Posts Global Market flat rolled steel 342 14 May 2026

In 2026, steel consumption is expected to increase by approximately 3%, to 3.4 million tons

Demand for finished steel in Sweden is entering a period of steady recovery after several years of stagnation. A unique public-private partnership model has laid the foundation for this process. The government is covering up to 15% of the costs associated with the green transformation of the steel industry and is investing billions of euros in critical infrastructure.

Key players

The largest local producer and a global leader in the high-strength steel segment is SSAB. In Sweden, the company operates three plants: in Luleå with a nominal capacity of 2.3 million tons per year, in Öxelesund with 1.5 million tons, and in Burlänge with 2 million tons. The latter is the largest rolling mill; there are no steelmaking facilities there. Other market participants:

- Avesta Works, one of the most high-tech plants in the world. Steelmaking capacity: 0.75 million tons; rolling capacity: 0.65 million tons. This is the Swedish division of the Finnish Outokumpu Group, specializing in cold-rolled and hot-rolled coils.

- The plants in Gofors, Smedjebacken, and Buxholm are consolidated into Ovako, a subsidiary of Nippon Steel. Steelmaking capacity in Gofors is 0.5 million tons. The combined capacity for steelmaking and the production of long products in Smedjebacken and Buxholm is 0.7 million tons. Electric arc furnace steelmaking takes place in Smedjebacken, while rolling mills are located in Buxholm. Ovako specializes in bearing steel and products for the automotive industry.

- The Alleima plant in Sandviken rounds out the list of operating facilities. It is a manufacturer of pipes, wire, and bars with a steelmaking capacity of 0.3 million tons. Despite its small scale, it is an important player producing high-margin products: precision tubes for the aerospace industry, medical wire, and more.

Stegra (formerly H2 Green Steel) is also worth noting. This is a new player that is literally knocking on the market’s door. The company is building a 2.5-million-ton hydrogen-based-DRI-EAF plant. This is the most ambitious hydrogen metallurgy project in Europe. The first phase of the project is nearing completion, with commissioning scheduled for late 2026.

Investments and public policy

- SSAB is undergoing a radical green transformation. Construction of electric arc furnaces (EAFs) is beginning at the Luleå plant; these will replace blast furnace-basic oxygen furnace (BF-BOF) production by the early 2030s. The project is valued at €4.5 billion, of which €70 million comes from EU grants. Construction of the EAF in Oxelesund is in full swing, with blast furnaces expected to be shut down in 2027.

- Ovako has focused on decarbonizing intermediate production stages. In August 2023, the world’s first facility for producing green H2 (which replaces natural gas during steel heating prior to rolling) was launched at the plant in Gofors. The project cost €17 million.

At the plant in Buxholm, a new heating furnace capable of running on natural gas and hydrogen was commissioned in March 2025. The project cost €6 million.

- In 2025, Alleima launched a new vacuum arc remelting (VAR) furnace for steel. Also in 2025, new thermal spraying lines were launched for precision tubes and coatings for hydrogen electrolysers. The company invests €25–30 million annually in R&D and the improvement of production processes in Sandviken.

- Outokumpu invests €150–200 million annually in development. A significant portion of these funds is directed toward its Finnish and Swedish sites. In particular, the integration of digital supply chain management systems was completed at Avesta Works in 2024. Here, one of the lowest specific CO2 emission rates for stainless steel has been achieved—0.46 tons—mainly thanks to the use of green electricity.

The Swedish government is not merely a regulator but an active co-investor in the green transition. Support is provided through direct subsidies, preferential loans, and infrastructure development.

The main instrument for state investment is the Industrial Leap (Industriklivet) fund. It is designed to support the implementation of technologies that reduce emissions in energy-intensive industries and is managed by the Swedish Energy Agency (Energimyndigheten).

- In September 2024, Stegra received €100 million directly from the fund. The total amount of support will be €265 million.

- In November 2025, SSAB received €28.7 million for the electrification of its finishing processes for rolling and galvanizing in Luleå.

