Infographics EU 4262 12 March 2025

Imports increased for the first time after two years of stagnation

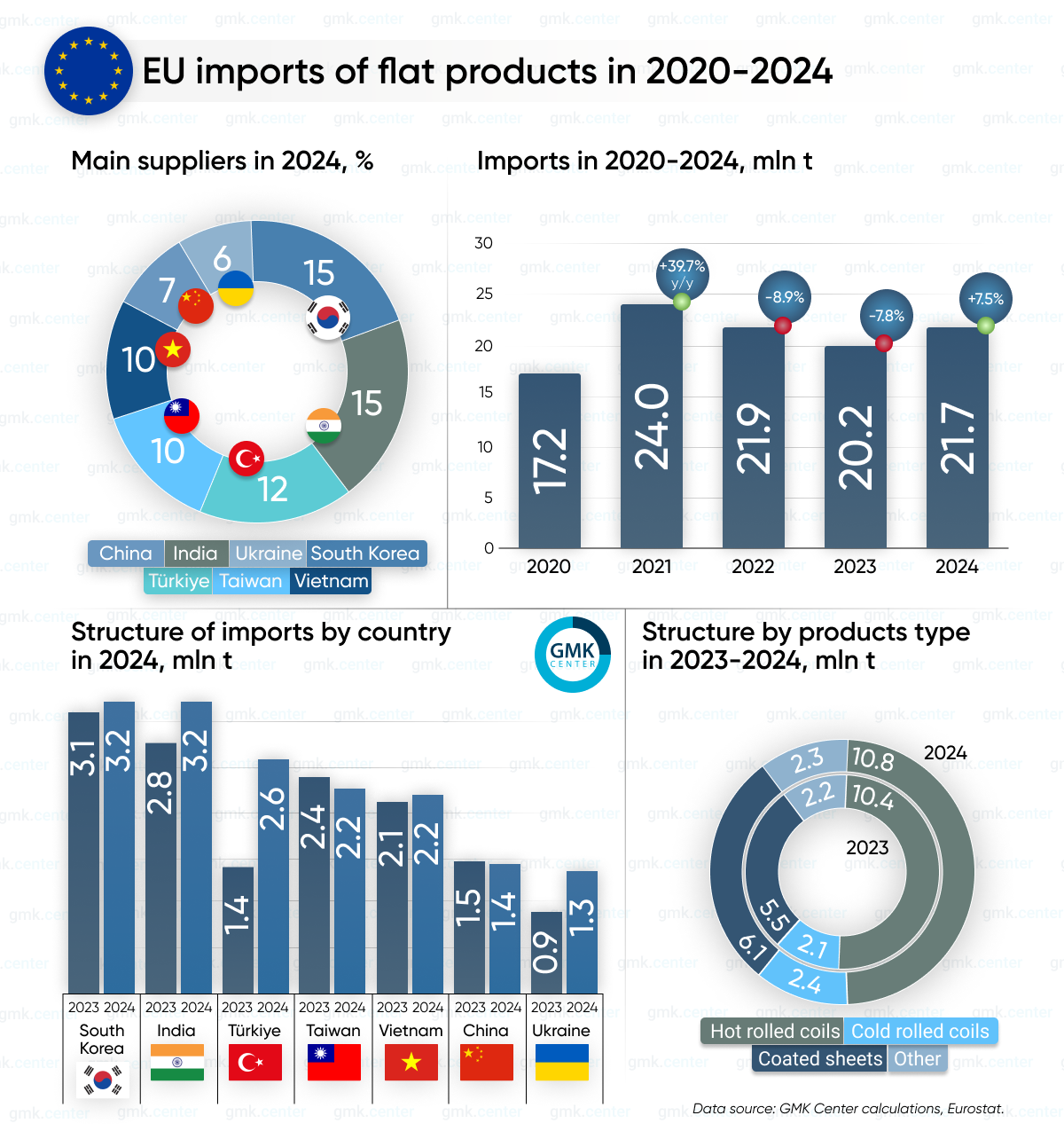

The European Union (EU) steel market received 21.68 million tons of flat products from third countries in 2024, up 7.5% from 2023. Imports increased for the first time after two years of decline.

Hot-rolled flat products (HS 7208) traditionally accounted for the largest import volumes, amounting to 10.81 million tonnes, up 4.3% y/y. Coated flat products (HS – 7210) also accounted for a significant share of supplies, with 6.13 million tonnes (+11.8% y/y), cold-rolled flat products (HS – 7209) – 2.44 million tonnes (+16.1%), and flat products made of other alloy steels (HS – 7225) – 1.11 million tonnes (-6.4%).

Key suppliers of flat products to the EU in 2024 include: South Korea, India, Turkey, Taiwan, Vietnam, China and Ukraine. These countries accounted for 75% of the total imports of the relevant products last year.

For example, South Korea increased supplies of flat products to the EU in 2024 by 3.5% y/y – to 3.21 million tons. Hot-rolled flat products accounted for the bulk of imports – 1.47 million tons (+6.1% y/y) and coated flat products – 1.03 million tons (-2.1%).

India shipped 3.18 million tons of flat steel to the EU, up 15.7% y/y. Of these, 1.6 million tons were flat hot-rolled products (+14.7% y/y) and 1.01 million tons were coated flat products (+16.2%).

Last year, the EU imported 2.59 million tons of flat products from Turkey, up 86.6% y/y compared to 2023, when imports suffered a significant decline. Flat hot-rolled products accounted for the bulk of supplies – 1.41 million tons (+129% y/y).

Taiwan and Vietnam exported 2.25 million tons (-5.1% y/y) and 2.15 million tons (+1.9% y/y) of flat products to European consumers, respectively.

Last year, imports of flat products from Ukraine increased by 48.7% compared to 2023, to 1.34 million tons. Hot-rolled flat products accounted for 1.13 million tons of supplies (+58.3% y/y), and flat steel products accounted for 154.6 thousand tons (+3.1%).

The largest importers of flat products among the EU countries are: Italy (6.23 million tons), Spain (4.02 million tons), Belgium (3.71 million tons), Poland (1.65 million tons), and Portugal (1.42 million tons).

Several key factors will influence the EU flat products market in 2025. Firstly, apparent steel consumption is expected to recover moderately after the decline in 2024, which may stimulate demand for imported products. Secondly, changes in EU protective quotas, in particular for galvanized and cold-rolled steel, may limit imports from certain countries. Given these factors, imports of flat products to the EU may remain stable or fluctuate slightly this year, depending on the balance between demand and regulatory restrictions.

“Last year, imports of flat products to the EU increased due to more active supplies from Asian countries, amid expanding exports from China. In addition, most product categories saw an over-concentration of suppliers, which reflected a price imbalance, with Asian suppliers offering lower prices. This resulted in pressure on prices in the EU, particularly in the second half of the year, and unprofitable operations of European steel producers,” comments Andriy Tarasenko, Chief Analyst at GMK Center.

European officials initiated changes to the quota system by introducing a 15% limit on the share of one country within the quota of other countries in the coil segment. This did not have the desired effect – imports remained at the same level, but there was a certain change in the market structure – Asian imports increased in the segment with higher added value (cold-rolled steel, coated steel), adds Andriy Tarasenko.

“By 2025, we expect that imports of flat products to the EU may decline by 15% as a result of changes in the tariff quota system,” summarizes the GMK Center analyst.

-

Opinions Industry steel consumption

13 July 2026

06 July 2026

01 July 2026

22 June 2026