Infographics EU 7163 10 September 2024

The EU steel industry has a huge unrealized potential to increase scrap consumption to meet the goals of reducing carbon emissions and developing a circular economy

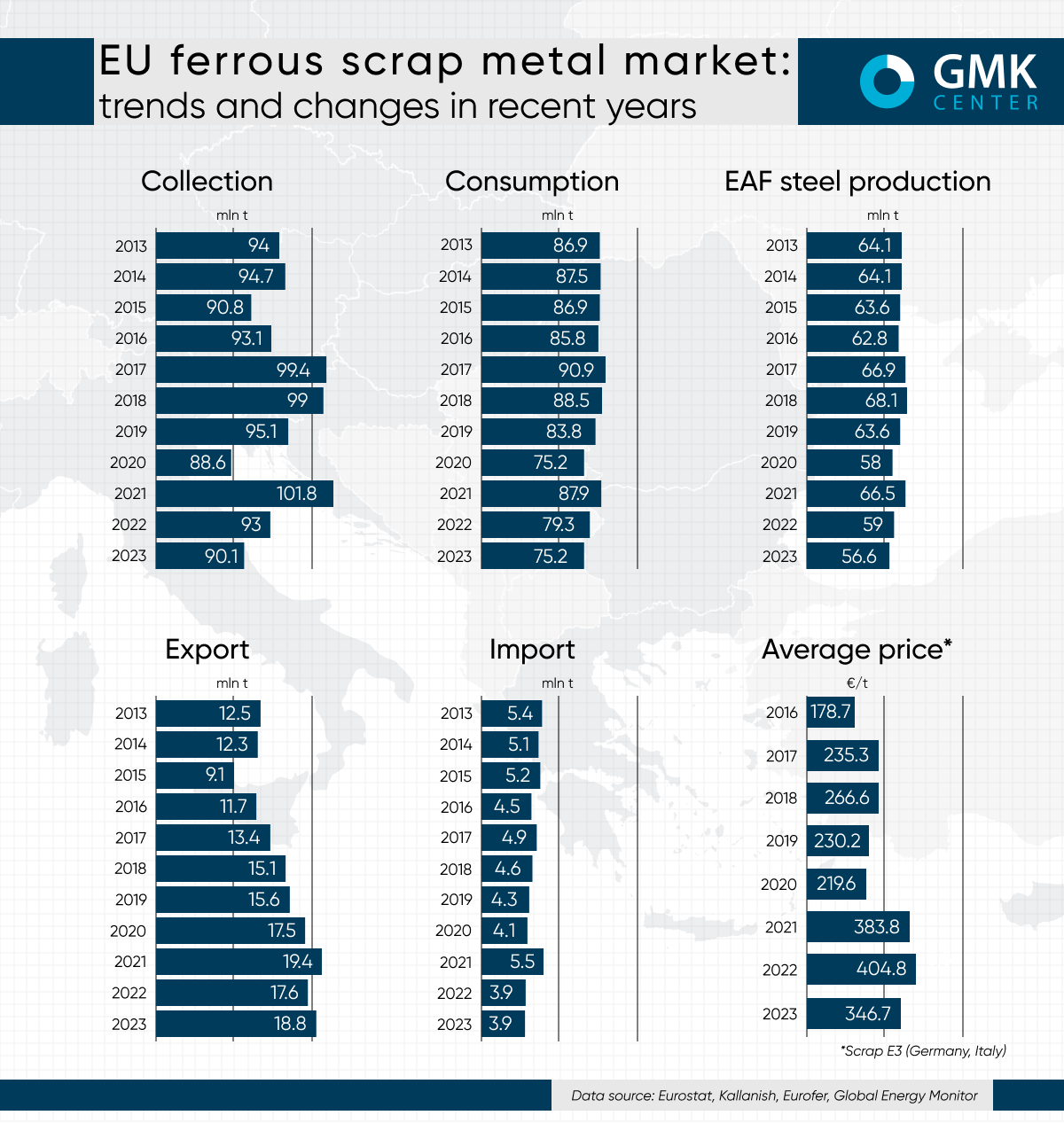

The scrap market in the European Union has undergone significant changes over the past decade, driven by various factors, including economic, environmental and geopolitical developments. The main trend affecting the market is the green transition, namely the increased use of scrap at existing facilities and the replacement of blast furnace – basic oxygen furnace (BF-BOF) facilities with new electric arc furnace (EAF) facilities.

Collection and consumption

Scrap collection in the EU remains a key element of green steel production. In 2013-2021, there was a gradual increase in scrap collection due to improved collection and processing technologies. Unfortunately, scrap consumption remained stable, with a slight increase in demand in Central and Eastern Europe.