- Ovako received grants totaling €15–20 million for the construction of a hydrogen hub in Gofors.

Pan-European mechanisms, in which the Swedish government acts as a guarantor, are being actively utilized.

- The EU Innovation Fund has allocated €143 million in grants for the construction of a demonstration plant for hydrogen-based DRI production for HYBRIT (a joint project of SSAB, LKAB, and Vattenfall). Stegra received confirmation of a €250 million grant in 2024–2026 to scale up its plant in Boden (capacity is expected to increase to 5 million tons per year by 2030). Total project funding has reached €6.5 billion.

- The Just Transition Fund has allocated €132.4 million to SSAB for the EAF transition project in Luleå. An additional €71 million has been allocated to this company in 2026 for employee retraining.

Thanks to government guarantees through the Swedish Export Credit Agency (EKN) and the Swedish National Debt Office (Riksgälden), it has been possible to secure €4.2 billion in loan capital for the Stegra project.

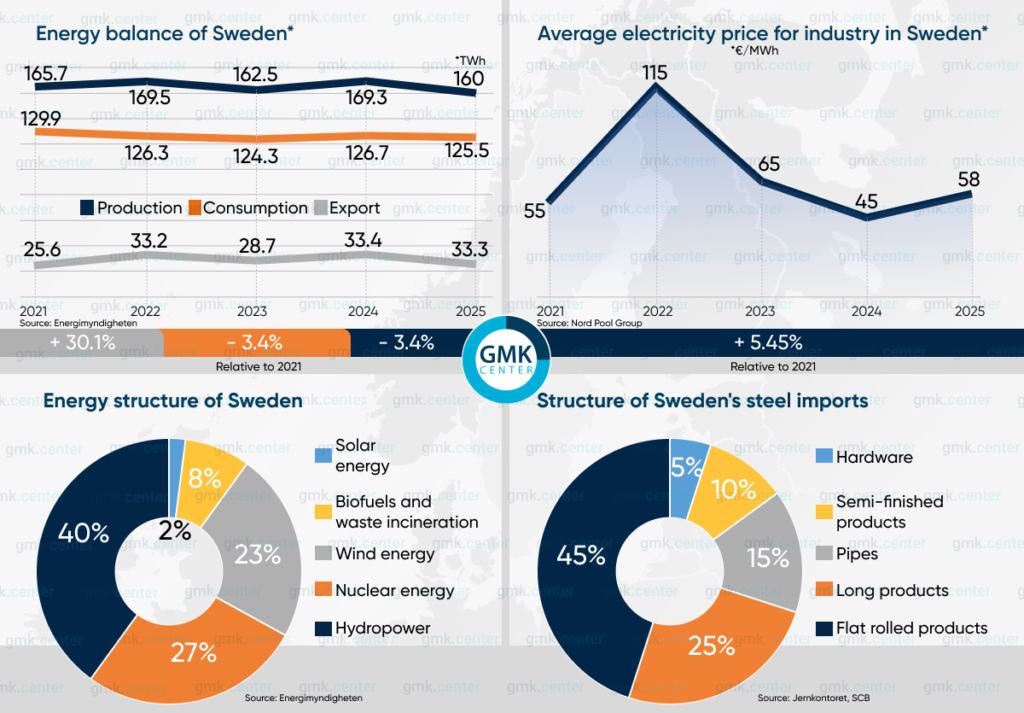

Infrastructure projects are a key focus. The state-owned company Svenska kraftnät is investing hundreds of millions of euros in expanding power line capacity in the north of the country. The goal is to supply steel mills (especially Stegra and SSAB) with massive amounts of green electricity. The demand of the Bodén plant alone is comparable to the consumption of all of Denmark, while energy production is concentrated primarily in the northern regions.

Since 2019, the government, through the Swedish Transport Administration (Trafikverket), has been modernizing the Malmbanan railway. Since 2024, a large-scale replacement of the track has been underway to accommodate heavy freight trains, along with the construction of new passing tracks and stations.

