Infographics iron ore 9802 27 March 2025

Australia has traditionally been a key supplier of raw materials

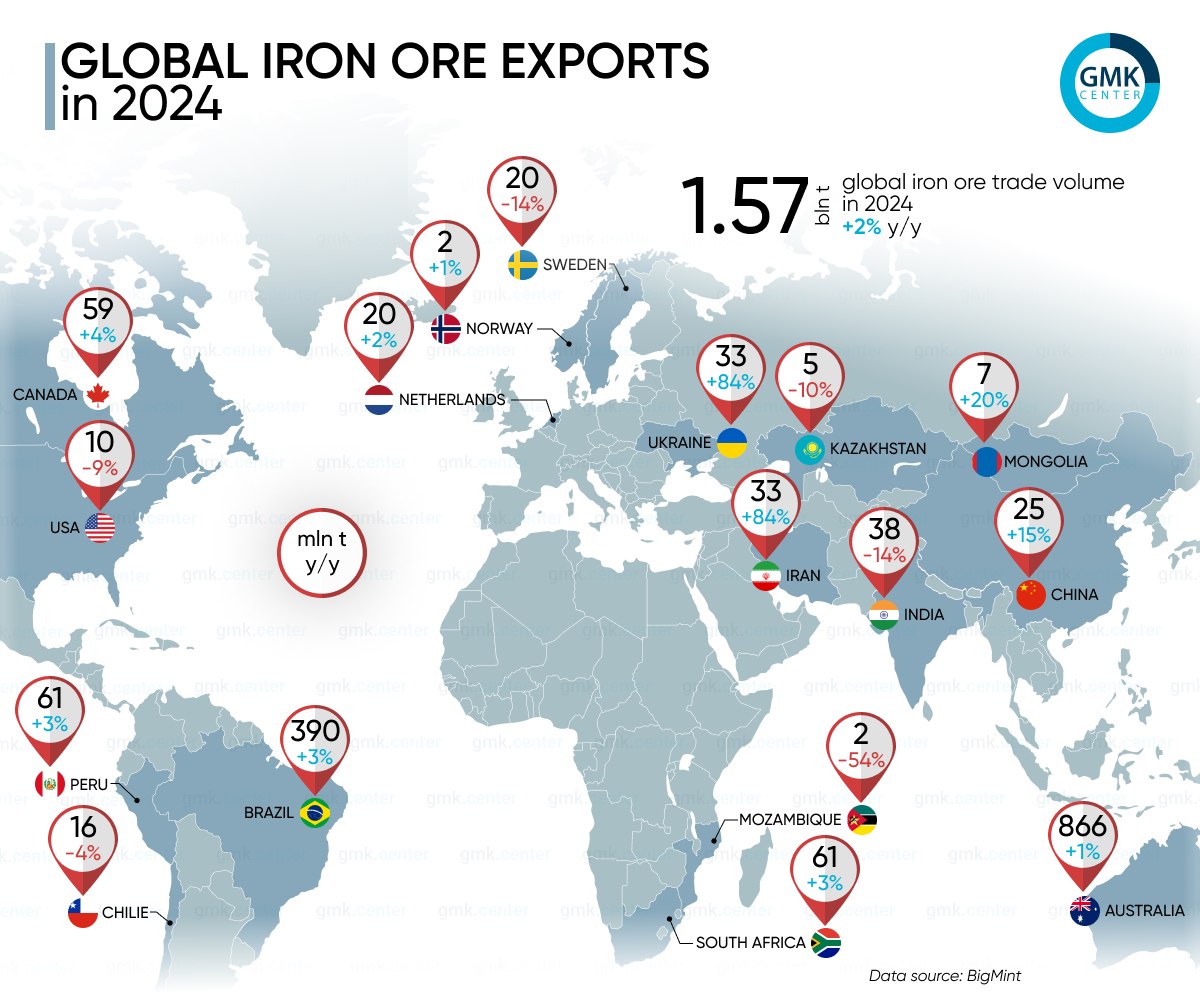

Global iron ore exports in 2024 increased by 2% compared to 2023, from 1.57 billion tons – to 1.6 billion tons. The growth rate of supplies slowed down after +5% in 2023.

Australia traditionally remains the main supplier, accounting for more than half of all global supplies:

- Australia – 866 million tons (+1.4% y/y);

- Brazil – 390 million tons (+2.6%);

- South Africa – 61 million tons (+3.4%);

- India – 38 million tons (-14%).

China, the world’s largest importer of iron ore, increased its purchases of raw materials by 5% y/y last year, reaching 1.237 billion tons. Among the key drivers:

- Positive macroeconomic developments in the second half of the year, including stimulus measures for construction and manufacturing.

- The US Federal Reserve’s rate cuts, which helped improve the global economic environment.

- Relatively stable steel production in the country – 1.005 billion tons (-1.7% y/y).

- Increase in iron ore stocks at Chinese ports to 143 million tons (+16% y/y).

Favorable iron ore prices.

Most global mining companies increased their iron ore production last year, including BHP (Australia) by 3% y/y – to 290 million tons, Rio Tinto (Australia) by 4% to 290 million tons, Fortescue Metals Group (Australia) by 2% to 194 million tons, Vale (Brazil) by 2% to 328 million tons, a record level since 2018. India’s ore production increased by 2% y/y – to 284 million tons, driven by rising domestic steel demand.

The World Steel Association expects global steel demand to grow by 1.2% y/y in 2025 after two years of decline. This may further boost iron ore production and exports. Major mining companies such as Rio Tinto, BHP and FMG have kept their production forecasts stable. Vale even raised its production target to 325-335 million tons in 2025.

India, which reduced exports by 14% y/y in 2024, is likely to increase production to 305-310 million tons in 2025, offsetting the decline in export demand with domestic consumption.

The global iron ore market remains dependent on China, macroeconomic factors and the balance between supply and demand. 2025 could be a watershed year for the industry, especially if the steel industry recovers sustainably.

-

Opinions Industry steel consumption

13 July 2026

06 July 2026

01 July 2026

22 June 2026