Infographics DRI 22 18 June 2026

DRI projects depend on partnerships with iron ore miners

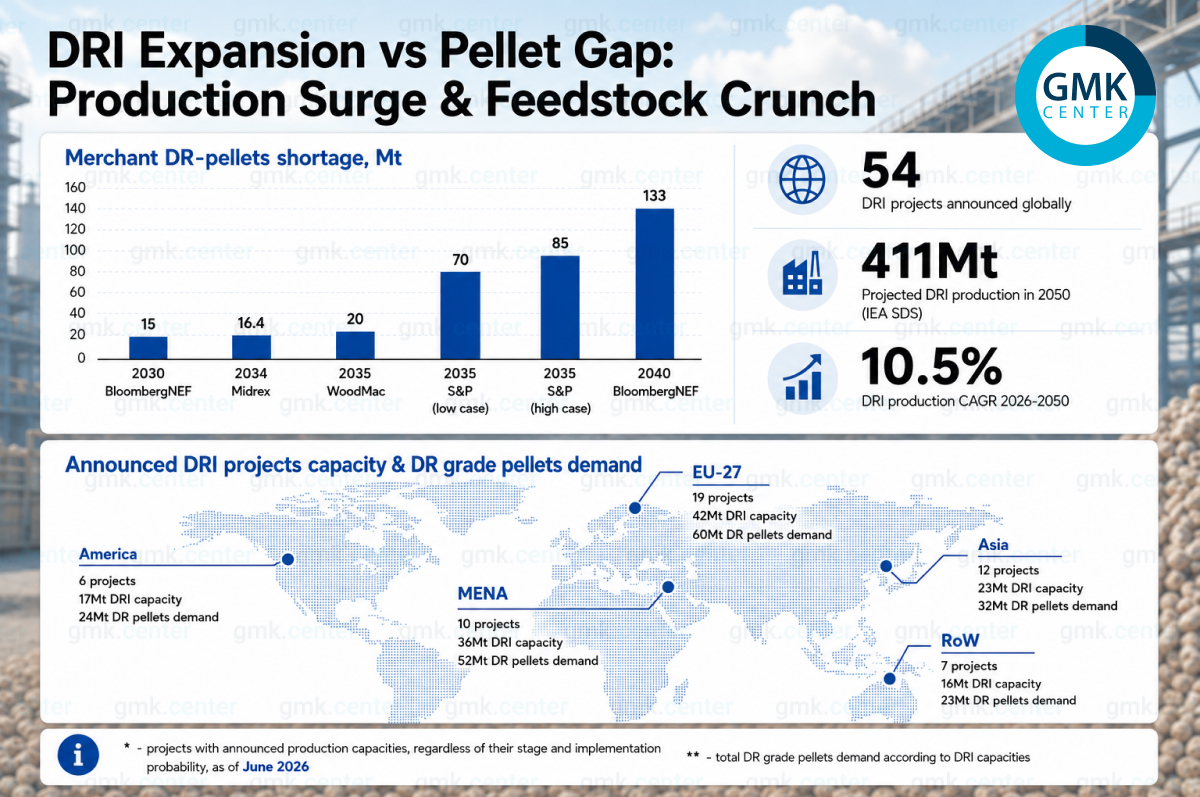

Steel decarbonization is a complex challenge, but securing suitable feedstocks is emerging as a central concern. Direct reduced iron (DRI) remains the primary route for lower-carbon steelmaking, and global momentum is strong. Industry data show 54 announced DRI projects totaling 134 million tonnes of annual capacity.

The EU leads the project pipeline, but the MENA has made notable strides with 36 million tonnes per year – a quarter of the total global announced capacity. MENA investors plan to exploit cheap gas and strong renewable potential to export HBI, demonstrating a decoupling of iron and steel production. That could help decarbonize regions where scrap is scarce.

Projects in the US, Brazil and Australia benefit from domestic iron ore and low-cost energy. By contrast, EU and MENA producers lack a local ore base and will depend on merchant suppliers, adding pressure to seaborne markets.

Limited high‑grade iron ore reserves make supply a growing risk. Announced DRI projects would require 190 million tonnes of DR‑grade pellets and 580 million tonnes by 2050, up from 48 million tonnes in 2025. Only 30% of current supply is available on a merchant basis. As more steelmakers move to DRI, competition for high‑grade material is accelerating.

Most forecasts point to a widening supply deficit after 2030. Equipment supplier Midrex expects a 16.5 million tonnes shortfall of DR‑grade pellets in 2034, while BloombergNEF sees the gap reaching 133 million tonnes by 2040.

Using an electric smelting furnace (ESF) offers only partial relief. ESF allows lower‑grade blast furnace pellets to be used for DRI. But spare capacity among global pellet exporters is already very tight, limiting this option.

Successful implementation of DRI projects will therefore depend on partnerships with iron ore miners to secure long‑term, reliable supply. Without such collaboration, raw material availability could become a critical bottleneck for the green steel transition.

-

15 June 2026

17 June 2026

04 June 2026

03 June 2026