The transport of iron ore via the Malmbanan railway from LKAB’s mining operations in Kiruna to the SSAB and Stegra plants is critical to maintaining uninterrupted operations, along with a stable electricity supply. Thus, the state covers indirect costs that are critical for the steelmakers. And although the companies themselves bear the main costs of the green transition, total state support amounting to 10–15% makes their investments economically viable.

The energy component

The cost of electricity during the green transition is critical for steel production. The Swedish government has established a system of indirect incentives that make electricity cheaper for steelmakers than in the rest of Europe. How does this work in practice?

- Long-term PPAs (Power Purchase Agreements) form the basis of the Swedish model. Large companies (SSAB, Stegra, Ovako) enter into direct contracts with energy producers (such as the state-owned giant Vattenfall) for 10–20 years in advance. The price is fixed at a low level, often below the market spot rate. The government, through the EKN agency, provides credit guarantees for these contracts. This reduces risks for energy producers, allowing them to offer more favorable terms to steelmakers.

- The government has set minimum energy excise tax rates for energy-intensive industries, including steelmaking. Industrial enterprises currently pay 0.6 ö/kWh, while households pay 45 ö/kWh (including 25% VAT).

- The state pays compensation to power companies for the carbon component in the electricity price. This component exists despite the fact that 99% of Sweden’s electricity generation comes from hydropower, nuclear power, and wind power. However, Sweden is part of a single electricity market with the rest of Europe. Swedish electricity producers incorporate the cost of CO₂ allowances into electricity prices because they operate within European common market. Swedish steelmakers must purchase an additional 10% to 30% of their electricity needs on the spot market (Nord Pool). As a result, partial government for the CO₂ component embedded in electricity prices is highly important for the industry.

Thanks to the mechanisms mentioned above, in 2025, large Swedish plants in the north purchased electricity at a price of €30–45/MWh. The average wholesale price for industry in the EU at that time was €95/MWh.

Overall, Sweden is a net exporter of electricity. The main destinations for exports are Finland, Lithuania, Poland, and Germany. However, during peak hours and periods of low wind, the power grid receives imports from Poland and Germany. Energimyndigheten forecasts an increase in energy consumption from the current 130 TWh to 250–280 TWh by 2045 due to the green transition in the steel industry and other industrial sectors.

