Posts Industry steel consumption 1069 01 September 2025

In 1H2025, steel consumption grew by 13% year-on-year, but taking into account the normalization of inventories, real growth amounted to 9% year-on-year

In the first half of 2025, the Ukrainian steel consumption market continued to recover, showing growth of 13% y/y. At the same time, virtually all steel traders noted a decline in margins and a transition to market stagnation amid a significant increase in steel imports from Turkey and China.

Visible growth amid stagnation

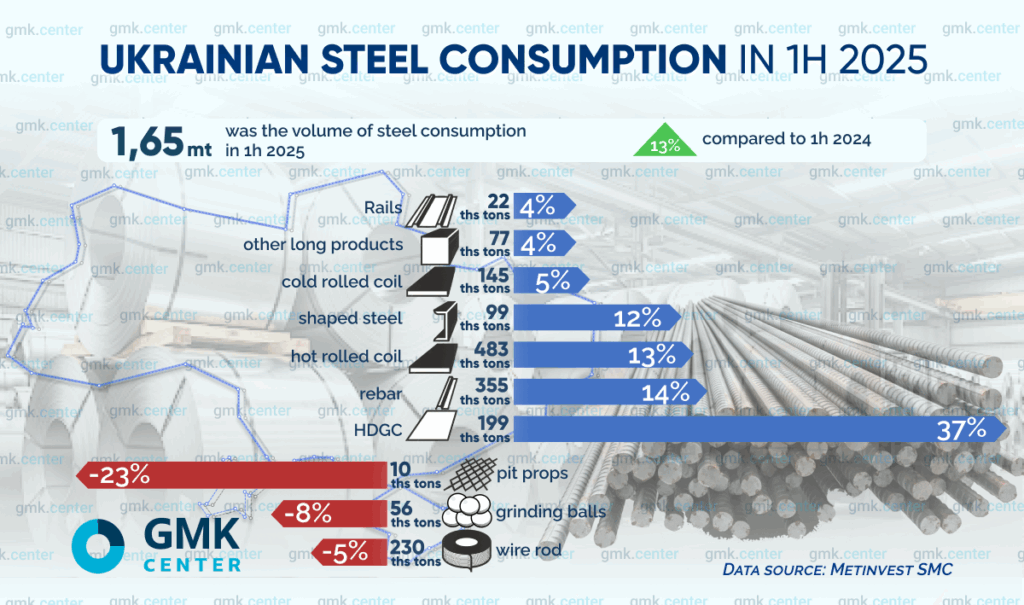

The volume of steel product consumption in the Ukrainian market (excluding polymer-coated rolled products, stainless rolled products, and tinplate) grew by 13% y/y – to 1.65 million tons in the first half of 2025. However, attempts by steel traders to increase sales and market share by contracting imports before the season led to oversaturation. According to Olexander Vedernikov, head of the analytics and pricing department at Metinvest-SMC, the increase in steel traders’ inventories since the beginning of the year is estimated at more than 120,000 tons. Taking into account the normalization of inventories, the real growth in market capacity was about 9%.

At the same time, market operators surveyed by GMK Center note mixed half-year sales dynamics: some companies showed 10-15% growth, while others saw a 5% decline. However, all note that the market is practically not growing, being on the verge of stagnation (or already in it).

The companies surveyed in the industry cite the following main problems (in addition to general security risks):

- Staff shortages, especially in blue-collar professions. Even companies with booking capabilities are experiencing difficulties with hiring.

- Falling margins and dumping.

- Delays in payments. Lack of payment discipline limits the implementation of projects.

- Logistics problems: long delivery times, unstable tariffs, and the refusal of some carriers to work in frontline regions.

Structural changes in steel product consumption

The structure of steel product consumption in the first half of the year shows mixed dynamics. According to Metinvest-SMC, the segments most affected in the first half of the year compared to the same period in 2024 were those related to construction to varying degrees:

- galvanized rolled products – by 37% to 199 thousand tons, which is associated with active imports and the development of domestic

- production of polymer-coated rolled products;

- rebar – by 14% to 355,000 tons, mainly due to construction;

- hot-rolled products – by 13% to 487,000 tons;

- shaped rolled products (beams, angles, channels) – by 12% to 99 thousand tons;

- cold-rolled products – by 5% to 145 thousand tons;

- other long products and rails – by 4% – to 77 and 22 thousand tons, respectively.

At the same time, consumption declined for a number of rolled steel products:

At the same time, consumption declined for a number of rolled steel products:

- SVP profiles (mine props) – by 23% to 10 thousand tons, due to the curtailment of coking coal production in Pokrovsk;

- grinding balls – by 8% to 56 thousand tons, due to a decrease in exports of iron ore and a reduction in the workload of mining and processing enterprises;

- wire rod – by 5% to 230 thousand tons, which is explained by the replacement of steel with other materials.

Sectoral and regional consumption structure

The most significant change that the Ukrainian steel trading market has undergone recently is a substantial reduction in demand from infrastructure and fortification projects. The former is related to the closure of USAID programs, which financed the construction of shelters over energy facilities. Demand from fortification projects has decreased due to the use of non-metallic substitute products.

