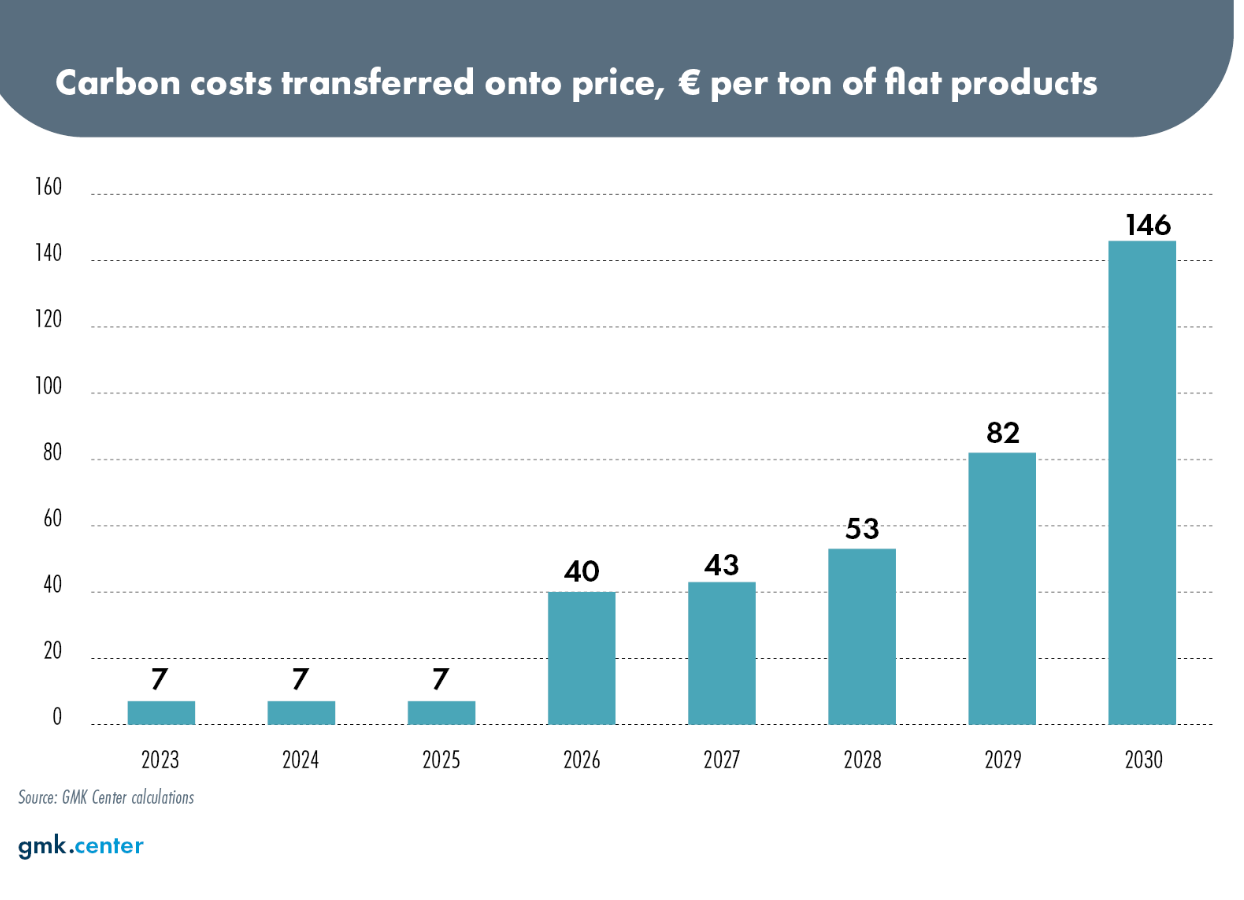

Carbon costs for importers will increase by €146 per ton of steel in 2030, according to GMK Center calculations. Carbon costs will also increase for European producers from €7 per ton of steel on average in 2022 to €96 per ton of steel in 2030, due to the reduction of free allocations and the increase in carbon prices on the EU ETS. So, carbon costs will increase for almost all players on the market. It creates the prerequisites for transferring carbon costs to the price, i.e. to the end customer.

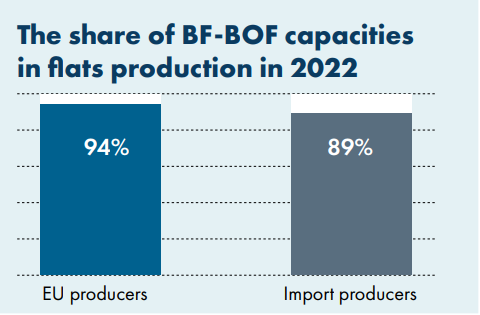

A feature of the flat rolled segment in the EU is the dominant share of BF-BOF in supply – 94% for domestic production and 90% for imports. Therefore, EAF producers will not be able to increase the supply and influence the market. So, flats producers will have the opportunity to transfer the increase in carbon costs to the end customer, who won`t have an alternative, but accept elevated prices.

Therefore, GMK Center suggests that prices in the EU flat segment could increase by €146 due to CBAM, that would offset the increase in carbon costs for importers. By the way, a similar situation was observed in the energy segment in the EU. Refusal of free allocations for power generation led to an increase in electricity prices. The European Commission even introduced a mechanism for offsetting indirect carbon costs when purchasing electricity, which is very popular in the EU.

Highly likely that the development of projects for the production of low-carbon steel in the EU to have limited impact on market supply, in other words on the ability of transferring carbon costs onto the price.

In fact, in the EU we see a boom in announcements of decarbonization projects. The most of these projects based on the DRI-EAF route, that could reduce carbon intensity of up to 0.8 t of CO2 per ton of steel and can reach 0.2 t when using hydrogen (up to 80% in a mix with natural gas ) or in tandem with CCU/CCUS.

Most of the announced projects are projects of large companies, that have announced the decommissioning of blast furnaces upon the introduction of new DRI-EAF facilities. So, its a substitution model. And such a model should not lead to a change in market supply.

But there is one exception. There are new independent players on the market. Startups. These are H2 Green Steel and BlastrGreen Steel projects. And these are large-scale projects. If they are introduced in accordance with the announcements, then this is up to 9 million tons of flat rolled products per year by 2030. Its about 10% of the European flat market.

If the consumption of steel in the EU will remain unchanged for the next 5-7 years, then the increase in the supply of low-carbon products from new entrants will deprive traditional market players of the possibility of transferring carbon costs to the price.

That’s the issue of €146 per ton increases the price level. Big market players understand this well. In this case, new entrants will be very attractive objects for M&A by large European iron and steel companies, as it is a matter of control over supply and prices.

Therefore, GMK Center`s basic idea is that by 2030, CBAM won`t have an impact on the competitiveness of players in the flats segment.

As GMK Center reported, Ukraine could lose 1.4 mln tons of merchant pig iron export to the EU and 1.6 mln tons of long product and square billet annually till 2030 as the result of CBAM introduction.

-

Opinions Industry steel consumption

13 July 2026

14 July 2026

06 July 2026

17 May 2026