Market profile

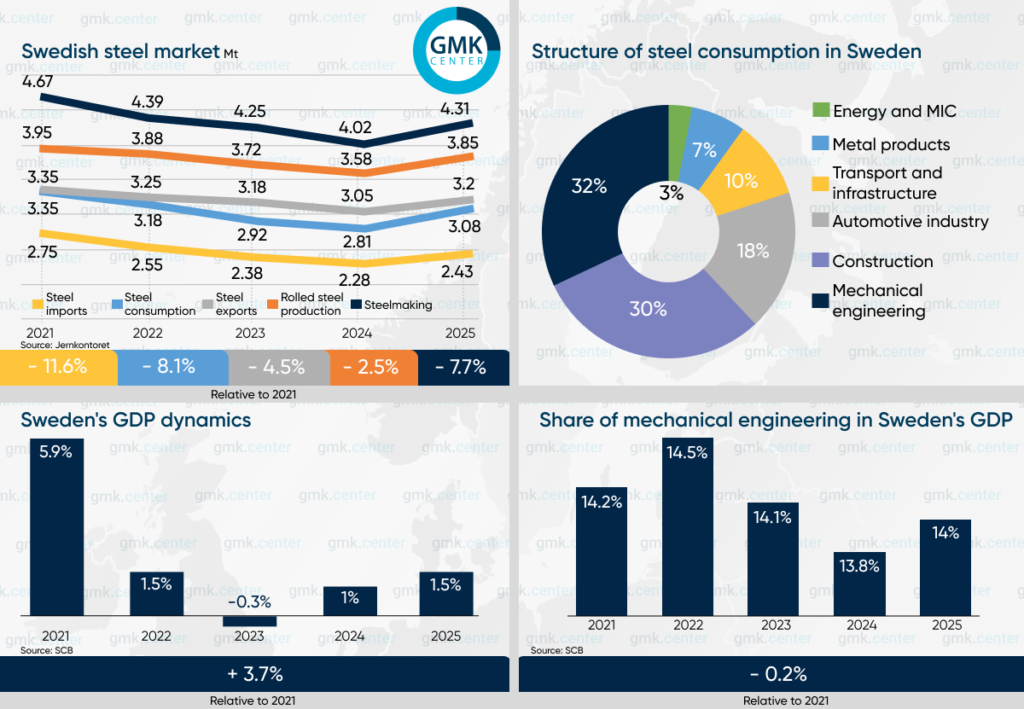

Flat-rolled products (hot-rolled and cold-rolled sheets) account for approximately 65–70% of total steel production. Most of this is produced at SSAB’s plants in Luleå and Burlänge, which cater to the automotive and heavy machinery sectors.

Crude steel and rolled product output in Sweden declined steadily between 2022 and 2025 amid the broader European economic slowdown. The drop in production in 2024 was also partly linked to preparations for plant modernization. In the second half of 2025, rolling mill utilization improved as inventories at traders and steel plants declined.

Sweden remains a stable net exporter of steel, although its positive steel trade balance is trending downward in terms of physical volumes. Foreign contracts account for 82–88% of total sales by Swedish steel mills. The main destination is Germany, which accounts for about 20% of all shipments. Other significant partners include Italy, the United States, China, and Norway.

Due to the stagnation of the German economy, Swedish exporters actively shifted their focus to the U.S. and Indian markets in 2024, where demand for wear-resistant steels from mining equipment manufacturers remained stable. In 2025, they actively replaced capacity in Germany and France that was being phased out or shut down due to high natural gas costs.

Imports account for 75–85% of Sweden’s domestic steel consumption. Local production is focused on the high-margin export segment. It is more cost-effective to import construction rebar, standard long products, and ordinary hot-rolled sheet for machine building from neighboring EU countries.

The largest volumes of imports come from Finland—25–28% (this includes supplies of semi-finished products for Avesta Works from Outokumpu), Germany—18–20%, Italy—10%, Poland—7%, and Austria—5–6%.

The share of China, India, and Turkey in Swedish imports began to decline in 2024, even before the official launch of CBAM payments. Swedish consumers (primarily automakers) had already begun requiring reports on CO2 emissions from steel production during the tender phase. Imports from Finland and Germany became a higher priority, as their products are easier to certify as low-carbon. Poland became the main supplier of rolled steel and finished steel structures for the construction industry.

Steel consumption

The Swedish economy has stabilized following the EU energy crisis, which triggered a surge in inflation and a tightening of the Riksbank’s monetary policy. Steel consumption trends are in line with this pattern.

Demand for flat-rolled steel is more stable than for long products, thanks to export orders for Swedish industrial equipment. The main buyers of steel sheet include:

- Volvo Group, Volvo Cars, Scania (automotive industry).

- Atlas Copco (compressor manufacturing).

- Epiroc and Sandvik (manufacture of mining and tunneling equipment).

- ABB (power generation equipment).

- SAAB (aircraft and shipbuilding).

- SKF (production of bearings).

Foreign contracts account for up to 80% of sales for Swedish engineering giants. Hence their dependence on the economic situation in the EU. In 2024–2025, due to the European crisis, production of construction and household equipment declined in Sweden. The decline was offset by growth in the power machinery sector (transformers, hydrogen electrolysers) and the defense industry. This supported demand for high-strength steel sheet.

