Posts Green steel green steel 1564 25 September 2025

Local players rather than global companies can ensure the success of Brazilian metallurgy decarbonization

Brazil’s steel sector could easily be green by now. As recently as 2023, 93% of all electricity (e/e) generated here was from renewable energy sources (RES), according to the Global Energy Monitor. The country also has the world’s second largest reserves of high-quality iron ore (Fe60-67), which does not require additional beneficiation. Finally, it has a fairly well-developed gas production. Plus the possibility of importing gas from neighboring Argentina.

Thus, everything is in place to build a Middle Eastern model where 100% of steel is smelted using NG-DRI-EAF technology with average emissions of 1.3-1.4 tons of CO2 per 1 ton of finished steel products. However, EAF in Brazil now accounts for only 24% of steel capacity. The remaining 76% is BF-BOF. Moreover, local steelmakers have to import all the coal and coke needed for their operation. As a result, average CO2 emissions in Brazilian metallurgy amount to 1.7 tons. And it is problematic to reduce them for a number of reasons.

On the periphery of public policy

Why have EAFs not become widespread in Brazil? First, because of the lack of a resource base. Scrap collection volumes are relatively small and, strange as it may sound, there are no DRI plants here. And this is despite the huge investment opportunities of Vale SA corporation, the world’s largest exporter of iron ore. The situation looks paradoxical. But.

DRI production here is unprofitable because of the high cost of natural gas. According to the Brazilian research center Energy Transition, the country ranks 3rd in the world in terms of gas prices. Only Sweden and Finland are more expensive. And difficult production conditions are not the most determining factor. The main problem is the lack of a gas market. The state corporation Petrobras is an absolute monopolist in the field of supply.

Accordingly, metallurgists cannot count on competitive prices. Plus extremely high taxes. They account for about 26% of the gas price for consumers. That is why Vale is investing in the largest complex to produce 12 million tons of DRI/HBI per year in Saudi Arabia. And Ternium is planning a DRI plant in Mexico, but not in Brazil itself.

Second, EAFs allow higher quality steel to be produced. But it costs more than blast furnace-converter technology. Therefore, it cannot compete with cheap imported steel products. This is exactly what foreign BF-BOF mills supply, mainly from China.

Now they can do it unhindered, as there is practically no tariff protection of the domestic market. Thus, in 2024, steel imports to Brazil soared by 24% to a record 6.23 million tons. Of this, 92% came from China. And this is not an ad hoc surge. This is a multi-year trend.

Accordingly, Brazilian producers have no incentives to increase the share of EAF in total production. This means that there are no prerequisites for growth in demand for DRI, the main raw material for electric arc melting of steel.

The next question is why is this happening? Probably the reason is that the steel sector accounts for only 4% of Brazil’s CO2 emissions. Whereas the agribusiness sector accounts for 65%. Therefore, steel is not among the priorities in the national decarbonization policy, which aims to achieve a carbon-free economy by 2050.

Brazilian President Luiz Inácio Lula da Silva has repeatedly stated in public speeches the need for green steel production in the country. However, the 2024 Industrial Decarbonization Action Plan does not directly address the steel industry. Brazil’s updated October 2023 National Emissions Document (NDC) does not identify specific mitigation measures or emission targets for the steel industry.

Company plans

Brazilian steel companies’ decarbonization plans are quite conservative and based on the availability of local resources.

- ArcelorMittal Brasil, the largest producer, has pledged to reduce emissions by 10% by 2030 compared to the base year of 2018. This is to be achieved by increasing the use of scrap and natural gas in BF, as well as optimizing the use of charcoal;

- The second largest producer Gerdau has not set emission reduction targets at all. However, it is precisely this company that can afford to take its time. Its average emissions are 0.93 tons of CO2 – because steel is smelted in the EAF and 73% of the raw material is scrap. Gerdau is also highly energy efficient and uses charcoal;

- Ternium aims to reduce its CO2 emissions by 20% by 2030. This will involve increasing the use of scrap and RES, improving energy efficiency, and partially replacing coal with charcoal;

- Large flat-rolled steel producer Usiminas will reduce emissions by 15% by 2030 compared to 2019. The same instruments as Ternium will be used. Usiminas has invested $538 million in 2024 to modernize the BF at the Ipatinga mill, which accounts for 70% of the company’s emissions;

- CSN Corporation will reduce greenhouse gas emissions by 10% by 2030 and 20% by 2035 compared to 2018 through operational efficiency improvements. CSN Group has implemented H2 blowing into a kiln at its cement plant in the US as a pilot project. And now the developer, UTIS, will try to adapt this technology for blast furnace production in Brazil. CSN’s iron ore division will reduce CO2 emissions by 30% by 2035 and 100% by 2044;

- Vale Corporation will reduce Scope 1 and 2 greenhouse gas emissions by 33% by 2030 compared to 2017. By 2050. – By 100%. Including by increasing the use of RES to 100% compared to 84% in 2024. In 2022, the corporation launched the 766 MW Sol do Cerrado (Minas Gerais state) SES, one of the largest in Latin America. Other areas of decarbonization include replacing coal in sintering furnaces with biochar. Vale intends to reduce Scope 3 CO2 emissions by 15% by 2035. Ways to achieve this: electrification of road and rail transportation, use of bioethanol and biodiesel as automotive and marine fuels.

The problems are growing

Most Brazilian steel companies either do not declare carbon neutrality at all, or do not have medium- and long-term strategies to realize this goal. And more ambitions are still held by local players rather than global ones.

