Infographics billets 560 06 April 2026

Growth was observed in both the slab and square billet segments, and China’s market share increased particularly sharply

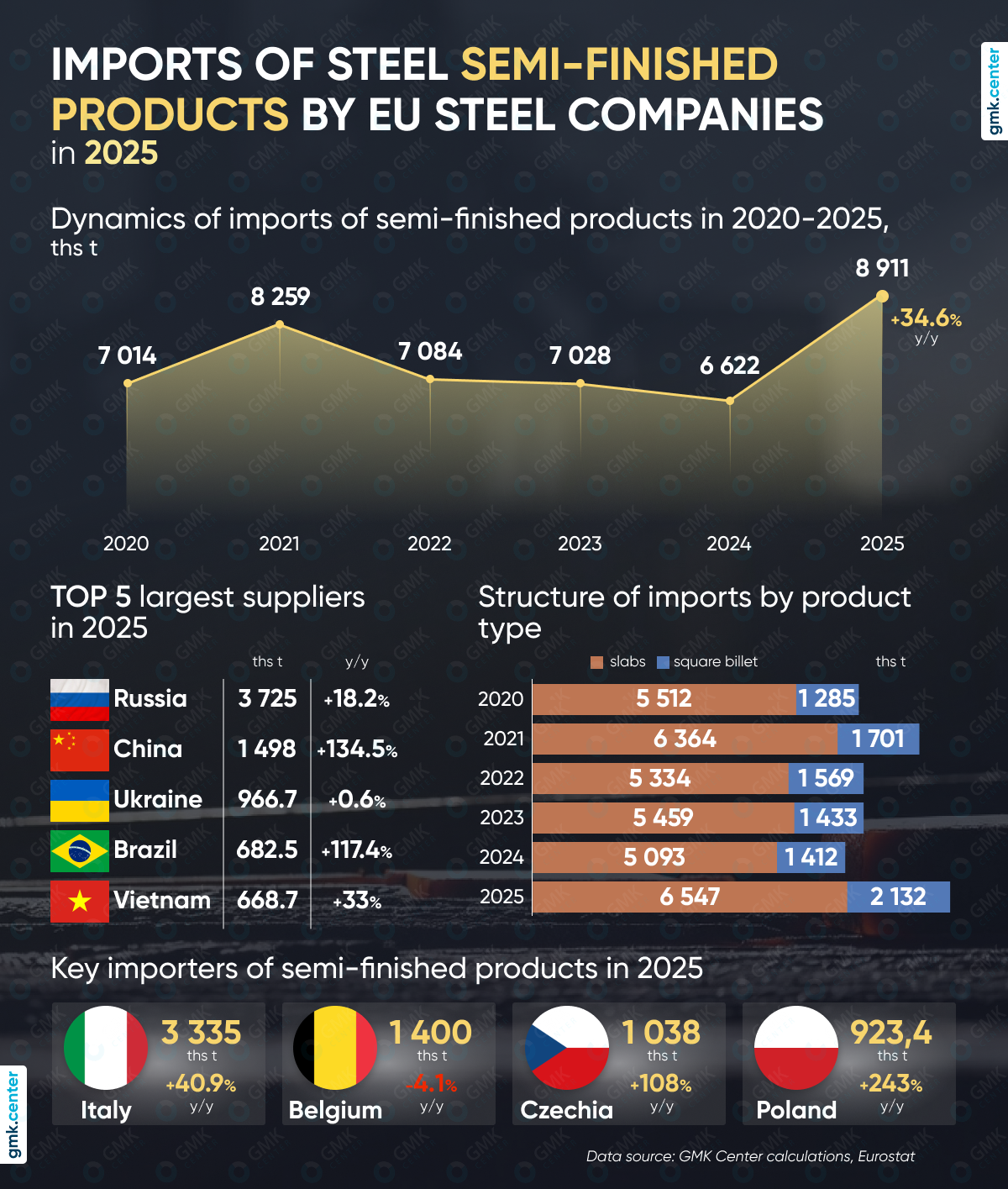

In 2025, the European Union (EU) significantly increased its imports of semi-finished steel products. Total imports reached 8.91 million tons, a 34.6% year-on-year increase — the highest figure in recent years. For comparison: in 2024, imports amounted to 6.62 million tons, and in 2023 – 7.03 million tons.

Slabs remained the key product category. Imports of slabs grew by 28.6% year-on-year to 6.55 million tons, accounting for 73.5% of total shipments. Meanwhile, imports of square billets increased even more rapidly — by 51% year-on-year — to 2.13 million tons. Their share rose to 23.9% from 21.3% a year earlier.

Among suppliers, Russia remained the largest source of semi-finished products for the EU—3.73 million tons, or 41.8% of total imports. This represents an 18.2% increase year-on-year. China took second place, effectively becoming the main driver of the upward trend: shipments grew by 134.5% year-on-year – to 1.5 million tons, and its share reached 16.8%. Ukraine retained third place with 966,700 tons (+0.6% year-on-year), accounting for 10.8% of the market. Brazil also saw a significant increase — 682,500 tons (+117.4%) — as did Vietnam — 668,700 tons (+33%).

In terms of absolute growth, the largest contributions to the increase in imports came from China (+859,000 tons by 2024), Russia (+573,000 tons), and Brazil (+369,000 tons). This points to further diversification of procurement, although dependence on Russian supplies remains very high.

Italy was the main consumer of imported semi-finished products in the EU — 3.34 million tons, or 37.4% of the total volume, which is 40.9% more year-on-year. Next came Belgium – 1.4 million tons (-4.1% year-on-year), the Czech Republic – 1.04 million tons (+108%), Poland – 923,400 tons (+243%), and Denmark – 559,200 tons (-5.1%). The sharp increase in the Czech Republic, Poland, and Romania point to a growing level of processing of imported billets and slabs in Central Europe.

Overall, the import structure shows that in 2025, European consumers were more actively meeting their needs through external supplies. This was likely due to efforts to minimize raw material costs for rolling mills, as well as a broader supply from Asia and South America. At the same time, China’s growing role, combined with Russia’s still significant share, indicates that the EU market continues to rely on traditional suppliers of semi-finished steel products.