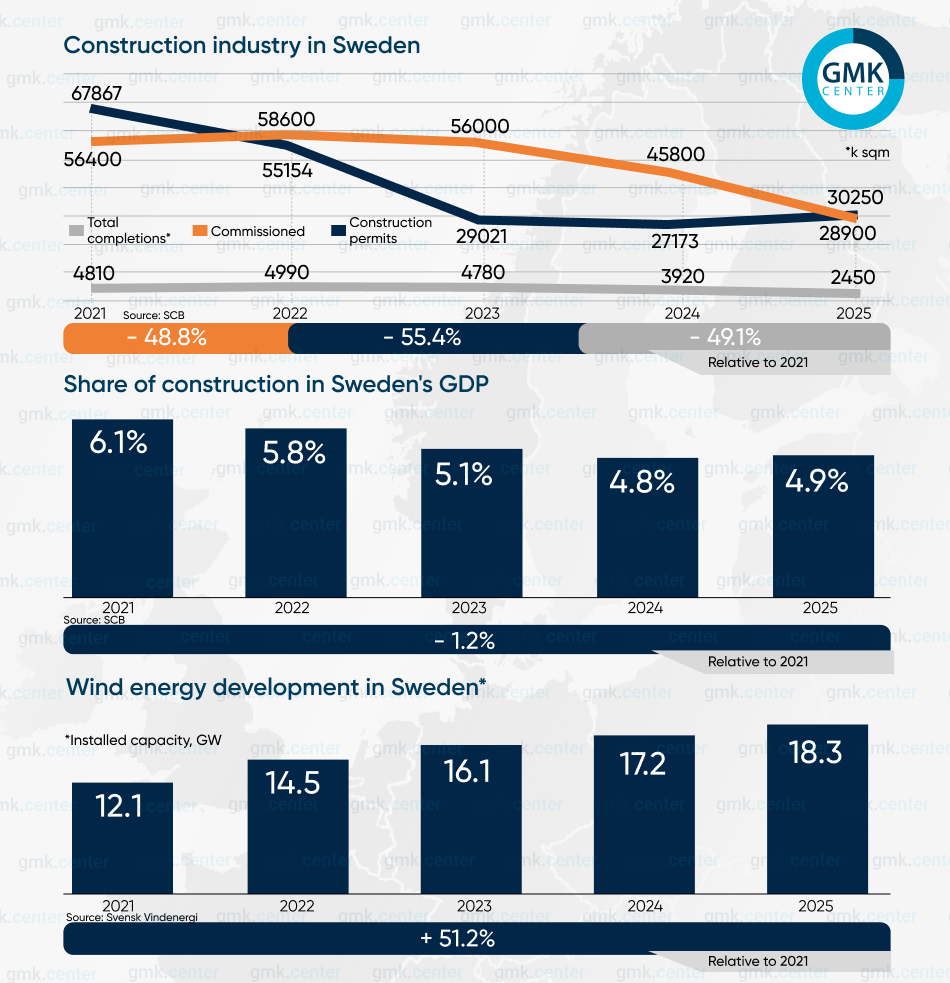

The construction sector is going through its most difficult period. The inflationary shock of 2022 led to higher prices for building materials and an increase in the Riksbank’s base rate from 2.5% to 4.0% in 2023. As a result, residential construction in Sweden has become unprofitable. The residential segment accounts for 40–50% of total construction work (in monetary terms), so construction’s contribution to national GDP in 2024 fell to its lowest level since 2014.

Demand for steel rebar and mesh collapsed, though it was partially sustained by industrial and infrastructure construction. In 2025, the government invested €14.01 billion in infrastructure development. This enabled the industry to improve its performance by boosting sales of long products and bridge steel structures. In 2025, the residential sector was reeling from the effects of the previous three years of crisis. The volume of housing units completed hit a historic low.

Despite the crisis, wind power has grown at the fastest rate among all types of power generation in recent years. By 2025, Sweden had established itself among the EU leaders in this regard.

An important detail: Between 2021 and 2025, Sweden’s real GDP increased by 5.7% (adjusted for inflation), while steel consumption declined. This is due to the structure of the economy. It grew thanks to the service sector, primarily the IT sector, financial services, and engineering services.

The reduction in steel intensity in the mechanical engineering and automotive industries—the main consumer sectors—also played a role. To build electric vehicles with a long range, Volvo and Scania use advanced high-strength steels (AHSS). These allow for thinner sheet steel while maintaining strength. As a result, fewer kilograms of steel are used per vehicle body than five years ago, even though the cost of the vehicle (and its contribution to GDP) is higher. Similarly, modern machine tools and armored vehicles require higher-quality and more complex steel, rather than greater mass.

