Infographics DRI 646 17 March 2026

The main suppliers include Russia, Venezuela, and the United States

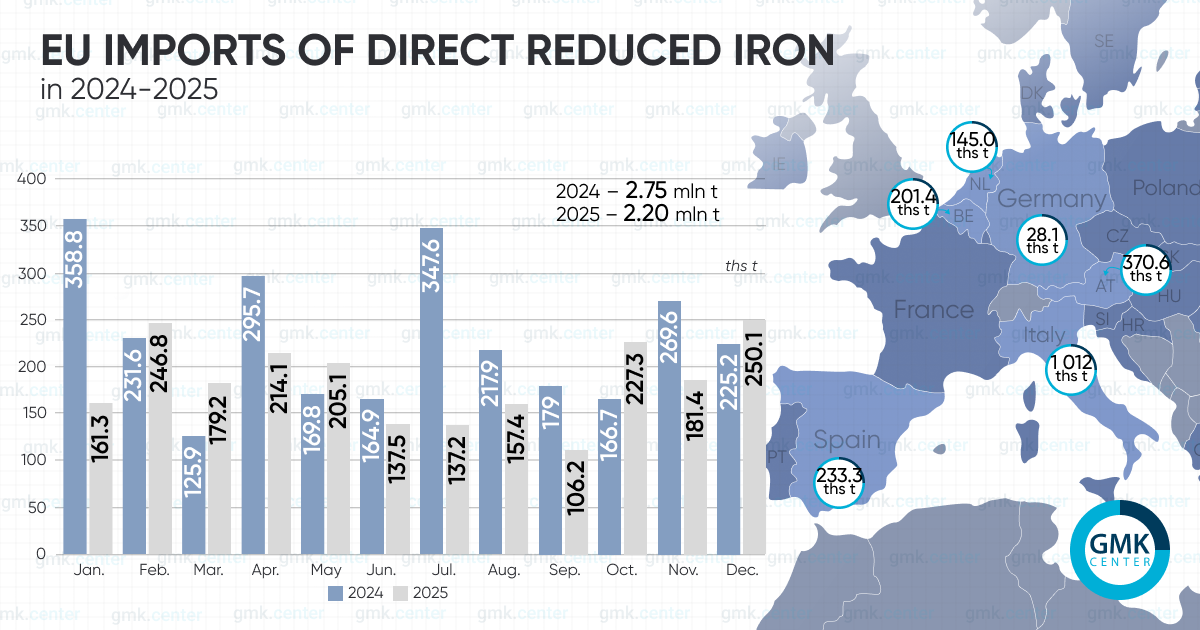

In 2025, EU steelmakers had reduced imports of direct reduced iron (DRI) by 20% compared to the previous year, down to 2.203 million tons. In 2024, this figure increased by 16.9% y/y. This is evidenced by calculations from the GMK Center based on Eurostat data.

Venezuela became the main supplier of raw materials last year, more than doubling its exports to the EU to 593,850 tons. In 2023–2024, these volumes ranged from 130,000 to 300,000 tons. This surge is attributed to rising demand from Italy, which increased its imports of Venezuelan DRI by 4.2 times year-over-year, to 477,680 tons. Another 115,450 metric tons were shipped to the Netherlands (-20.7% year-over-year), 27,300 metric tons to Belgium (no shipments were made in 2024), and 16,400 metric tons to Spain (+3-fold).

A significant share of imports traditionally comes from Russia, although in 2025 volumes fell by 44% y/y – from 1.04 million tons to 584,650 tons. Russian producers supplied 312,140 tons of DRI to Italy (-36% year-on-year), 135,270 tons to Belgium (-34.7% y/y), and 82,200 tons to Spain (-26.7% y/y).

Last year, the United States shipped nearly 500,000 metric tons of direct-reduced iron to the EU, increasing shipments by 34.1% compared to 2024. These volumes were distributed between Austria and Italy – 370,600 tons (+34% y/y) and 97,770 tons (0 tons a year earlier).

Another 328,220 tons of raw materials were imported from Libya (-31% y/y). Of this amount, 125,230 tons were shipped to Italy (+114% y/y), 60,510 tons to France (+64.6% y/y), and 47,520 tons to Spain (-35.6% y/y).

The largest importers of DRI in 2025 were Italy – 1.01 million tons, increasing volumes by 53.5% year-over-year, Austria – 370,600 tons (+34% y/y), Spain – 233,290 tons (-5.6% y/y), and Belgium – 201,360 tons (-15.6% y/y).

The trend in DRI imports into the European Union in 2024–2025 largely reflects both a shift in supply channels and weak conditions in the European steel market. The growth in 2024 was partly due to larger available volumes of Russian DRI/HBI within the EU’s transitional quotas: as of 2024, these stood at 1.14 million tons, while for 2025 they were reduced to 651,900 tons. Last year, imports declined amid weak demand for steel in the European Union, where real consumption fell for the third consecutive year, and steel production dropped to 126.2 million tons.

Despite this, the structure of supplies continued to change: the EU increasingly replaced Russian volumes with supplies from Venezuela, the U.S., and Libya. Full replacement has not yet occurred, as even in 2025, Russia remained one of the largest suppliers of DRI to the EU market. As of 2026, imports of Russian DRI/HBI have been completely halted, so the European market’s shift toward alternative suppliers is only expected to intensify.

-

Opinions Industry steel consumption

13 July 2026

06 July 2026

01 July 2026

22 June 2026