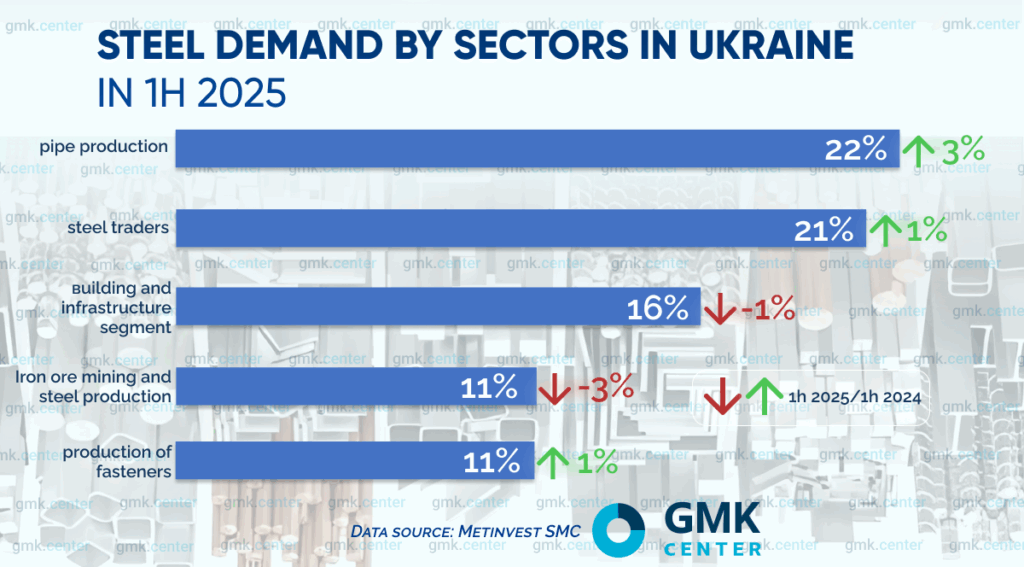

An analysis of the structure of demand by sector in the first half of the year (based on data from Metinvest-SMC) shows the following changes (compared to 1H 2024):

- The pipe industry took the lead with a 22% share of the total portfolio (compared to 19% a year earlier), thanks to an 18% increase in hot-rolled coil deliveries.

- Steel traders also strengthened their position, with a 21% share compared to 20%.

- Construction companies remained relatively stable: 16% compared to 17%.

- The iron and steel complex reduced its share to 11% (from 14%) due to the loss of mines in Pokrovsk and a decline in exports of iron ore.

- Private customers became more active: their share grew to 11% from 10%.

For his part, Roman Anzin, CEO of Vartis, notes that the main consumers remain mechanical engineering, the agricultural sector, and private construction.

For his part, Roman Anzin, CEO of Vartis, notes that the main consumers remain mechanical engineering, the agricultural sector, and private construction.

«In the western regions, against the backdrop of business relocation and growing demand for housing, private construction and commercial properties continue to generate stable demand. A significant part of the activity is in the agricultural sector, with farms investing in warehouses, logistics infrastructure, and technical facilities. At the same time, large-scale development and heavy industrial construction remain on hold, which reduces their share in the overall consumption structure,» the expert says.

According to some estimates, the steel products segment for mechanical engineering grew by 25-30% in 2024, and in the first quarter of 2025, the increase was another 10-12%. The key driver of demand is the defense industry. The overall conclusion is that consumption is increasingly shifting from infrastructure projects to commercial and private construction, as well as defense projects.

Since the start of the war, there have been significant changes in the regional structure of consumption, with consumption growing in the western regions.

“In the spring, with the start of the construction season, our sales in Western Ukraine increased. While the western regions have always accounted for 20-30% of sales, today they account for more than 50%,” notes Vitaly Prytula, director of Eurometal.

Among the other regions, the Kyiv and Dnipropetrovsk regions continue to maintain high consumption volumes. At the same time, the frontline regions of Kharkiv and Zaporizhzhia are showing a sharp drop in demand.

Increased pressure from imports

One of the key trends in the first half of the year was a significant increase in pressure from imports. According to Metinvest-SMC, it grew by 36% year-on-year in the first half of 2025.

“There has been a significant increase in imports, with interest shown not only by large steel traders but also by individual producers who are also trying to enter the steel trading market,” says Olexander Vedernikov.

Turkey stands out in terms of imports. In the overall import structure, the share of Turkish steel products increased to 71% (a year ago – 66%), displacing primarily European suppliers. The situation is particularly striking in the galvanized rolled steel segment, where imports grew by 60% year-on-year to 147,000 tons in the first half of the year (according to Metipol). Supplies from Turkey account for 86% of total imports in this segment.

Vitaly Pritula confirms this trend: “Previously, Turkish steel products accounted for about 15% of imported steel, but today they account for about 40%.” China’s share in the first half of the year grew from 4% to 10%. As a result, the share of other importing countries decreased from 30% to 19%.

Competition is particularly fierce in the sheet steel and rolled products segments. Imports offer more attractive prices, forcing Ukrainian manufacturers to adjust their pricing and product range policies. In turn, Ukrainian steel trading companies are trying to strengthen their positions through flexible pricing policies, service, and expansion of their product range.

Market development forecast

Despite the challenges, market operators are moderately optimistic.

“No significant negative trends have been observed so far. Until the end of the year, demand and market growth dynamics will remain at the level achieved in the first half of the year,” believes Olexander Vedernikov.

There may be a decline in visible market supply due to accumulated warehouse stocks, especially in November-December, when many players will try to “dump” steel products before the low winter season. On the other hand, there may be a short-term increase in deferred demand if prices stabilize in August-September.

Metinvest-SMC expects that by the end of 2025, market capacity could grow by 10% year-on-year, barring any sudden external shocks. This situation reflects a broader trend of market cooling after an intense recovery in 2023.

“After a sharp recovery in 2023, the market was supposed to move into a balanced state. That is why the baseline scenario for the industry in 2025 is to maintain last year’s results,” Roman Anzin emphasizes.

The Ukrainian steel trading market has already adapted to the conditions of war, but its significant growth is only possible after the end of the active phase of hostilities as part of the country’s post-war recovery.