Outlook for flat steel consumption

The Riksbank, the National Institute of Economic Research (NIER), and SEB, Sweden’s largest private bank, believe that 2026 will mark the full recovery of the Swedish economy. GDP growth is expected to reach 2.1–2.4%. However, as noted above, this does not imply an increase in steel consumption. Other factors will influence it.

The forecast of a 2% increase in flat steel sales is based primarily on optimistic expectations from the automotive industry. According to calculations by the Mobility Sweden association, passenger car production will increase by 1.5% to 198,000 units, and truck production by 2% to 96,000–98,000 units. Key drivers:

- The success of the new EX60 electric crossover. Volvo Cars has revised its production plans upward.

- Volvo Trucks launched production of the FH Aero Electric with a range of 700 km in April 2026. This model will ensure full capacity utilization at Swedish plants for the entire year, the company states.

- In early 2026, Scania noted high demand in Europe and an acceleration in the transition to BEVs (electric trucks). Sales in Q1 fell by 6% to 20,978 units, but orders for the current quarter increased by 10% to 27,318 units.

The increase in Sweden’s defense budget to 2.6% of GDP means additional orders for special steel for armored vehicles and the navy, up to 0.6% of last year’s consumption volume.

By the end of 2026, the installed capacity of Swedish wind farms will reach 20 GW, with an increase of 1.7 GW. As of May, approximately 0.6 GW of capacity is currently under active construction, while the steel structures for the remainder still need to be procured.

This expansion is projected following the central government’s decision to allocate €34.09 million to local communities for hosting wind farms. Previously, municipalities blocked up to 75% of applications for the construction of such facilities. Another benefit is that property taxes from wind turbines will now remain in local budgets.

In 2026, many wind turbines from the early 2000s will reach the end of their 25-year operational cycle. They are set to be replaced with new, more powerful models. This will require significant volumes of steel structures.

Outlook for long products

Demand for rebar and structural steel will show positive growth for the first time in four years—up 4.5%. According to Riksbank estimates, housing investment will increase by 5–7% thanks to last year’s reduction in the discount rate. The number of housing starts will rise by 24%, to 35,100 units. However, the low base effect of 2025 must be taken into account here.

The infrastructure segment will be the primary driver of the 10% overall increase in construction volumes. The Swedish government previously approved the largest-ever state program for the development of transport networks for 2026–2037.

State-owned company Vattenfall’s expenditures on power line upgrades alone for 2026–2030 will total €15.2 billion. This exceeds all government infrastructure spending in 2025.

According to the document, spending on road infrastructure will increase by 30%. The construction of new facilities and the repair of existing roads will create additional demand for long-haul rentals, amounting to at least 150,000–200,000 tons in 2026. Notable projects include:

- Construction of the Norrbotniabanan (North Botnia Line), a 270-kilometer railway line between Umeå and Luleå along the northern coast. Construction of bridges and overpasses on the Umeå–Skellefteå section is currently in full swing; there will be about 250 of them. The second section of the road, Skellefteå–Luleå, is in the design phase.

- Förbifart Stockholm (Stockholm Bypass). This is one of the longest road tunnels in the world (21 km, of which 18 km is underground). In 2025, excavation work was underway; currently, the installation of technical systems and the reinforcement of the tunnel arches are in progress. Commissioning is scheduled for 2030.

- Västlänken (Western Link), a railway tunnel under central Gothenburg with three new stations. The first phase—the underground section of Gothenburg Central Station—will open in December 2026. The project is being implemented under very challenging geological conditions, requiring a massive volume of steel piles and sheet pile walls.

- Continued modernization of the Malmbanan.

Overall, steel consumption in 2026 will increase by 3%, to 3.4 million tons.

-

OpinionsGlobal Marketmacroeconomics

28 May 2026

27 May 2026

20 May 2026

07 May 2026