Infographics steel import 2051 17 September 2025

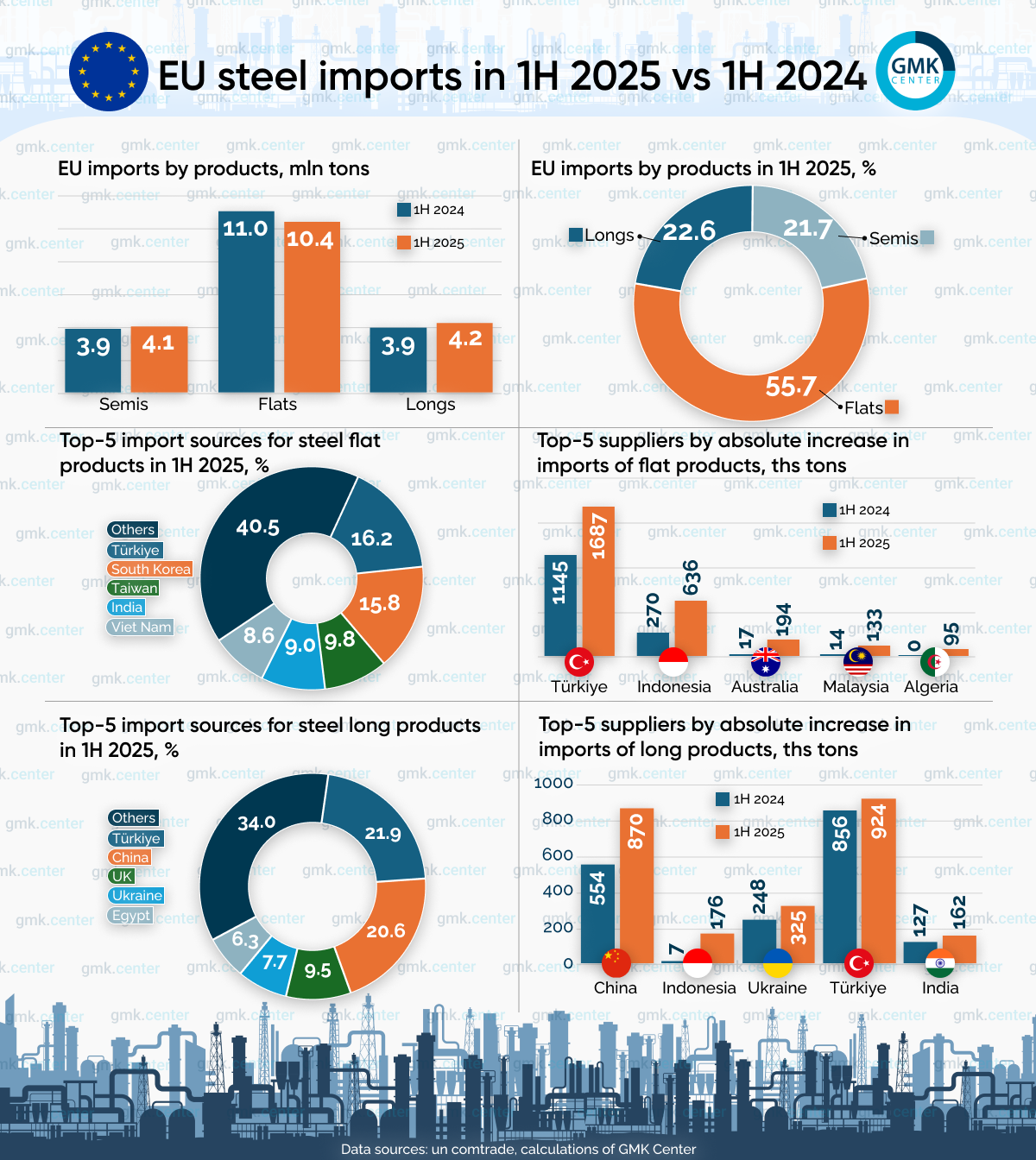

Flat products accounted for more than half of steel imports

In January–June 2025, the EU imported 18.7 million tons of steel, including semi-finished products, flat products, and long products. For comparison, in the same period of 2024, this figure was 18.9 million tons. The stability of import volumes contrasted sharply with price dynamics: since the beginning of May, prices for hot-rolled coils have fallen by 12.9%, while prices for rebar have fallen by 6.1%. This underscores the scale of the market shock that the region is experiencing this year.

The greatest pressure on prices came from imports from Southeast Asia. In early September 2025, suppliers from Indonesia offered hot-rolled coil at €480/t CIF, while Turkey and India offered it at €525/t CIF. Such significant discounts forced other exporters to revise their pricing strategies in order to maintain their market share. Loopholes in European protective measures and the slow response of regulators contributed to an increase in low-priced flat steel supplies to the EU market.

The share of imports in long product consumption remains relatively small, at around 15.0% in the first half of 2025, so imports in this segment do not have a significant impact on prices. In addition, strict restrictions on the use of third-country quotas effectively curb the growth of long product imports. As a result, prices in this segment did not fall as sharply as in the flat steel market.

The problems of the European market are related not so much to the total volume of imports as to the unfair practices of individual suppliers. Therefore, instead of introducing broad restrictions on import volumes, it is more appropriate to focus on monitoring prices to identify signs of unfair competition and to take targeted measures against specific countries and companies where necessary.

In the first half of 2025, imports of long products to the EU increased by 6.8% y/y – to 4.2 million tons, while imports of flat products decreased by 5.6% y/y.

Flat products remained the largest import category, accounting for 55.7% of total shipments during this period. The five largest suppliers (Turkey, South Korea, Taiwan, India, and Vietnam) together accounted for 59.5% of flat product imports. The largest growth in supplies was recorded from Turkey (+542.5 thousand tons), Indonesia (+366.1 thousand tons), and Australia (+176.9 thousand tons).

In the long products segment, the five leading suppliers to the EU in the first half of 2025 were Turkey, China, the United Kingdom, Ukraine, and Egypt. Imports of long products are more concentrated than flat products: the top three suppliers (Turkey, China, and the United Kingdom) accounted for 52.0% of total supplies. China (+315.9 thousand tons) and Indonesia (+168.8 thousand tons) showed the highest export growth. The increase in supplies from other countries was much more modest. For example, Ukraine increased its exports to the EU by 77.0 thousand tons, which is only 0.3% of the apparent consumption of long products in the EU in the first half of 2025.

As GMK Center reported earlier, the European Commission will propose a new way to restrict steel imports. European Commission President Ursula von der Leyen noted that global overcapacity is squeezing steel producers’ margins and leaving little incentive for environmental premiums. She stressed that Europe will always remain open and welcome competition, but will protect its industry from unfair competition

-

Opinions Industry steel consumption

13 July 2026

20 July 2026

06 July 2026

01 July 2026