«We are not going to set goals that we cannot achieve,» said Marco Polo de Mello Lopes, executive director of the Brazilian Steel Institute (IABr).

In mid-August, Gerdau announced it was cutting back on investments due to the influx of Chinese steel. According to CEO Gustavo Werneck, the decision reflects unfair competition from foreign producers, as well as the government’s lack of trade protection measures to block the supply of subsidized steel from China.

Gerdau had already closed a plant in Minas Gerais in the first half of this year and laid off 1,500 employees. The company’s other plants are operating at capacity, Werneck emphasized. If steel imports to Brazil continue to grow, the company will have to resort to additional layoffs, he said. At the same time, Gerdau will expand its operations in the U.S., given the more stable and predictable conditions in the North American market.

Obviously, this makes it really difficult for Brazilian companies to plan and implement decarbonization. The question is about the survival of the industry. And it is its own government that has driven it into such conditions.

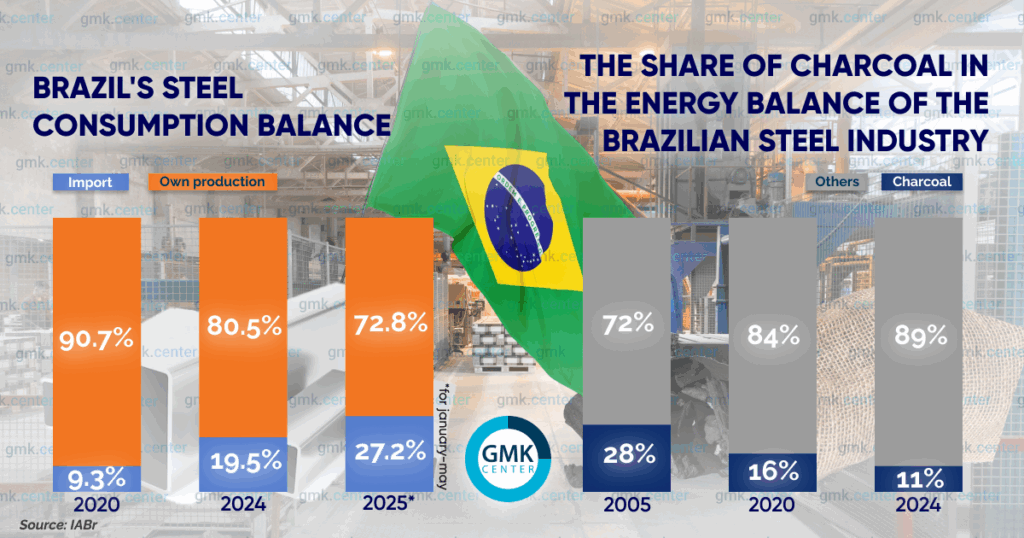

It is possible that Brazilian officials consider the local steel industry to be “green” enough as it is. The average emissions from steelmaking are 1.7 tons of CO2. But this is only partially true. The lower figure is due to BF’s use of charcoal instead of metallurgical coal. However, not everyone shares this view.

For example, in the European Union, this material is not considered as environmentally friendly because of the emissions from its production, as well as the impact on the climate from deforestation. According to the European assessment methodology, the average CO2 emissions in Brazilian metallurgy are 2.0 tons. And, for that matter, abandoning coal chips in favor of charcoal in blast furnaces is a huge step backward, a return to the technologies of the 18th century.

And we must also take into account the narrowing of charcoal utilization possibilities within the framework of forest protection policies. Therefore, in any case, companies cannot rely on this resource in the long term.

Ukraine: a reason to think

It can be assumed that the Brazilian authorities are in no hurry to close their steel market with duties because of the low cost of local products. According to Energy Transition, the country ranks 3rd in the world in terms of cheapness of metallurgical production, thanks to its reserves of high-quality iron ore.

But this is due to the BF-BOF mills. Which in the process of decarbonization should be closed and EAF plants should be built instead. Or convert to hydrogen technologies together with CCUS. Both options require huge investments – $29.19 billion, according to IABr calculations.

The question arises: where will metal companies get such funds from, if they are up against cheap imports in the domestic market? In such a case it is possible to compete only with low sales margins. And, accordingly, low profitability. But this is not all. Pretty soon, the investment opportunities of Brazilian steelmakers will shrink even more.

On December 12, 2024, Law 15.042/2024, which introduces a nationwide greenhouse gas emissions trading system (SBCE), came into force in the country. The preparatory phase will last until December 12, 2028. Until that date, companies are only required to report their CO2 emissions. After that, they will have to pay for their emissions. This is likely to make BF-BOF production unprofitable.

It is worth noting that a similar situation is developing in Ukraine. Both countries have sufficient iron ore resources for the steel industry. But there is a shortage of scrap required for EAF transition. The EU market is as important to the Ukrainian steel industry as the American market is to the Brazilians. And access to these markets is severely restricted. For Brazil – by Trump’s current duties, for Ukraine – by the prospect of the European EAF.

Therefore, Ukrainian metallurgists are also facing the need for decarbonization. Here, too, the authorities continue to work on launching a greenhouse emissions trading system (GET). But at the same time, as in Brazil, the domestic steel market is very much under pressure from imports. Consequently, Ukraine’s steel industry risks being trapped in the same trap as in Brazil.

-

15 June 2026

10 November 2025

16 October 2025

14 October 2025