Infographics EU 765 13 April 2026

Due to sanctions, the EU cast iron market is becoming more diversified, with alternative suppliers gaining ground

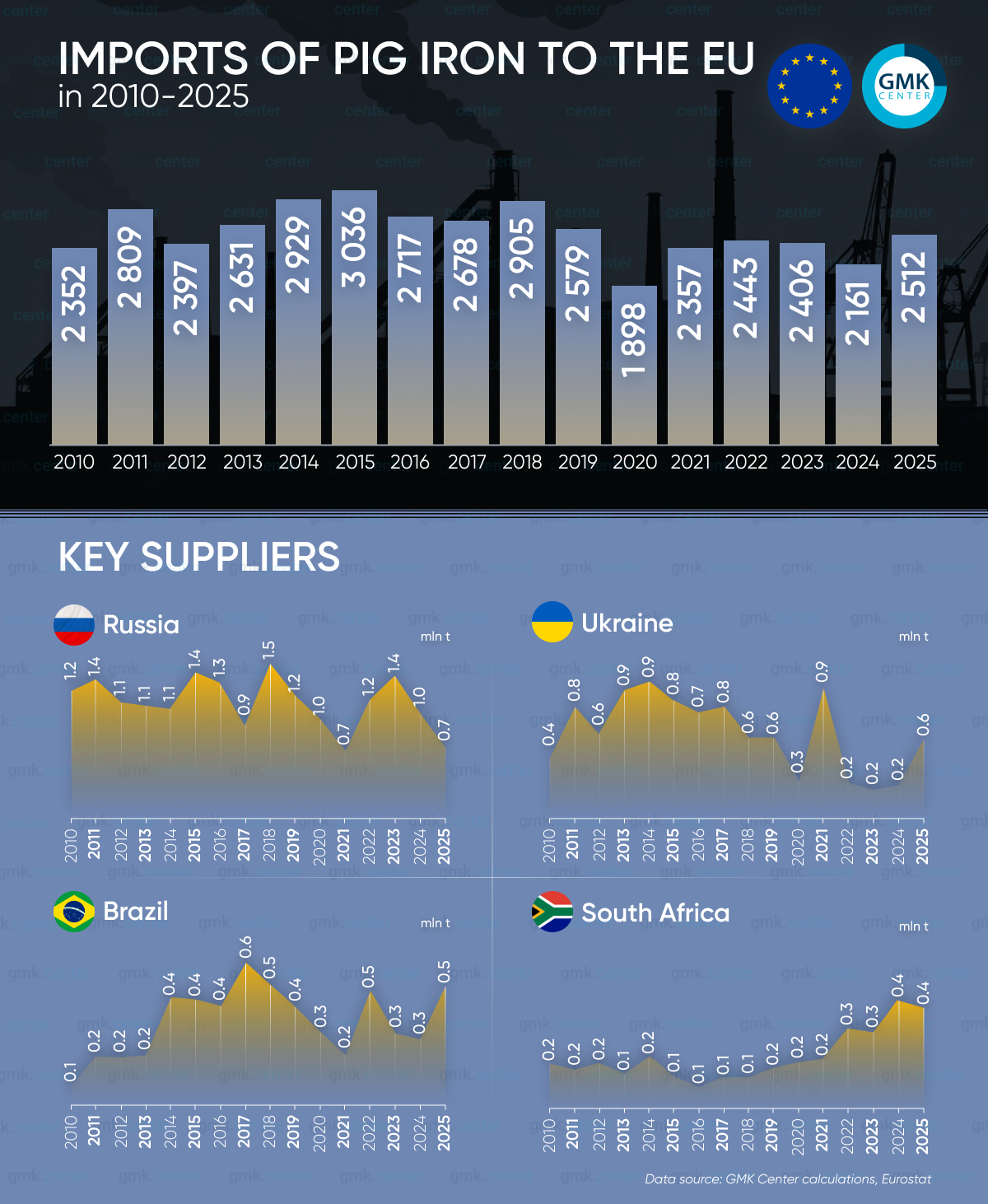

Pig iron imports into the EU rose to 2.51 million tons in 2025, a 16.2% year-on-year increase. Following a relatively weaker 2024, this indicates a partial recovery in purchases, although in the longer term the market still remains below the peak levels of the mid-2010s. Specifically, compared to 2010, imports increased by only 6.8%, and compared to the 2015 peak of 3.04 million tons, they were 17.3% lower.

Overall, between 2010 and 2025, the EU pig iron market went through several phases. From 2010 to 2019, imports fluctuated mainly between 2.35 and 3.04 million tons, and the supply structure was fairly stable. In 2020, imports fell to 1.90 million tons, marking the lowest level for the entire period. Subsequently, the market partially recovered: in 2021–2023, the figure remained around 2.36–2.44 million tons, fell to 2.16 million tons in 2024, and rose again in 2025.

Russia remained the largest supplier of pig iron to the EU in 2025, with 699,990 metric tons, or 27.9% of total imports. At the same time, its shipments fell by 32% year-on-year, and its share dropped sharply from 47.7% in 2024 and 53.4% in 2010. Ukraine ranked second with 566,770 metric tons (22.6%), increasing exports by 135.5% year-on-year. Brazil came in third with 500,150 metric tons (19.9%; +80.4% year-on-year), and South Africa ranked fourth with 401,850 metric tons (16%; -6.8% year-on-year). Collectively, these four countries accounted for 86.4% of pig iron imports to the EU in 2025.

Over the entire 2010–2025 period, Russia remained the leader with a total share of about 44.8%, followed by Ukraine (24%), Brazil (13.8%), and South Africa (8.3%). However, the market structure gradually changed. While Russia’s dominance was unquestionable at the beginning of the period, in recent years the EU has increasingly relied on diversifying its supplies. This is particularly evident in the growing role of Brazil and South Africa and Russia’s less stable share.

The current market situation remains mixed. On the one hand, sanctions, logistical risks, and geopolitical instability are forcing European consumers to reduce their dependence on specific sources. On the other hand, pig iron remains a vital raw material for the EU’s steel industry, and it is difficult to quickly replace large volumes of supplies. Therefore, in the short term, the market is likely to remain volatile, with a subsequent redistribution of market shares among key exporters and a gradual strengthening of alternative supply routes.

“The outlook for pig iron exports to the EU in 2026 is uncertain. According to our calculations, CBAM payments for Ukrainian pig iron amount to 65 euros per ton. Price trends do not allow for these payments to be passed on to prices in the first half of 2026. Therefore, at the beginning of the year, pig iron exports from Ukraine to the EU are virtually nonexistent. These volumes have been redirected to the U.S. market,” comments Andriy Tarasenko, Chief Analyst at GMK Center.

-

Opinions Industry steel consumption

13 July 2026

22 July 2026

20 July 2026

06 July 2026