Posts Global Market scrap prices 8520 28 May 2024

The offer is kept at a high level

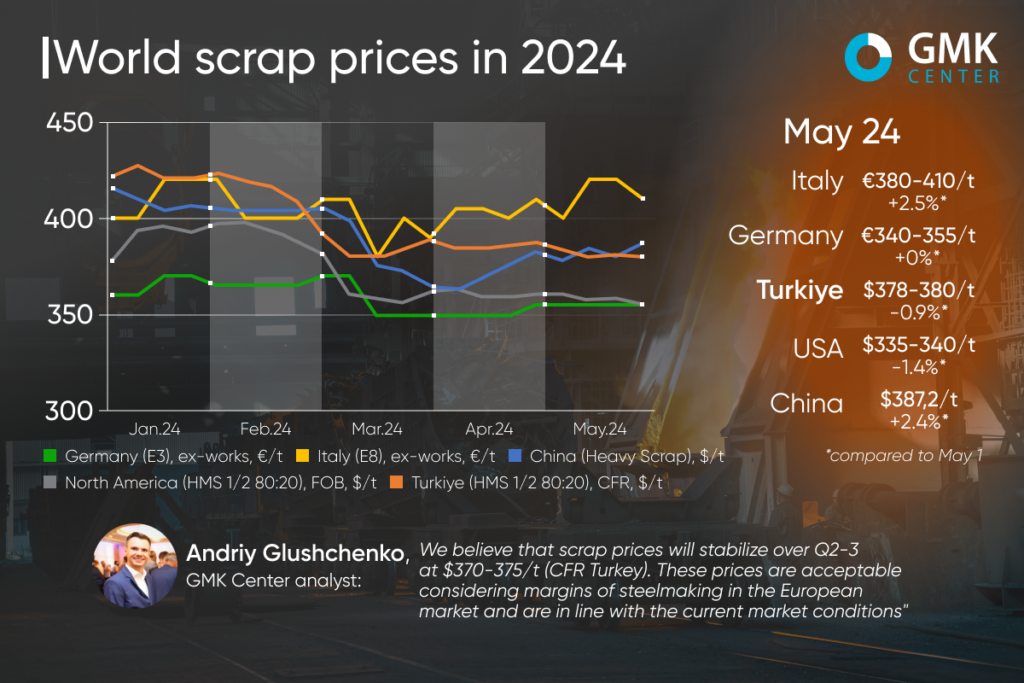

Global scrap prices remained largely stable in most major markets in May. Price fluctuations did not exceed $10/t.

Prices for HMS 1&2 80:20 scrap on the Turkish market in May 2024 are mostly stable. They fluctuate within $5/t. In particular, as of May 27, raw material quotes amounted to $378-380 CFR, which is the same as the previous week and 1.3% less than the price at the beginning of the month.

Overall, the Turkish scrap market has been stable since early spring. Prices were mostly at the level of $380-390/ton. At the same time, in January-February, raw material quotations reached $427/t and generally remained at least $400/t.

The positive trend at the beginning of the year was driven by improved market sentiment due to increased demand for raw materials during the post-holiday period. At the same time, in late winter and early spring, prices were adjusted after being kept high for a long time. This was driven by a slowdown in the Chinese steel market, an increase in scrap supply and Turkey’s macroeconomic problems.

May is currently the month with the lowest monthly average scrap prices in Turkey in the spring, as steel producers do not have an urgent need for purchases due to weak demand for steel. In addition, scrap prices are under pressure from a decline in the price of square billets.

Weak steel sales, pressure on finished product prices, and low margins at steel mills are holding back purchases of scrap, especially imported scrap, which requires large batches of raw materials to be booked. The mills have chosen a wait-and-see attitude to assess the outlook for the steel market. At the same time, the supply of raw materials is sufficiently high to prevent price increases.

At the same time, prices for raw materials are not falling below $380/t, as suppliers have indicated that this is the lowest operating level due to the slow collection rate and the strengthening of the euro.

Expectations for the future prospects of the Turkish steel and scrap market are negative. In June-July, Turkey is expected to see a significant increase in electricity prices. This will lead to a further decline in the profits of local steelmakers and, accordingly, shutdowns of production facilities. In May, Marmara Steel shut down for a week due to weak demand for steel.

«If this is the demand now, even though we are in the middle of the highest construction season, I don’t want to imagine what will happen in the summer. The only change in the situation may be the resumption of steel sales to Israel. Other than that, I don’t see any impetus for recovery,» said a source at a Turkish steel mill.

Currently, scrap prices are squeezed into a fairly narrow range, as mills cannot afford higher levels due to pressure on steel prices, and suppliers, particularly Europeans, do not agree to lower levels due to slow collection rates.

In the short term, scrap prices in Turkey will remain largely stable as the market has reached a stalemate. At the same time, electricity prices will play a key role in price formation in June-July. If electricity costs rise at the current level of steel demand, local steelmakers will resort to significant production cuts, which will significantly reduce demand for scrap.

The European market showed a mixed trend in May. In particular, in Italy, scrap prices (E8 Light New Scrap) increased by €10/t – to €380-410/t Ex-Works in the period from May 3 to 24, while in Germany (E3) they remained stable at €340-355/t Ex-Works.

At the same time, Italian prices reached €420/t, but declined due to a drop in market consumption. The German market saw prices stabilize during the month due to low demand from domestic steel mills and a decline in exports.

As scrap becomes more available in Western and Southern Europe, mainly due to lower demand from Turkey and North Africa, steel mills are more confident and believe that prices will decline slightly in June.

North America saw a slight decline in prices in May, down $10/t – to $335-340/t (US Midwest Delivered Basis) as of May 24. As supply and demand have balanced out and industry fundamentals are still insufficient to support commodity prices, prices have slightly adjusted downward. In addition, the market recovery was not helped by the maintenance shutdowns of some steel mills. Additional pressure came from a drop in domestic hot-rolled steel prices and weaker export expectations and demand.

In June, scrap prices are expected to remain unchanged or slightly decrease as market fundamentals are still not strong enough to support prices.

As of May 27, 2024, prices for Heavy Scrap in the Chinese market amounted to $386.2 per tonne, up 2% from the price as of May 1.

Raw material prices in China in May strengthened amid improving prospects for steel consumption. Scrap consumption increased after Labor Day, which was accompanied by an increase in productivity and capacity utilization at electric arc furnace mills. In addition, prices were supported by a decrease in the supply of raw materials due to environmental inspections in some regions of the country.

At the same time, the market is still quite volatile and scrap does not have a price advantage over pig iron, so further growth expectations are limited.

«We believe that scrap prices will stabilize in Q2-3 at $370-375/t (CFR Turkey). These prices are acceptable in terms of margins for steelmaking in the European market and are in line with current market conditions,» said Andriy Glushchenko, GMK Center analyst.

The outlook for the global scrap market is negative. Turkey, the world’s largest importer of raw materials, faces numerous obstacles, including a decline in sales of finished products due to the loss of the Israeli market and an expected increase in production costs. The European and North American markets are heavily dependent on demand from Turkey, which has not yet shown any positive signals. Prices may be supported by an improvement in the Chinese steel market amid numerous consumption incentives from the authorities.

-

OpinionsGlobal Marketsteel consumption

13 July 2026

14 July 2026

16 June 2026

10 June 2026