However, the economic downturn in the EU caused by the COVID-19 pandemic and the Russian invasion of Ukraine in 2022 led to a temporary decline in steel production and, consequently, scrap consumption.

In 2020, scrap collection fell by 6.9% y/y– to 88.6 million tons, while consumption fell by 10.2% y/y – to 75.25 million tons. In 2022, the industry again showed negative dynamics, with collection decreasing by 8.6% – to 93 million tons and consumption – by 9.7% y/y, to 79.34 million tons. In 2023, collection decreased by 3.2% y/y – to 90.1 million tons and consumption – by 5.3% y/y, to 75.17 million tons, respectively.

The decline in scrap consumption in 2022-2023 is the result of a decline in electric arc furnace (EAF) steel production. Thus, in 2021, this production volume was estimated at 66.52 million tons (+14.7% y/y), in 2022 – 59.01 million tons (-11.3% y/y), and in 2023 – 56.58 million tons (-4.1% y/y). The decline in steel production in EAF is the result of rising energy prices since the second half of 2022.

The EU has a huge untapped potential to increase the use of scrap as part of steelmakers’ decarbonization strategies. Despite the fact that the decarbonization of the EU steel industry is publicly associated with the transition to electric arc furnace steel production using green hydrogen-based DRI, the real results of carbon emission reduction may be shown by an increase in the share of EAF production and, consequently, an increase in scrap consumption.

GMK Center estimates that in 2035, the EU will have 100-110 million tons of EAF capacity, with potential scrap steel production of 60-70 million tons per year.

“For one large integrated steel plant to entirely switch to 100% green steel production (based on green hydrogen), 50-60% of Germany’s current installed wind power generation capacity is reuqired. First, steel producers in the EU should increase the share of scrap in their existing capacities and switch to EAF steelmaking technologies. Only after maximizing the potential of utilizing existing scrap does it make sense to move on to the next steps: introduce the best technologies and modernize BF-BOF production, switch from coal to gas, introduce direct reduction technologies, use all the opportunities for carbon capture, storage and utilization (CCS, CCUS), and finally switch to hydrogen technologies when the infrastructure is ready,” comments Andreas Koller, Managing Director of Steel Partner Consulting, a leading international steel plant engineering consultancy.

Raw material prices

Scrap prices have been extremely volatile over the past 10 years, depending on numerous factors, including supply and demand on global markets, changes in trade policy, and economic and political events. For example, in 2016, scrap prices hit a low (≈€178.7/t) due to oversupply and weak demand. On the other hand, in 2021-2022, prices rose sharply (≈€383-404/t) due to a shortage of raw materials and high demand for steel after the pandemic. In 2023, the average EU scrap price was €346.7/t.

“Scrap prices are driven by demand from large consumers such as Turkey. But we need to understand that the price will never return to $180/t. Scrap has become a strategic raw material for the decarbonization of the steel industry. On the one hand, prices on local markets will be restrained by trade restrictions, while on the other hand, the competition for high-quality scrap on the global market will increase,” comments Stanislav Zinchenko, CEO of GMK Center.

Export and import

Over the past ten years, the volumes of scrap exports and imports in the European Union have fluctuated significantly.

Exports of raw materials gradually grew in 2013-2021, but began to decline after 2022. While in 2021 the EU scrap industry exported 19.43 million tons of scrap, which is an absolute record, in 2022 it was 17.63 million tons (-9.3% y/y), and in 2023 – 18.83 million tons (+6.8% y/y).

Although the market has adapted to the new realities, EU scrap exports are unlikely to exceed 2021 levels in the coming years. The green transition being implemented in the EU creates the preconditions for restricting exports of this critical raw material. The EU is already actively discussing this issue due to the gradual increase in demand within the bloc and the desire to protect its own steel industry.

On the other hand, imports of scrap to the EU have been fairly stable. However, in 2022, amid the war in Ukraine and sanctions against Russia, the EU reduced its scrap imports. Thus, in 2021, the EU imported 5.52 million tons of scrap (+34% y/y), but in 2022 it reduced volumes by 28.4% y/y – to 3.95 million tons, and in 2023 – by another 1.1%, to 3.91 million tons.

The balance of the EU scrap market will change over the coming years. The key trends include the following:

- steel producers are actively investing in vertical integration by acquiring scrap companies to secure their supply chains;

- investments in the collection, sorting and processing of scrap in the EU market are increasing;

- tighter trade restrictions will increase the impact on the availability of scrap on the global market.

-

Opinions Industry steel consumption

13 July 2026

22 July 2026

20 July 2026

06 July 2026